Initial Memo: Monster Beverage Corporation. (NASDAQ:MNST), 52% 5-Year Potential Upside (Olivia ZHANG, VIP)

Olivia suggest that Monster’s stock price remains relatively high, making it an unsuitable time to buy.

LinkedIn | Jiayu (Olivia) Zhang

1. Company Overview:

Monster Beverage Corporation, formerly known as Hansen, is a Holding Company headquartered in Crona, California. It develops, promotes, sells, and distributes energy drinks through its subsidiaries. In 2002, it launched the Monster energy drink series and began transitioning from juice soda to energy drinks.

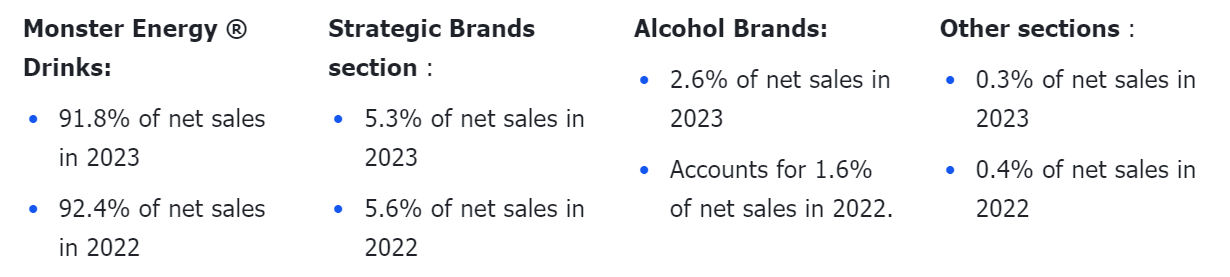

The revenue streams are primarily divided into four operating and reportable segments: 1) Monster Energy Drink (91.81%): primarily sells ready-to-drink packaged energy drinks (RTD) to bottlers and full-service beverage distributors. 2) Strategic Brands (5.27%): primarily generates net operating income from the sale of concentrate or beverage base to authorized bottled and canned partners for the brand series eg, NOS, Throttlee, etc., which were exchanged from Coca-Cola . 3) Alcohol Brands (2.58%): primarily generate revenue from the sale of barrel beer, ready-to-drink canned beer, hard fruit alcoholic beverages, and flavored malt beverages to beer distributors in the US. 4) Other (0.33%): Covers non-energy drinks, such as tea drinks, lemonade, and other soft drinks.

2. Company History

1) 1930-2001 Start-up period:

Operating juice and soda water business.

In 1997, following Red Bull, Monster launched the 8.3-ounce carbonated energy drink Hansen's Energy Drink, which ultimately failed.

2)2002-2007 Transition Period:

As a pioneer, Red Bull has completed consumer education about energy beverages, and the energy drink market has developed rapidly. In 2002, the company launched Monster Energy Drink, which was well received, and has since deeply cultivated the energy drink track.

Pricing strategy: counter positioning on pricing strategy-'cost-effective strategy', doubling the capacity at the same price. The company launched a 16-ounce product with a price similar to Red Bull's 8.4-ounce product.

Promotion strategy: At the beginning of the 21st century, young people in the US pursued individuality. The company used packaging that was different from traditional drinks such as Coca-Cola and Pepsi. It used a bold and avant-garde (dark color) image to match the marketing of high-intensity activities such as extreme sports and car races, anchoring the younger generation of consumer groups.

Channel strategy: In 2006, Monster signed a distribution agreement with Budweiser, the largest beer company in the US.

3)2008-2014 Globalization Transition Period:

In response to the 2008 US financial crisis, Q4 partnered with Coca-Cola's distribution network to expand the global market, increasing convenience store coverage to 92%. At the same time, Red Bull vigorously expanded its global distribution network. In contrast, Red Bull established the "Red Bull North America Distribution Company" to be fully responsible for Red Bull's sales in North America.

Signed a distribution agreement with Asahi Beer in Japan in 2011, responsible for exclusively distributing Monster products in Japan.

In January 2012, the company was officially renamed Monster Beverage Corporation.

4)2015-2023 Maturity period:

In 2015, Coca-Cola invested and obtained a 16.7% equity stake in the company for $2.17 billion. As of the end of 2023, Coca-Cola holds 19.5% of the shares and is the largest shareholder.

Completed brand exchange with Coca-Cola, obtained the energy drink brand owned by Coca-Cola, and entered the Coca-Cola bottling system at the same time. The company has transferred most of its bottling and distribution business to Coca-Cola bottlers.

On April 1, 2016, the company completed the acquisition of its long-term partner, American Fruits & Flavors (AFF), for $690 million. The integration of major flavoring suppliers into the company's system will provide better support for product flavor development and uniqueness retention.

Acquired CANARCHY in 2022, testing the beer industry.

Acquired VITAL PHARMACEUTICALS in 2023 to further enrich the product matrix with BANG ENERGY.

Implement pricing actions from 2022 to 2023, increase prices, reduce promotional discounts, and have a positive impact on gross profit in 2023.

3. Industry Overview:

3.1 What are energy drinks?

Energy drinks are beverages that contain energy ingredients and add additional nutrients or specific ingredients such as taurine, caffeine, guarana, ginseng, etc. These drinks are designed to supplement the body with energy or accelerate the release and absorption of energy.

Energy drinks not only have the thirst-quenching and hydrating functions of traditional packaged drinks, but can also quickly supplement the energy components needed by the human body. Compared with traditional drinks, they can enhance the functions of nerves, muscles, and the heart, providing health benefits such as refreshing the mind, restoring physical strength, and enhancing immunity. In addition, energy drinks are usually designed to be portable and easy to consume, suitable for athletes, professionals who work long hours, and people who need extra energy.

3.2 Alternatives to caffeine consumption habits:

Western consumers are accustomed to drinking addictive beverages and have a considerable dependence on caffeine. Compared with traditional coffee and tea, functional beverages not only meet the expectations of modern consumers for functional needs, but also keep pace with the times, closely combining products with culture and sports. Through rich marketing strategies and brand stories, they have successfully attracted advocates of healthy lifestyles and sports enthusiasts, effectively conveying brand concepts through sports and health. This combination strengthens consumers' dependence on functional beverages and develops strong stickiness, further increasing their brand loyalty.

1) Caffeine:

Central nervous system stimulants drive away drowsiness, but can easily cause irritability, anxiety, insomnia, etc

85% of Americans drink caffeinated beverages at least once a day, with an average daily consumption of 165 milligrams of caffeine per person. Energy drinks have a caffeine content of 0.3mg/ml.

2) Taurine:

Promote nutrient metabolism, improve human antioxidant capacity, have calming and attention-enhancing effects.

3.3 Market size, growth rate, and industry trends

According to Euromonitor, the size of the US energy drink market was $17 billion in 2019, and by 2023, this market size will increase to $23 billion, an increase of 35.3% from pre-epidemic levels. Energy drinks account for 9.2% of the entire beverage market, ranking fourth in the soft drink category. Compared with mature carbonated drinks, packaged water, and juice, energy drinks still have huge development potential.

Functional drinks are a high-quality track in the beverage market, thanks to the deep coffee culture abroad. Many people are accustomed to consuming caffeine every day to stay awake. Therefore, functional drinks are not only highly addictive, but also have a high Re-purchase Rate. Although their single bottle price is higher than that of ordinary carbonated drinks, it is lower than that of coffee. This pricing strategy and consumption frequency have jointly promoted the expansion of its market size.

