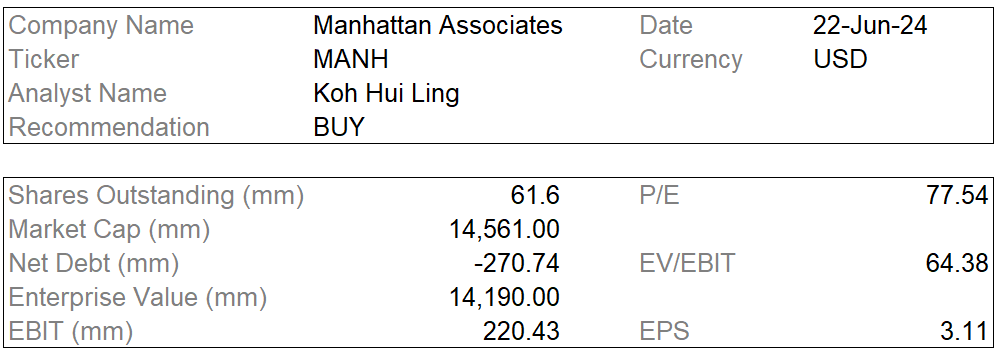

Initial Memo: Manhattan Associates, Inc. (NASDAQ:MANH), 35% 3-Year Potential Upside (Huiling KOH, EIP)

Huiling presents a "BUY" recommendation on Manhattan Associates due to sticky revenue streams from maintenance revenue create recurring revenue and strong relationships.

Linkedin | Koh Hui Ling

Company Overview

The company designs, builds and delivers supply chain commerce solutions globally. The company offers products through direct sales personnel and partnership agreements with various organizations. The company operates in the Americas, Europe, the Middle East, Africa, and the Asia Pacific. Company’s revenue centers around three main buckets – supply chain, omnichannel commerce, and inventory management. 3 products – OMS, TMS, WMS. Customers include Walmart, Loreal, Nike, and Home Depot. Expertise in apparel-based businesses such as Under Armour, Lululemon, Adidas, and Crocs.

Business Model

Software

Software License

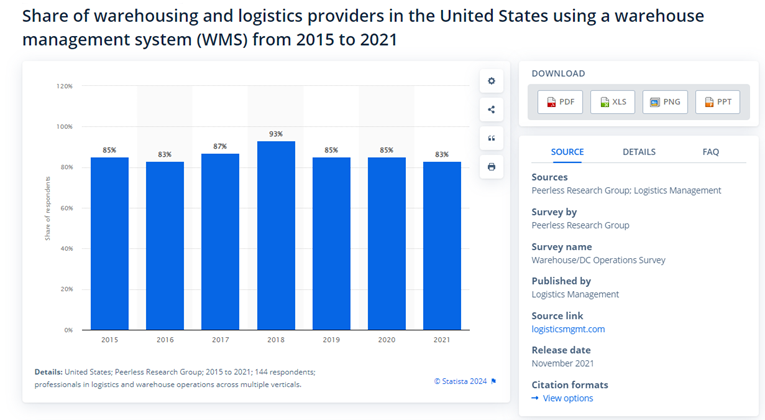

Industry

There is also room for growth in the market for WMS with only 83% of warehousing and logistics providers in the US using a WMS.

Investment Thesis

Thesis 1: Sticky revenue streams from maintenance revenue create recurring revenue and strong relationships

Sticky revenues because once everything works together nicely, there’s a very small chance the customer will ever rip the system out. These software solutions aren’t quite as sticky as something like an ERP which ties the entire business together but supply chain management software has notoriously low churn rates because stitching together all of the assets is very time consuming upfront and directly affects revenue and profits.

Revenue accelerating due to cloud business growth (consistently larger portion of total revenue). 6 years into cloud transition and it only accounts for 25% of overall business. What’s interesting is that Manhattan didn’t have to go through the same cash flow trough that Adobe did since they get half of their revenue from services. The company was able to slowly shift customers from on-premise deployments to the cloud. That’s why it has taken a while – here we are six years later and 26% of revenue is from the cloud. COVID did accelerate the adoption of the cloud products too because in-person maintenance upgrades became far more of a hassle. The products that Manhattan offers are extremely mission critical, so transitions have to be very smooth. In fact, the company was planning the transition and the development of cloud products for four years prior to actually launching in 2017.

Cloud growth driven by companies shifting to omnichannel model of having stores and efficient e-commerce operation. For eg, “the business of retail has gotten much more complex over the past decade. Nike can’t just ship products to Footlocker and get their money anymore. They have to do DTC, have their own fulfillment centers, contract with logistics providers, and do returns. The operations have become much more complex which is a tailwind for Manhattan.”

Gross margins in low-to-mid 50% because 50% of business is still professional services. Lower than standard 70%-80% pure SaaS business but these are necessary because these aren’t small implementation. It’s quite difficult to tie together a bunch of distribution centers, trucks, and retail stores. FCF margin consistently in 25% range (> EBIT margin), due to strong working capital dynamics and deferred revenue. Operating leverage increases as cloud business continues to scale (1Q24 +250bps YoY).

Management

Management has shown to be thoughtful as shown by its gradual and thoughtful cloud transition. The company has also bought back 40% of its shares over the last 15 years.

Valuation

Based on a DCF valuation, my 1-year target price is USD259.85 (11.3% upside), which gives an intrinsic forward P/E ratio of 47.7x.

However, based on an intrinsic value basis, Manhattan is valued at USD 253.15 (8.46% upside), with a forward P/E ratio of 70.4x. The high P/E ratio can be attributed to the lack of other listings that provide the same exposure and opportunities in this sector, especially from one of the leaders, has led to very high P/Es for Manhattan.

Risk

Macro-economic uncertainty and high i/r may hinder adoption of cloud technology

ESG Assessment

1. Social (S): Security and Ensuring Privacy of Products

a. Manhattan has a regular auditing process to test the security of its products, as well as to adhere to industry standards from CIS, ISO27001, and NIST. It also audits its security by an independent third party annually. The company also extends its Partner Code of Conduct to all its business partners. The company recorded zero data breaches involving any disclosure of customer sensitive data in 2020-23.

2. Environment (E): Energy consumption and water usage

a. The company uses a significant portion of energy, however balances that with offices that are located in buildings that use clean energy.

b. The company uses a significant amount of water (including its cooling towers) and with its % of water recycled fluctuating drastically year on year (33% in 2020, 59% in 2021, 24% in 2022, 48% in 2023), it may be indicative of poor internal practices to ensure that the facility does not waste water. Hence, this may an area of key improvement for the firm.

3. Diversity and Labour Force

a. The company has no instances of forced labour, child labour as of 2020-23.

b. The company appears to have lower levels of gender diversity, with little improvement across the years, where its % of female employees globally fluctuates between 26-27% from 2020-23. Furthermore, the demographics of its employees appear rather consistent year on year, which could be indicative of one of two things: 1) there is little diversity efforts which may lead to a lack of competitiveness if Manhattan is unable to understand local customs and form crucial relationships with its customers 2) there is little turnover in the company due its fair compensation/practices. Regardless, 1) is likely to play a bigger role in Manhattan’s growth as a company as it would stand to benefit from acquiring new customers and expanding globally to extend its market leadership with its market leading products.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk