H2 Letter, EIP

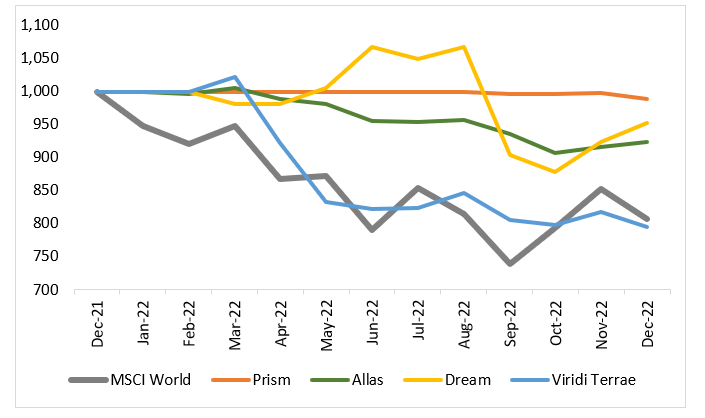

Let's take a look at how EIP performed from July to December 2022

New Strengths and New Market Conditions

Dear Sponsors, Board of Advisors, and Members,

I share with great pleasure that the ESG Investing Program has found itself with added strengths — the new EIP batch members would be installed into their new teams. I believe that they will provide additional insights with new perspectives to reinforce the current teams. This is my first time writing a letter for the whole club and it is exhilarating to be given so many responsibilities as a student while at the same time given a sum of money to invest.

Added Members

Team Prism – Kenneth Tee, Fernando, Dean Tay, Nicole Tan

Team Allas – Nicholas Tan, C M R Sooria, Sim Jia Yang

Team Dream – Koh Hui Ling, Iris Tan, Amelia Lee, Yiong Jon Lon

Team Viridi Terrae – Girvin Chang, Valerie Kang, Clive Tan, Jerome Teo

As we just ended a volatile year, it is important for us to reflect on our past actions, so that we can learn and apply them to our future. It is also with great pleasure to announce that majority of our portfolios are beating our benchmark, MSCI World Index.

Individual Team’s Reflection and Plans

Team Prism

Over the past year, we have held onto a defensive stance in the face of geopolitical tensions and rising interest rates that did not represent a meaningful risk-reward opportunity. As such, we maintained a 100% cash allocation until the end of Q3, when we initiated our first and only stock allocation to date, Alphabet Inc ($GOOGL).

Moving forward, we will more aggressively deploy capital into reasonably priced high cash flow businesses with a dominant moat. This is a stark shift from our defensive stance in 2022 as we believe that broad valuations have retraced to attractive levels and much of the macro pain is over.

Team Allas

For Team Allas, Q4 was a pretty exciting one because we did up an investment memo to buy another stock to add to our portfolio – SoFi Technologies. We felt that SoFi was and is still heavily undervalued to date and had presented as such during the latest portfolio update in December.

Being invested in SoFi would mean that Team Allas is primarily invested in the technological sector, albeit SoFi serving more as a FinTech platform compared to Meta – our other stock pick within our portfolio. With regards to the direction that our team is moving in, we would most likely diversify into other sectors such as the healthcare industry. Our team has done up another investment memo for Becton, Dickinson & Co and will possibly be invested in it soon!

Team Dream

Q4 2022 was characterised by extreme volatility, and that is saying something given developments in the preceding quarters. Global equity markets plunged in September as inflation remained sticky and monthly figures for August came out to be above consensus estimates. This shifted baseline expectations to one in which the Fed hikes rates to the median point of around 5% somewhere in 2023, with a longer, dragged out battle against inflation. Merely a month later, Xi Jinping further consolidated power at the 20th National Congress in which he secured a third term and installed loyalists to the CCP’s inner circle. The political manoeuvring cemented China’s image as an “anti-capitalist, uninvestable market”, though the real rhetoric at the Congress concerning Covid-zero and common prosperity remained unchanged for the year.

As others fled for safety, our team embraced the volatility and averaged down on our highest conviction ideas, such as GDS Holdings. We also initiated a position in American Water Works over the quarter that saw rationality forsaken even further for emotions. Our four current holdings – Daqo New Energy, Adobe Inc, GDS Holdings, and American Water Works, reflect Team Dream’s investment philosophy of “only investing in companies that we understand”, whereby these are relatively simple businesses to grasp but are nonetheless clear leaders in their respective markets with decent growth runways. At the portfolio level, our concentrated portfolio is also positioned for resiliency in an economic downcycle, given our sectorial tilt towards renewable energy, utilities, and IT infrastructure.

Just as we were (and are still) bullish on Chinese companies even when others classified them as “uninvestable” a little over a year ago, we continue to view volatility as golden opportunities. Moving forward, we continue to look for the next “land of opportunity”. With the sharp re-rating of Chinese stocks as the market digests the lower likelihood of a near term recession (China’s reopening, resurgent domestic demand, and monetary policy options at its disposal), we are inclined to seek out high quality US growth tech, a basket that has seen drastic valuation drawdowns.

Team Viridi Terrae

2022 was a year full of rollercoasters for the stock market, especially in the tech sector. Our team bought Unity in late March at what was considered a discounted price back then and was optimistic that the fundamentals of Unity was solid enough to withhold the temporary dip in the market. Today, we still believe in Unity’s fundamentals but were obviously mistaken about the “temporary” part. We witnessed the stocks continue crashing after multiple rounds of hikes in Fed rates, coupled with the uncertainty of (stag)inflation, Ukraine war, COVID and US-China tensions.