4. Business Model:

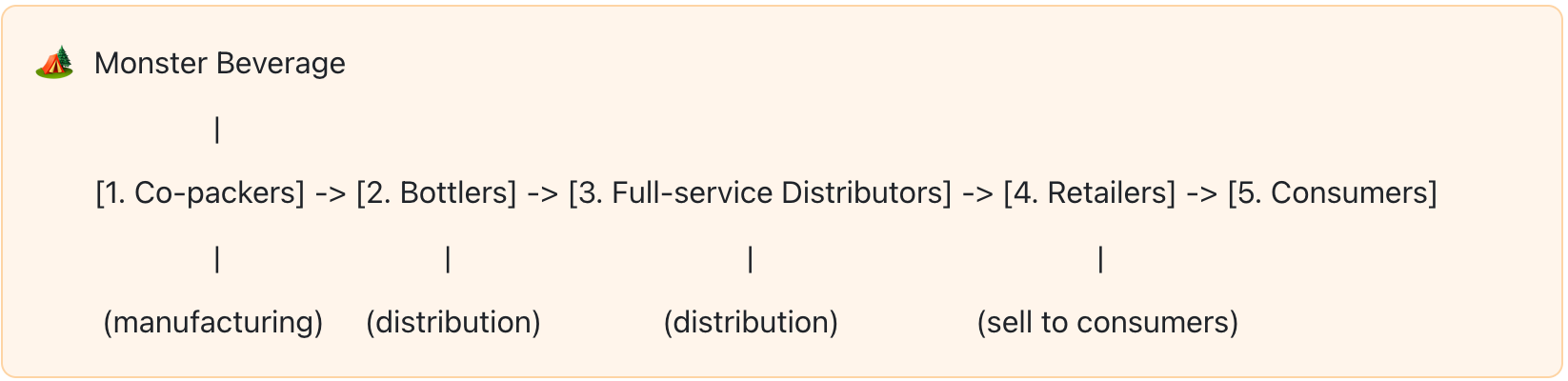

Monster primarily produces ready-to-drink energy drink RTDs (not directly manufactured goods) through contract manufacturers, and then sells them directly to end consumers through an extensive distribution network of bottlers and full-service distributions, including retail and wholesale channels.

Value positioning: "unleash the beast and release wildness"

It fits the consumption demands of young people who pursue individuality, vitality, and freedom.

The logo "Claw" and the name "Monster" both represent wildness, integrating fashion excitement, the pursuit of individuality, and the courage to challenge themselves into their corporate values.

Customer group :

young people aged 18-34, targeting young people who pursue excitement and vitality (this group is also the main consumer of energy drinks)

The main consumers of Red Bull functional drinks are tired people, and they occupied 80% of the market share in 2000. Monster (formerly Hansen) needs to differentiate its target audience by targeting young people who are energetic, exercise regularly, have good consumption ability, and have a high acceptance of US functional drinks. The two have different consumption scenarios and face different customer groups.

Key business

Monster series - selling bottled RTD

Distribution Channels/Partners :

Often work with local beverage companies or large beverage distributors in different markets to optimize their distribution network and market penetration rate. Mainly distributed through contract manufacturers, bottlers, full-service distributors, retailers, wholesalers

In the Monster beverage segment, the company primarily sells finished products (RTD, Ready to Drink) to bottlers and full-service distributors, and in some cases, directly to grocery stores, wholesalers, nightclubs, supermarkets, convenience stores, and catering channels.

4.1 Source of income : contribution by operating segment and region

1)Sales: In 2023, Monster Energy ® Drinks segment contributed the majority of sales, accounting for 91.8%. Ready-to-drink packaging is the key business, not concentrates.

Net sales in 2023 : 7.14 billion USD;

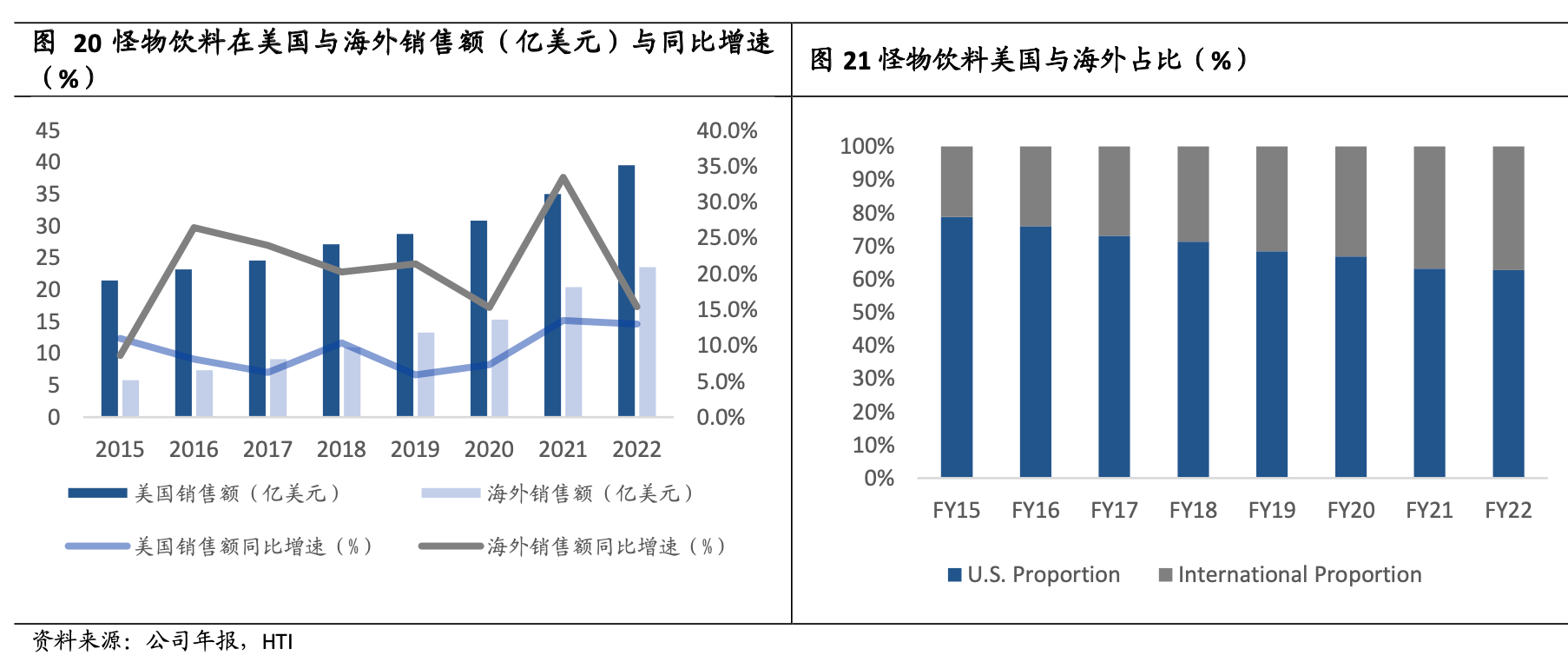

External sales (outside the US) : $2.71 billion, approximately 38% of total sales

The international market has gradually become the main driving force for revenue growth. With the expansion of energy drinks in overseas markets, the growth rate of overseas markets is significantly higher than that of the US market. The proportion of overseas markets in global total revenue continues to increase, making overseas revenue account for nearly 40% of global total revenue in 2022, compared to only about 21% in 2015.

