Initial Report: Alibaba Group (BABA), 98% 5-yr Potential Upside (China Tech Fund)

Seeing double? Let's see if you can spot the difference between China Tech Fund and VIP IC's analysis

Introduction to the Next Gen China Tech Fund

About

The inception of China Tech Fund was the shared idea between Shinya and Max while having a discussion about the exciting opportunity of the Chinese listed shares in the United States and Hong Kong. During these past two years, the Chinese government executed a total crackdown into the technology and real estate sector causing a hard deleveraging and share liquidation by foreign investors all around the world. The Hang Seng Index (HSI) fell approximately 50% and foreign investors totally lost confidence investing in the Chinese market. With the tightening of financial markets all around the world due to persistent high inflation, China remains firm on the decision to lower interest rate; however financial and psychological repercussions remain and market participation is fearful of allocating capital. With the previous successful execution of the inception of China 101010 Fund during the severe bear market during 2011-2012 period in China, China Tech Fund’s goal is to also replicate the success by capitalizing on the rare contrarian opportunity to buy into the highest quality internet technology companies in China and hopefully with a long term perspective (10 years) and patience to successfully compound capital by beating the benchmark indexes.

LinkedIn | Max Tai

Business Overview

Alibaba Group Holding Limited, through its subsidiaries, provides online and mobile commerce businesses in the People's Republic of China and internationally. It operates through four segments: core commerce, cloud computing, digital media and entertainment, and innovation initiatives and others. The company was founded in 1999 and is based in Hangzhou, The People's Republic of China. The company operates as Taobao Marketplace, a mobile commerce destination; Tmall, a third-party online and mobile commerce platform for brands and retailers; Alibaba Health Internet platforms for pharmaceutical and healthcare products; Alimama, a monetization platform; 1688.com and Alibaba.com, which are online wholesale marketplaces; AliExpress, a retail marketplace; Lazada, an e-commerce platform; and Tmall Global, an import e-commerce platform. It also operates Lingshoutong, a digital sourcing platform; Cainiao Network, a logistic services platform; Ele.me, a delivery and local services platform; Koubei, a restaurant and local services guide platform; and Fliggy, an online travel platform. The company also provides pay-for-performance and display marketing services, as well as the Taobao Ad Network and Exchange, a real-time bidding online marketing exchange. Further, Alibaba Cloud provides elastic computing, database, storage, virtualization network, large-scale computing, security, management and application, big data analytics, the Internet of Things, and other services for enterprises; payment and escrow services; and movies, television series, variety shows, animations, and other video content. Additionally, the company operates Youku, an online video platform; Alibaba Pictures and other content platforms that provide online videos, films, live events, news feeds, literature, music, and others; Amap, a mobile digital map, navigation, and real-time traffic information app; DingTalk, a business efficiency app; and Tmall Genie, an AI-powered smart speaker.

Industry Overview

The Chinese retail industry is highly fragmented, consisting of a large number of small and medium-sized retailers. Rental expenses in China are also more than 10% of the total costs of operating the business, and some command an even higher rate; thus, operating through e-commerce provides better cost savings and efficiency. This is unlike the U.S., where certain chains including Wal-Mart, Costco, and Target dominate most of the market. Although retail chains have expanded in recent years in China, the market still remains fragmented. This presents a strong opportunity for Alibaba, with little resistance from others as there is no single chain large enough to challenge its advance. This further contributes to sellers preferring to sell through online channels and advertising on Alibaba. According to the World Bank, there were 600 million rural residents in China in 2020, accounting for 40% of the total population in the country. Rural residents' average consumption level is RMB 12K per year, compared to the level of urban residence in 2009; e-commerce penetration in rural areas is also growing faster than in urban areas.

Investment Thesis

China Retail

China has been the largest grocery market in the world for a few years now, edging out the U.S. in terms of the total market size. The market is also expected to grow at a higher rate than in the U.S. to become a $1.6 trillion market by 2022. Sun Art was the largest operator of supermarkets and hypermarkets in China, with around 450 stores across 30 provinces under the banners Auchan and RT-Mart. The Chinese retail industry is highly fragmented, comprising a large number of small and medium-sized retailers. This is unlike the U.S., where certain chains including Wal-Mart, Costco, and Target dominate most of the market. Although retail chains have expanded in recent years in China, the market still remains fragmented. This presents a strong opportunity for Alibaba, with little resistance from others as there is no single chain large enough to challenge its advance. Alibaba will likely remain insulated from foreign competition disrupting its domestic addressable market due to the nature of regulations in China.