For many of us young investors, especially those who started our investing journey during the ‘good’ year of 2021, it’s our first experience of this extent of paper loss. The team debated about the counter strategy to such a climate, whether we should continue holding on to Unity, and whether we should buy other stocks at their low prices. There were uncertainties and there were paralysis; there were missed opportunities and there were regrets. Regardless, the whole experience was a learning journey for us, particularly in terms getting our anxieties under control. It was also a timely reminder for us on why taking a long-term view on companies are so important. Great companies are the ones which can withstand the challenges of times and economic cycles; likewise, great investment decisions should give investors the confidence to stand by these companies during such difficult times.

That said, there’s always a silver lining. Taking the tech sector as an example, many companies went through tough retrenchments in 2022. While such retrenchments are upsetting to individuals, from a company perspective, it signalled streamlining of businesses and a goodbye to bad or weak actors. The companies that survive will come out of this stronger and more resilient. ESG also shines amidst the gloom as more investors realise the advantage of companies with strong ESG ratings - more resilient, more effective, and more innovative. It’s a good year for ESG as more players join the ecosystem to help figure out pertinent issues such as standards, regulations and solutions.

Moving into the new year, the team is cautiously optimistic about the year ahead. We see positive signs such as the reopening of China’s borders, which will drive travel and consumption globally, and the ESG momentum continuing to grow strong. Challenges of inflation, COVID and geopolitics continue to linger, but we believe that after the rollercoaster ride in 2022, the team is more equipped and ready to face the uncertainties head-on. With our new members onboard, we will continue to learn together and hopefully, chart new ‘stocks’.

Overall Performance and Reflections

2022 was an astonishing year. The market has been unsettling: supply-chain congestion, COVID-19 infection waves, Russia’s Invasion of Ukraine, sky-high inflation, China’s zero-Covid Policy, central’s bank tightening, and many more…

We have also seen some uplifting developments in the market as well. The latest Drewry World Container Index stands at $2,119.96, which is 80% below the peak of $10,377 reached in September 2021, suggesting that the supply-chain pressures have been eased significantly. Global vaccination data states that 64.8% are fully vaccinated against COVID-19, transiting towards an endemic. The latest data also hints towards peaking inflation data – YoY CPI peaked at 9.1% in June, and since then monthly readings have steadily declined. Does that mean that 2023 would be a better year for investors?

With inflation starting to ease, many participants believe that the Federal Reserve would soon pivot its tightening policy back towards simulative. This would cause interest rates to return to near-zero levels. Either recession would be averted, or it would be modest and brief, and the market would soon return to better levels. While this may be a possible scenario, it is unlikely. This is because if the Fed rewinds back its interest rate to near-zero levels, it would have little ammunition left to help the economy should any new problems arise. Thus, I believe that the Fed would instead reduce the interest rate to around 2% in the long run, allowing room for both tightening and loosening, based on the situation.

While it's difficult to predict where the markets would go, I personally believe that the markets would still be bearish some time ahead, followed by a slow recovery. But let’s not forget that bear markets can be our friend too and market disruptions are always around as the market always finds a way to recover. Thus, we should invest amidst extreme pessimism.

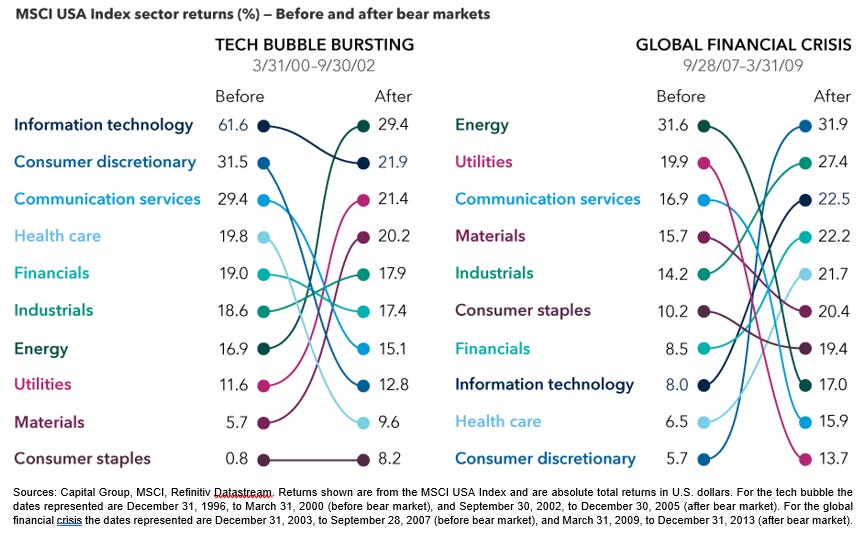

Also, as we approach a new market cycle filled with new market conditions, history has taught us to avoid the winners of the last cycle. According to Capital Group and an analysis of the two previous bear markets, with the shuffled sector leaderboards, investing in more unpopular sectors like utilities and telecommunications that generate consistent cash flows may be more prudent in today’s environment.

Therefore, I believe that we should continue to be prudent with our investments and invest in sectors that would perform well during this changing environment. With that, I would just like to wish everyone a great 2023 year ahead and happy investing!

Best regards,

Sooria C M R (Chairperson) / Sim Jia Yang (Co-Chairperson)