Sales revenue and proportion of operating sectors:

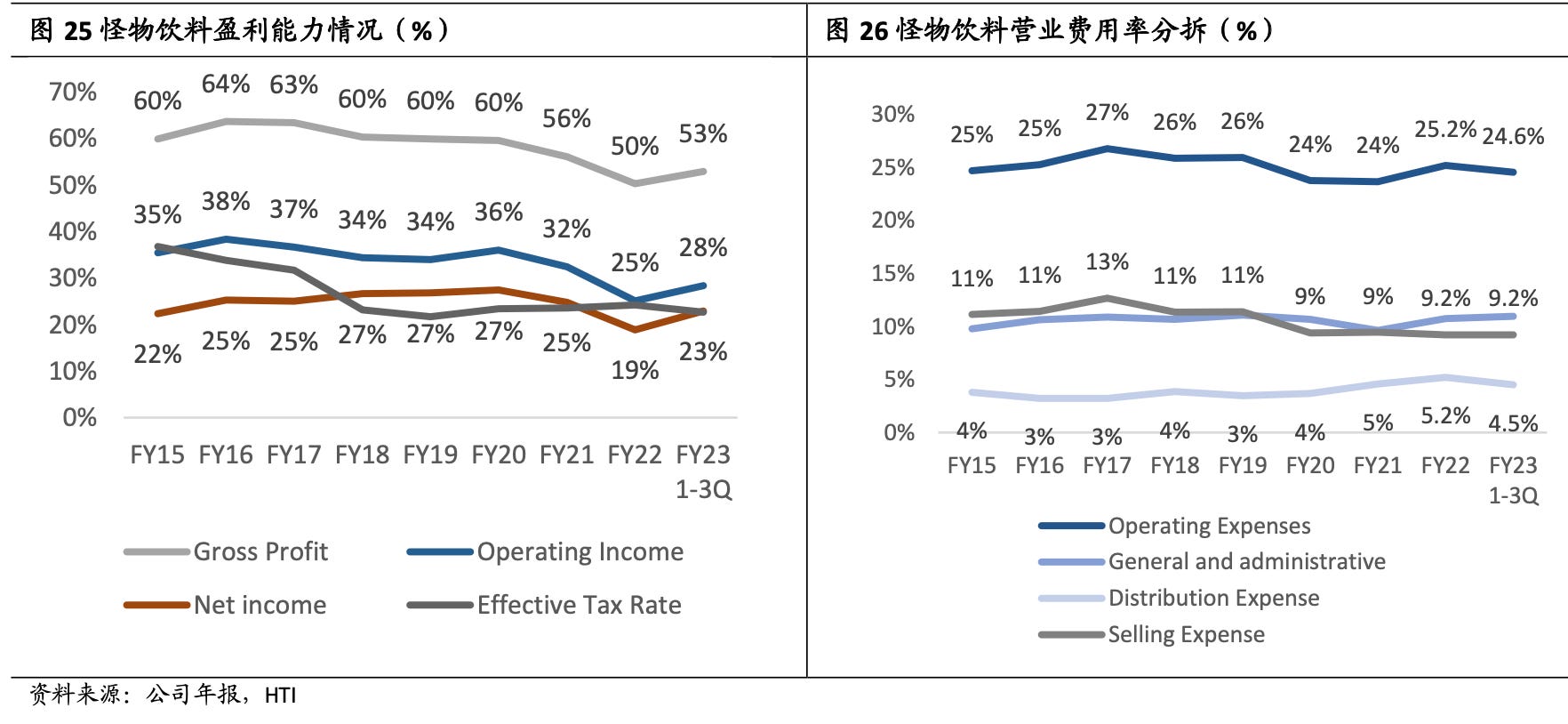

2) Gross profit margin, growth rate

-- Divided by regional income --

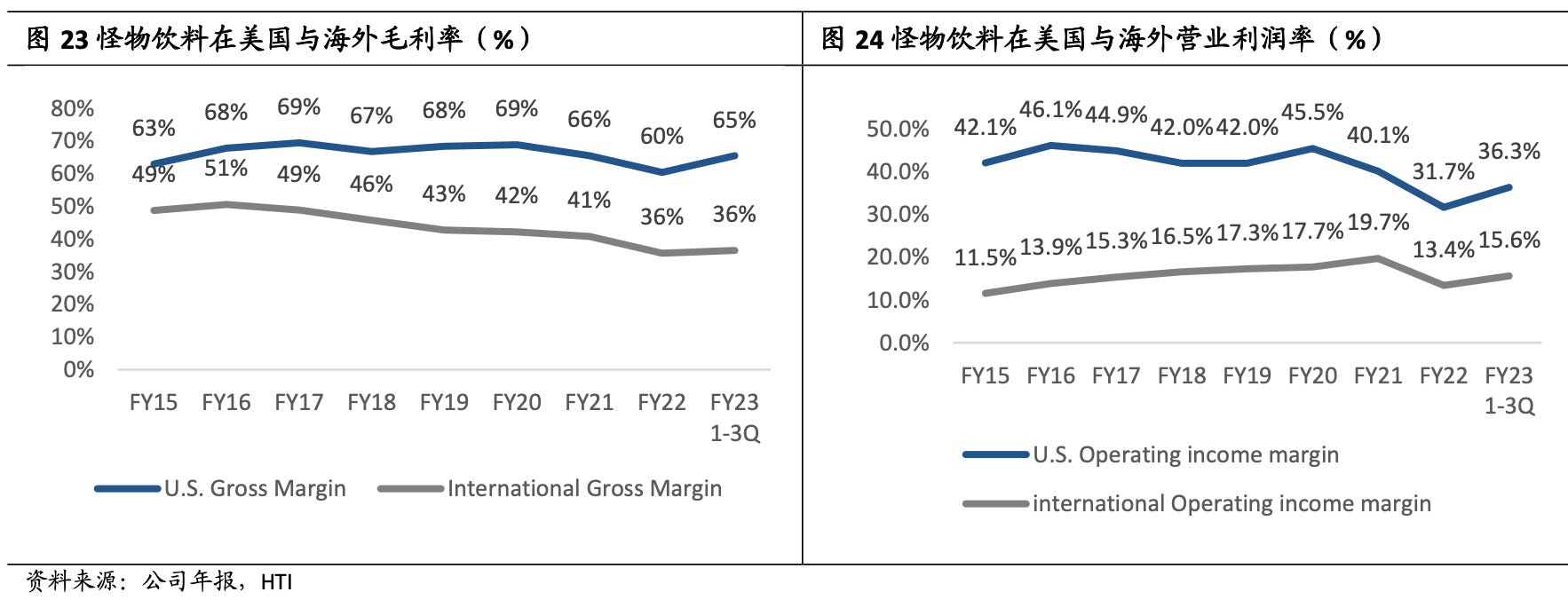

US market: Due to strong consumption power and high product pricing, the gross profit margin has been stable at about 68% for a long time.

International Market: In contrast, the average product pricing in the international market is lower, and the gross profit margin is only maintained in the range of more than 40%. From 2015 to 2020, especially in major markets such as Europe and South America, the gross profit margin has declined year by year, mainly because the overseas market is still in the growth stage, and the company has to increase some promotional subsidies to develop the market.

Overall: Overall, the company's gross profit margin remains between 50% -60%. From 2021 to 2022, the company's gross profit margin rapidly declined, from 56.1% to 50.3%, mainly due to the rapid increase in costs. However, since September 2022, the company has raised prices for specific products in different regions, and the profitability in 2023 has begun to stabilize and rebound, with a year-on-year increase of 19.5% in gross profit.

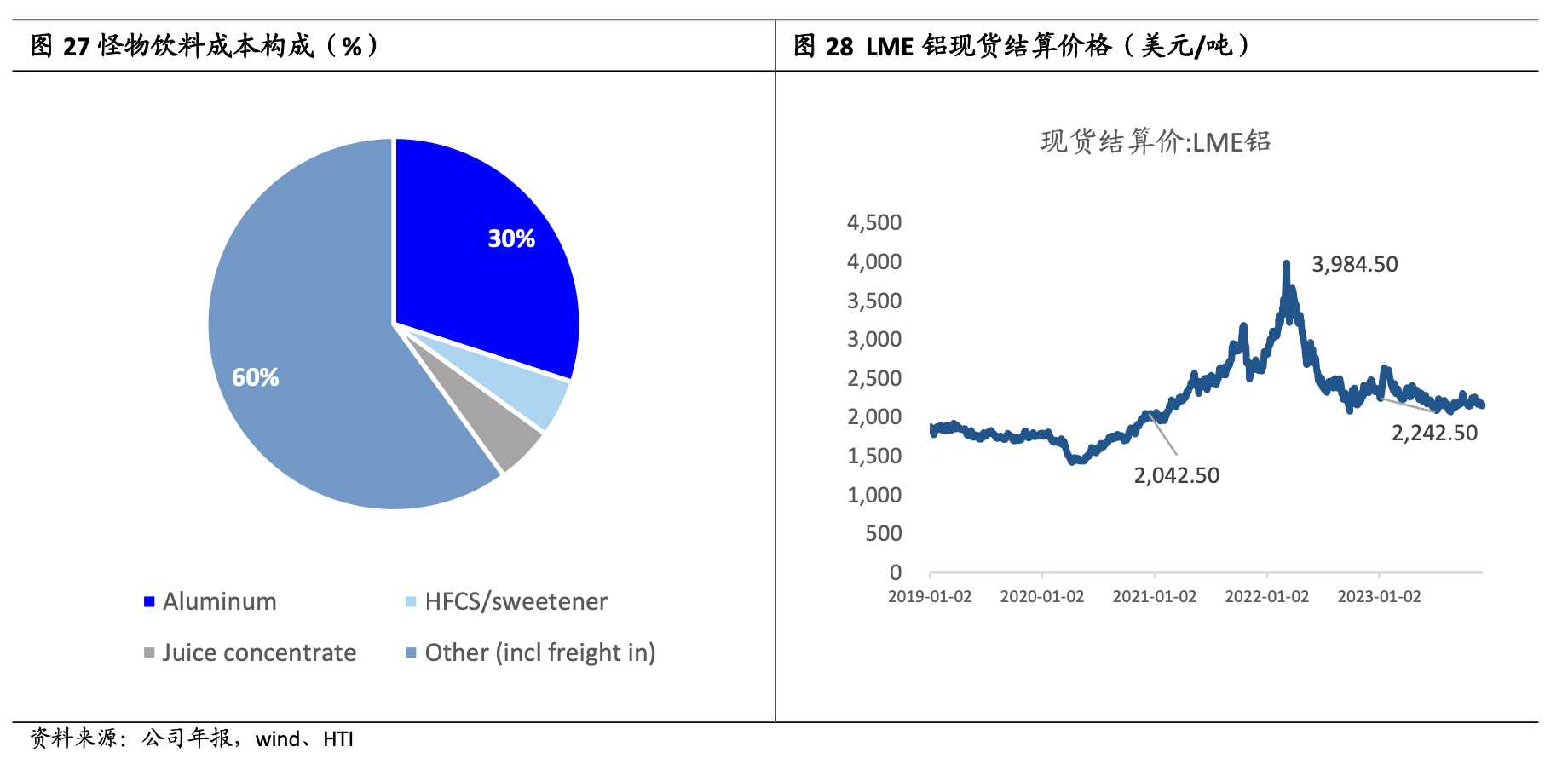

3) Cost structure - raw material dependence on imports

Monster only purchases raw materials (aluminum cans, juice, sugar, additives, etc.) and transports them to third-party bottlers and packers for the production, bottling, and packaging of finished products.

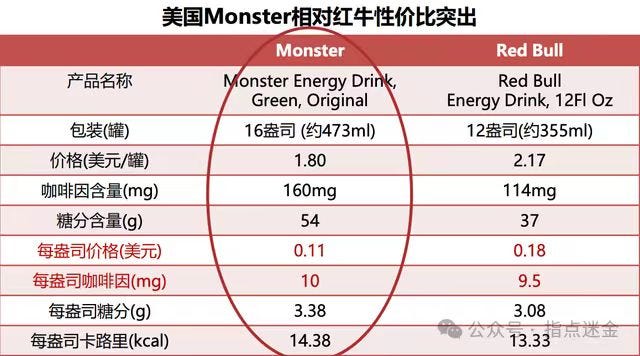

4) Operating expenses

In terms of management expenses, the company has remained relatively stable, usually fluctuating between 10% and 11%. However, sales expenses have shown a downward trend. In 2020, due to the impact of Covid-19, advertising activities were significantly reduced, and sales expenses dropped to 9%, which is 2pct lower than the historical average of 11%. As for transportation costs, from 2021 to 2022, due to global supply chain issues and inflation, the company faced challenges such as container shortages and port congestion, and had to turn to expensive air transportation methods, resulting in a significant increase in distribution costs.

5. Investment Thesis:

3.1 Brand (why Monsters can always exist))

1)Product competitive advantage-counter positioning. The company launched a 16-ounce product with a price similar to the Red Bull 8.4-ounce product.

Differentiated positioning refers to the company's products avoiding the product positioning of leading companies. For example, Red Bull positions itself in the mid-to-high-end market and has smaller cans, while Monster innovatively chooses the 16-ounce differentiated market to weaken direct competition with Red Bull. With large packaging and low unit prices, it successfully breaks away from competition with Red Bull.

2)Brand Moat: Strongly bound to the extreme sports market (especially with the brand perception of "claws" ), forming an entry barrier and not being affected by small brand energy drinks

It is clear that as a special category in the beverage industry, energy drinks have relatively small barriers in production technology, but the leading companies in the industry rely not only on the taste of the product itself, but also pay more attention to the psychological resonance and value recognition of consumers. Therefore, Monster has thousands of user loyalty, brand stickiness, and high consumption frequency as a competitive barrier.

3)Packaging differentiation:

Logo 'Beast Claw', black + fluorescent green (dark style) appearance is obviously different from other energy drinks

4)Marketing strategies are closely tied to brand positioning and extreme sports

Monster excels in understanding and meeting the demands of its target consumers, employing a unique marketing strategy to avoid the high costs associated with mainstream advertising. Monster opts to sponsor some of the coolest events, focusing on thrilling activities like extreme off-road motorcycle races, freestyle motocross, Formula One racing, UFC mixed martial arts, skydiving, rock concerts, skateboarding, snowboarding, bull riding, and NASCAR, rather than traditional TV or magazine ads. This approach resonates with Monster's young, blue-collar demographic. By engaging in niche cultures and aligning with the rugged American spirit of toughness and resilience, Monster has cultivated a highly loyal fan base directly targeting its core consumers— the millennial generation in America, perfectly fitting into this fast-paced and adrenaline-fueled world.

5.2 Innovation and functional dependence have improved Re-purchase Rate and penetrated a wider range of customer groups, providing product services for more diverse customer needs

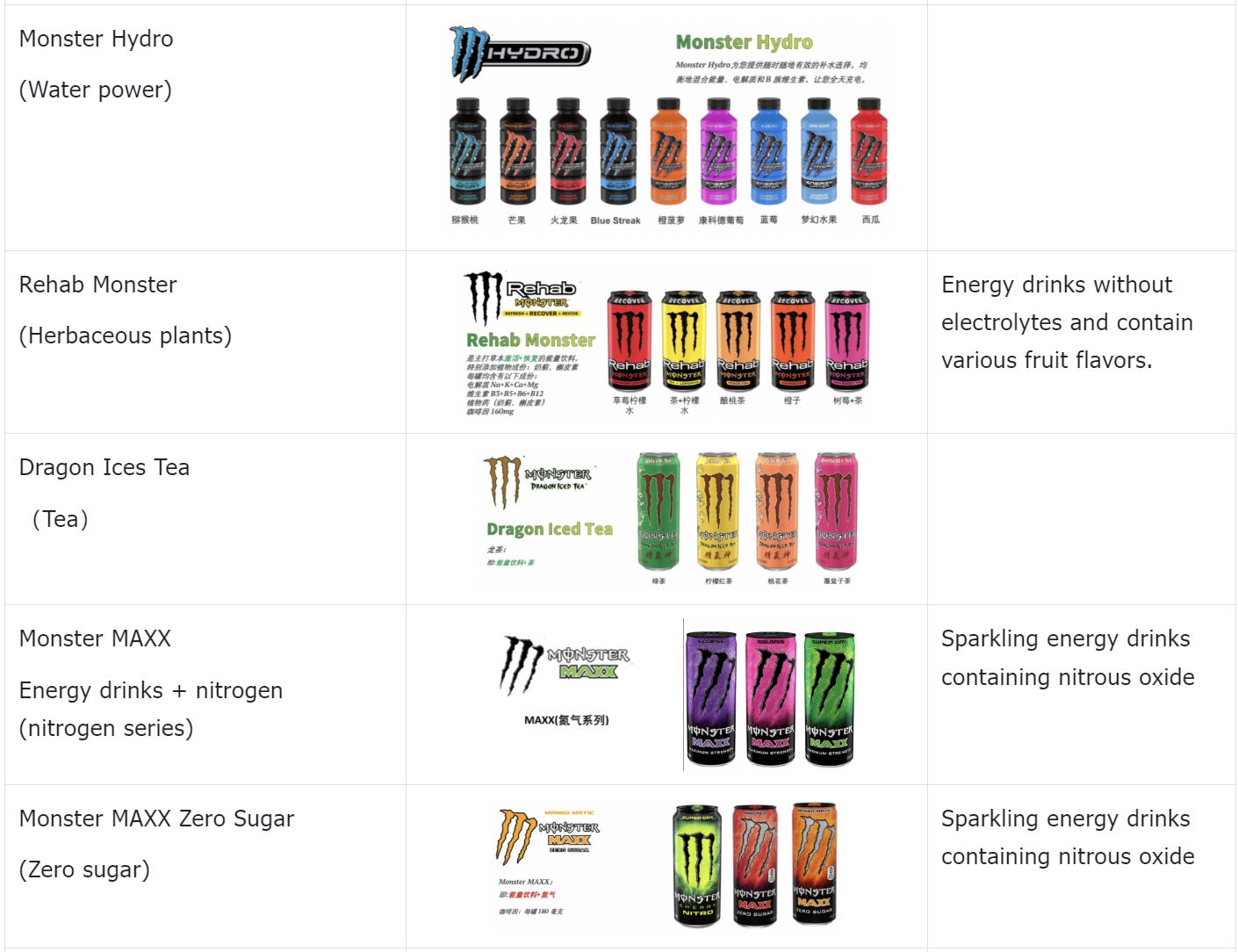

Each series has functional changes.

Monster Energy Drinks

Monster also reduces the threat of potential differentiated entrants by increasing new capacity to occupy shelf space and meet the needs of different usage scenarios in distribution channels.

Monster diversified its beverage flavors to break the monotony in the energy drink market compared to Red Bull. By introducing 1 to 4 new flavors annually, Monster aimed to cater to diverse consumer demands. Despite Red Bull's dominance in the U.S. market, its limited product range provided Monster with an opportunity to innovate. Monster followed three main principles in new product development: launching healthier options like low-sugar and zero-calorie series, adopting the "energy drink + X" model where X could be juice, coffee, ready-to-drink tea, or protein, to differentiate from existing products and minimize market share erosion. These strategies helped Monster achieve a leading position in the U.S. market.

Moreover, Monster's new product introductions drove revenue growth significantly. Nielsen data indicated that from 2010 to 2013, Monster's sales increased by 79%, with 72% of that growth attributed to products launched after 2010, such as zero-calorie options, ready-to-drink tea, and high-protein variants. This underscores the importance of ongoing innovation in enhancing customer retention and fostering growth.

5.3 Distribution channels: Light asset layout, often cooperate with local large beverage distributors in different markets to optimize their distribution network and market penetration rate. Leverage the distribution channels of giants to achieve rapid stocking.

The company has adopted a light asset model of outsourcing production and cooperative distribution, allowing it to focus more on marketing, branding, thereby promoting international expansion. In terms of distribution, the company adopts different partners in different regions: in Japan, Asahi Beer serves as a cooperative distributor; in the US and other regions, it relies on Coca-Cola as the main cooperative distributor.

Although Coca-Cola's sales channels are mainly concentrated in convenience stores, vending machines, Costco, and Sam's Club, there are still differences in the matching of sales channels. Therefore, Monster is also expanding potential sales channels such as gas stations, cinemas, nightclubs, car 4S stores, and industrial and mining enterprises, which are areas that Coca-Cola has less coverage in.

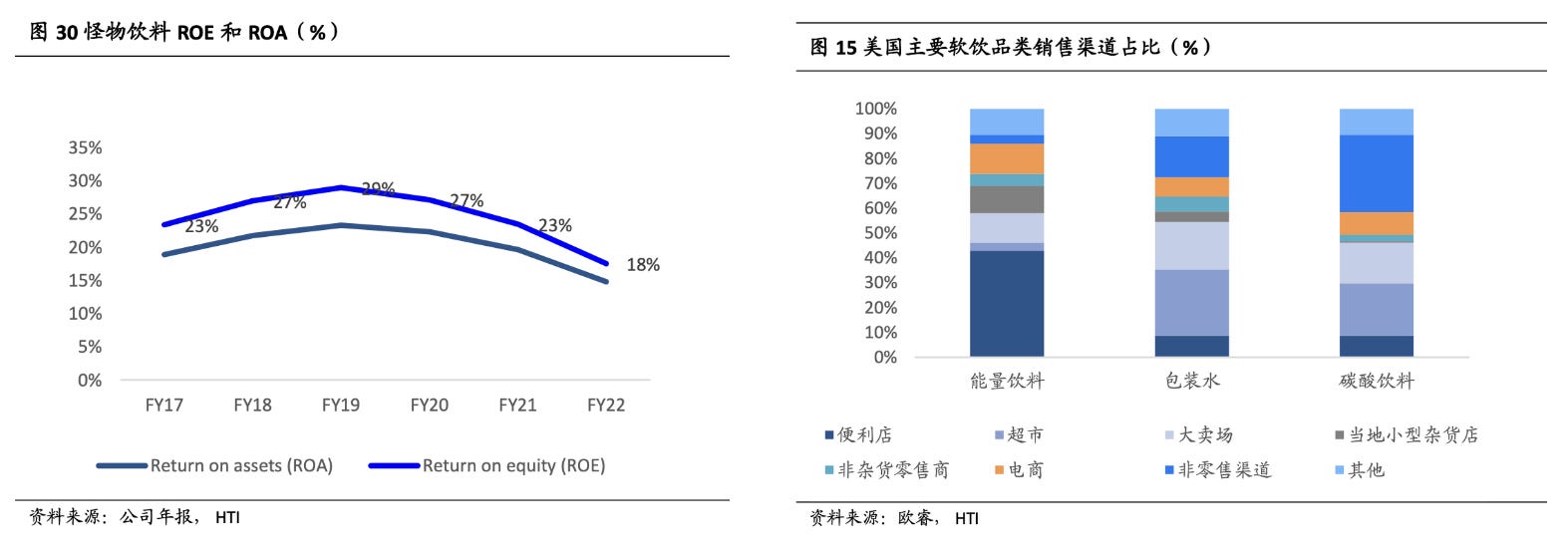

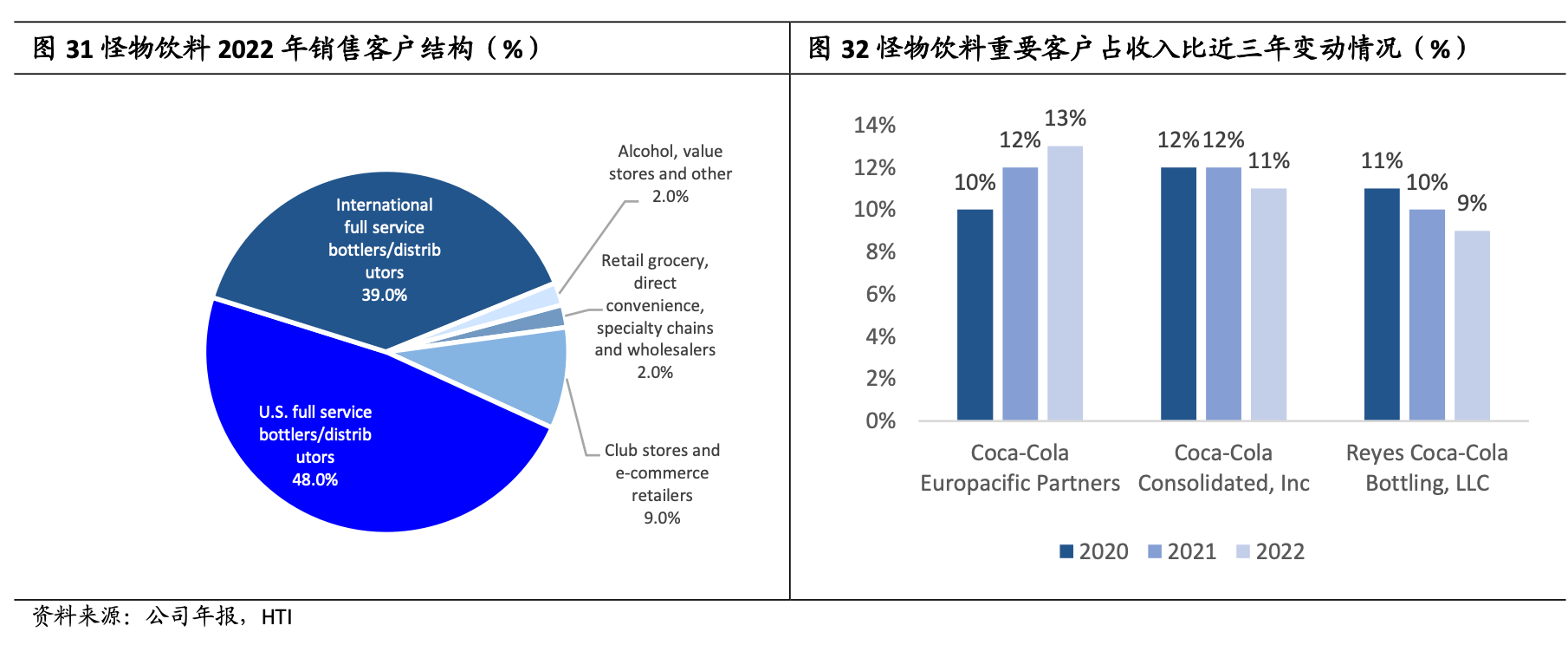

Monster's customer base is mainly Coca-Cola bottlers. This light asset operation model has enabled the company to maintain a high ROE. In 2022, 48% of Monster's sales came from US bottlers, 39% from international bottlers, and only 13% were directly retailed through channels such as e-commerce, club stores, and convenience stores.

Specific customers include:

Europe : Coca-Cola European Partnership (CCEP.US, 13% of revenue),

US : Coca-Cola bottling company (COKE.US, revenue accounted for 11%), Reyes Coca-Cola bottling plant (RCCB, revenue accounted for 9%) and other Coca-Cola bottling plants.

China : Monster's bottlers are Swire Coca-Cola and COFCO Coca-Cola.

5.4 The acquisition of fragrance suppliers guarantees taste exclusivity

Although the company also imports flavorings from other suppliers, acquiring AFF is crucial for protecting and innovating the core flavors of Monster beverages and for standardizing global taste profiles. The company has consistently used product innovation as a key strategy to compete with Red Bull, placing significant emphasis on the market rollout of new products.

This diversification allows Monster to continually expand the types of customer segments it serves and adapt its R&D to market trends and changing consumer preferences, providing greater flexibility.

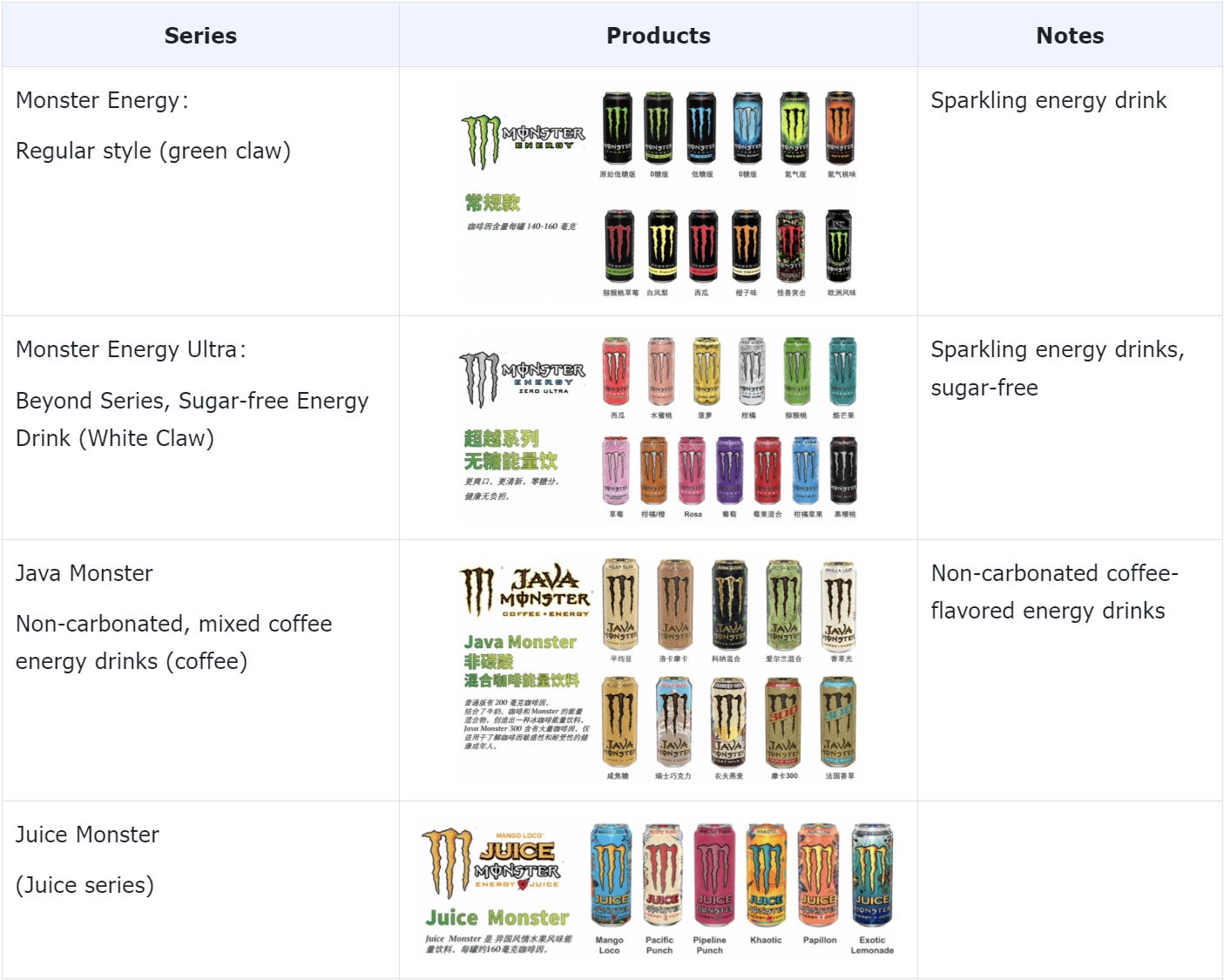

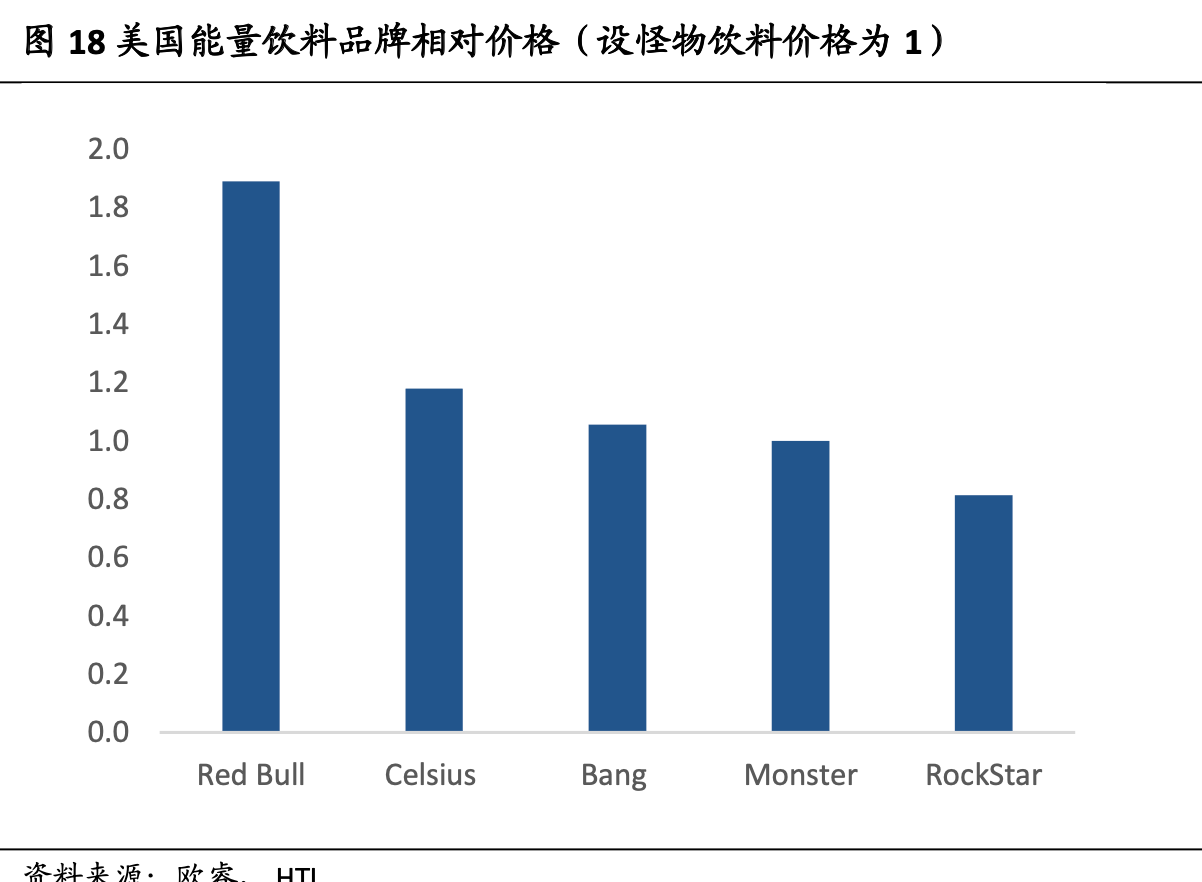

5.5 Other brand unit prices are at a high level, Monster is more cost-effective.

The overall pricing of top energy drink brands is relatively high. Red Bull targets labor and working people, and its average market price in 2023 is 1.9 times that of Monster. Although Monster's single can price is close to Red Bull, it maintains a high cost performance by increasing packaging capacity, surpassing Red Bull in sales volume, competing with it in sales, and quickly seizing the market.

Assuming Monster 1 unit price is 1 dollar:

6. Competitors

1) Fat-burning energy drinks grab the market

Celsius (CELH), as a challenger to Monster, focuses on the healthy concept of "0 sugar, 0 calories, 0 fat", emphasizing more natural nutrients and claiming to help burn fat. This "fat-burning healthy drink" positioning has opened up a unique market path for Celsius and caters to current consumer trends. In the past two years, Celsius has received investment and distribution support from Pepsi, seemingly replicating Monster's development path.

In the field of fat-burning beverages, Monster successfully acquired Bang in 2023. Bang focuses on the fitness and fat-burning niche market, and its different positioning and pricing strategy from Monster enriches Monster's product portfolio while resisting Celsius' attacks on the fat-burning beverage market. It is expected that this will bring greater brand growth space to Monster.

In the energy drink track where Monster is in (strongly tied to extreme sports), it maintains a monopoly position, making it difficult for competitors to enter its core customer base. Other brands mainly offer similar niche sports energy recovery drinks, with serious product homogenization and little difference in brand value. Therefore, I believe that emerging competitors will not pose a substantial threat to Monster.

At the same time, sponsoring major extreme events, music festivals, and E-sports competitions is an extremely expensive brand building project. The investment in these expenses and the first-hand advantage in consumer stickiness have set a relatively large threshold for potential entrants.

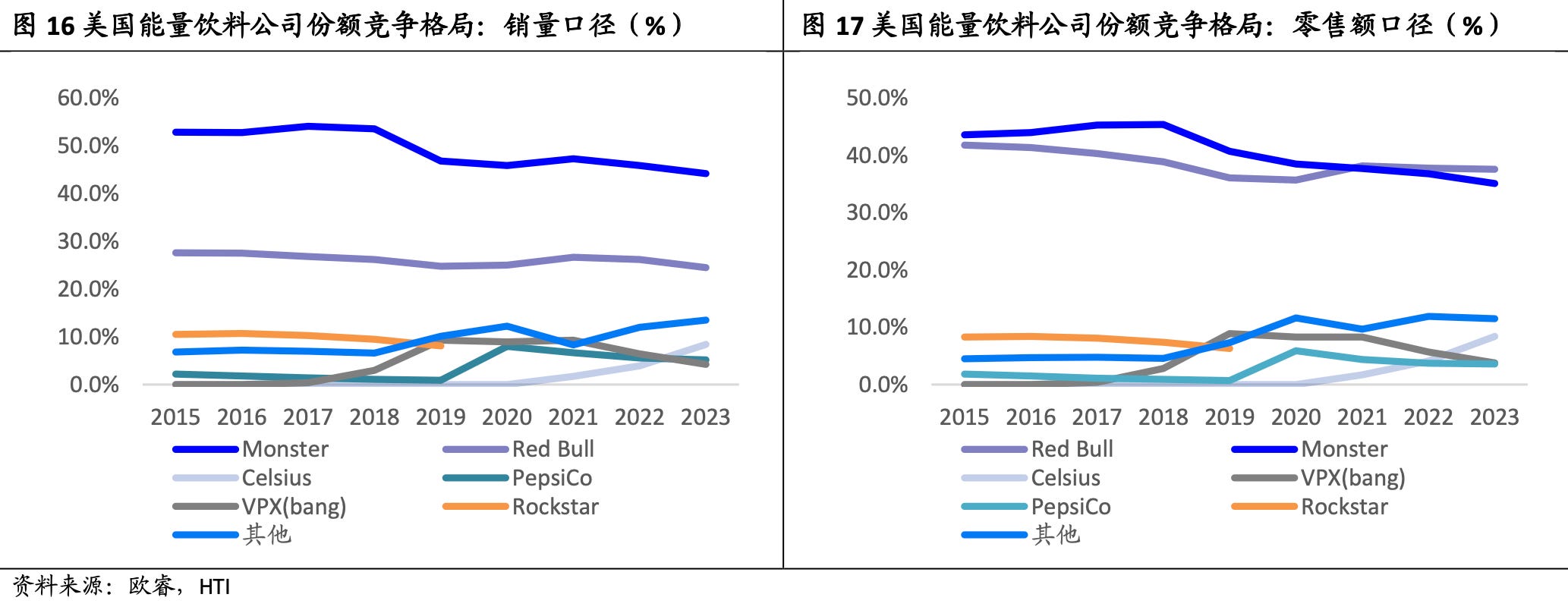

2)Monster and Red Bull are the US energy drink duopoly

In terms of volume, Monster held a 44.2% market share in 2023, significantly higher than Red Bull's 24.5%.

In terms of retail revenue, Red Bull and Monster had market shares of 37.6% and 35.1% respectively in 2023. The difference between the two is small, and both are much higher than other energy drink brands.

Between 2015 and 2020, Red Bull's market share declined each year. However, in 2021, Red Bull's market share rebounded, primarily due to the flexibility of its independent distribution system during the pandemic, which allowed for agile personnel management and adjustments in channel layout. Conversely, Monster’s market share decreased because many Coca-Cola bottlers faced labor shortages during inflationary periods. Red Bull’s own distribution network provided greater flexibility and resilience.

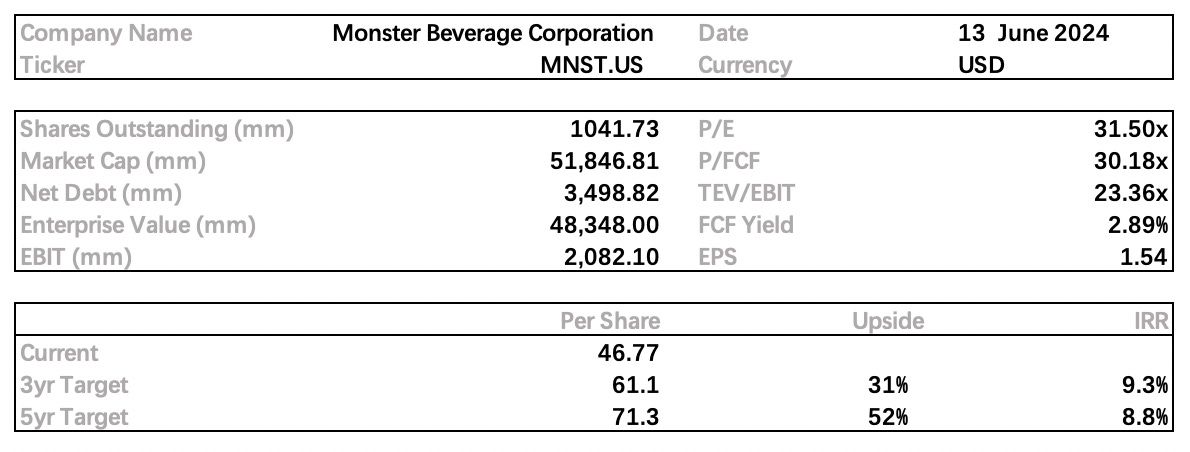

7. Valuation & Target Price

PE bands:

Target price:

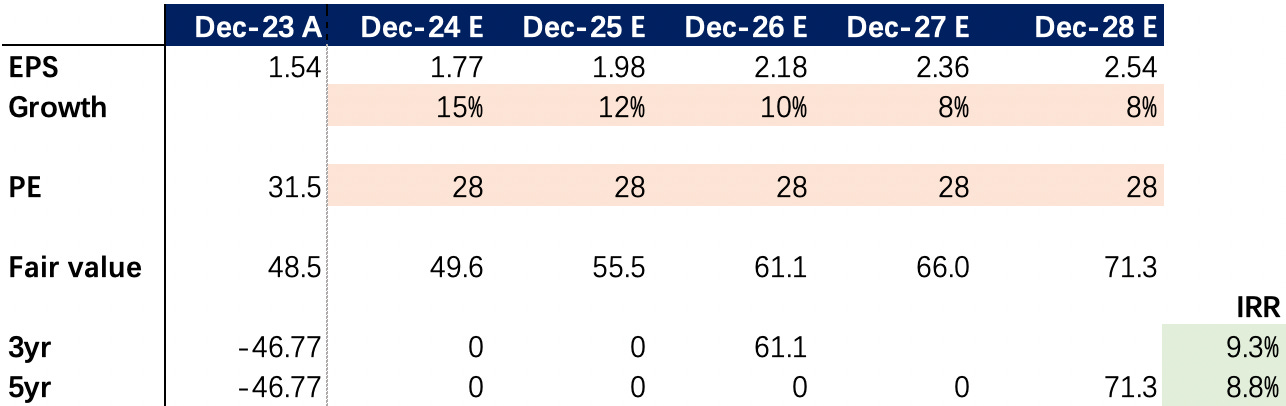

Setting a growth rate for the next 5 years at 15%, gradually decreasing to 8%, averaging a 2% decrease per year until it stabilizes at 8%.

As of December 31, 2023, with a PE ratio of 31.5x, Monster is relatively overvalued, so setting the expected PE ratio for the next five years at 28x.

Based on these, Monster's target price after 3 years is approximately $61.1, and after 5 years, it is expected to be $71.3.

8. Risks

1)Profits are easily affected by economic cycles, causing fluctuations

Monster needs to procure raw materials such as aluminum cans, fruit juice, sugar, and additives, and transport them to third-party factories—its Co-packers. This dependence makes the company susceptible to periodic supply chain disruptions. For instance, the rising costs of packaging materials like aluminum cans, as well as increased freight and fuel expenses, have an impact.

Due to the inflation and war in 2021, the prices of various commodities surged rapidly, including oil prices. Consequently, Monster was affected by the rising costs of aluminum, fuel, and freight. To address issues like aluminum can shortages, labor shortages, low freight efficiency, container shortages, and port congestion during 2021-2022, the company resorted to costly air freight to meet consumer demand, which further increased costs.

To mitigate these adverse impacts, Monster expanded its supplier base and managed raw material inventories more effectively.

2)Distribution channels rely on Coca-Cola distribution system, but are also limited by this

Red Bull’s independent distribution system proved more flexible during the pandemic, allowing for agile personnel management and adjustments in channel layout. In contrast, Monster's market share declined as many Coca-Cola bottlers experienced labor shortages during inflationary periods.

Labor shortages among Coca-Cola bottlers directly affected Monster’s market share. Insufficient labor led to reduced production and distribution efficiency, hindering the timely supply of products.

Coca-Cola may prioritize distributing its own branded products, potentially affecting Monster’s distribution priority within their channels. This could result in Monster being overlooked or receiving fewer promotional resources in certain markets and channels.

In dealing with rising costs (such as transportation and fuel expenses), Coca-Cola's distribution system might pass these increased costs onto Monster, leading to higher operational expenses for Monster. This further impacts Monster's price competitiveness and market performance.

9. Recommendation

Monster has entered a mature stage of corporate development, and currently, there are no significant growth drivers visible for the future. Monster heavily relies on Coca-Cola's bottling and distribution system, posing supply chain and cost risks.

If Monster begins to invest heavily in both the U.S. and international markets to establish its own distribution network, it might address these issues. However, expanding its distribution channels will increase CapEx, potentially affecting stock price volatility, but it will also lay the groundwork for penetrating more potential markets in the future.

Currently, Monster’s stock price remains relatively high, making it an unsuitable time to buy. It may be wise to wait for a more opportune moment to invest.

10. Summary

As a company that mainly sells ready-to-drink energy drinks to bottlers and distributors, Monster expands its scale and seizes market share by cooperating with Coca-Cola's leading companies through price differentiation, product diversification, and light asset allocation. It is also strongly bound to extreme sports events and continuously marketed, constantly appearing in the public eye to refresh memories.

Monster’s shift in its business strategy has been highly successful. Based on Monster’s experience, achieving growth requires first selecting a large market where the company can capture a substantial share, and having a unique entry point. Following this, the company should gradually expand its product lines and then move towards global market expansion.

However, there is an undeniable issue that Monster entered Capital Markets early on. Capital Markets witnessed Monster's growth from revenue of hundreds of millions to billions and market value from hundreds of millions to tens of billions. If it had not entered the market when the product was just starting out, or even before the development direction and core product were determined, we might not have seen this hundreds of times growth.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.