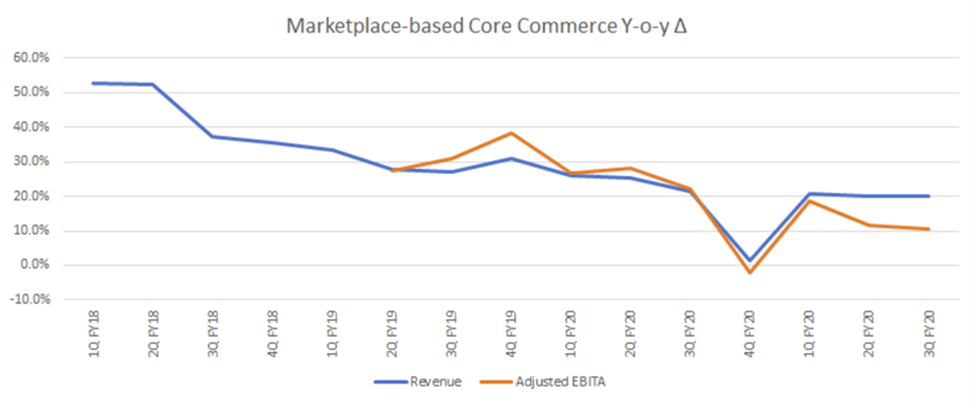

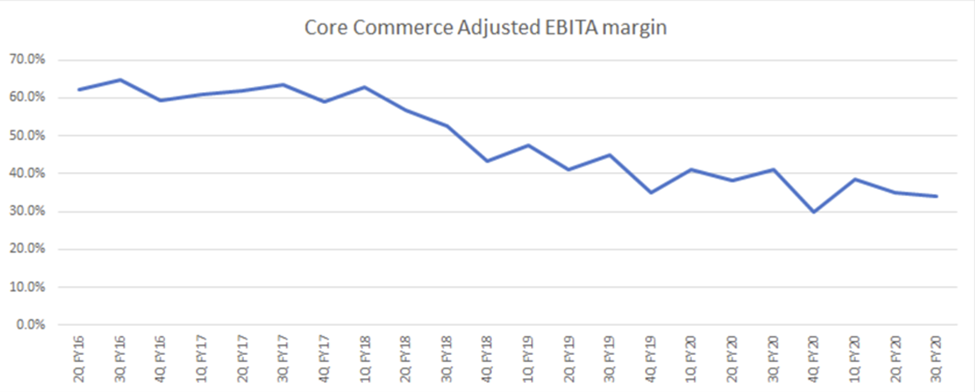

During 2022, Alibaba’s largest revenue contributor China Retail revenue grew 18% year on year in comparison to Y2021. Alibaba is prioritizing long-term growth over short-term profitability in 2022. Alibabawill continue to invest in new businesses to penetrate lower-tier cities via Taobao Grocery and Taobao Deals. Grocery is an over RMB 2T ($300B) market with online penetration of only 5%. Alibaba is tapping into the e-grocery market with different models (Hema, Taoxianda, and Ele.me) and investing in community group purchase start-up Nice Tuan. BABA already operates various types of offline stores, including Intime, Sun Art, Hema, and Cainiao Posts, and knows the grocery supply chain. It has a proven track record of converting loss-making businesses to profitability over time (e.g. cloud), and prioritizing long-term growth over short-term profitability. For Taobao Grocery, the key competitive edges of BABA are wide product selection across fresh and FMCG, as well as technological strengths in logistics and fulfillment. Community group purchasing is in the early stages of development, and Taobao Grocery could benefit from the Taobao app with increased usage frequency. Taobao Grocery, Taobao Deals, neighborhood shopping, and other new businesses are in investment mode. Meanwhile, expect BABA to invest in other strategic areas such as geographical expansion in local services and Lazada for the long term.

Cloud Computing

The cloud computing business has become one of Alibaba’s most promising revenue resources, riding on the established IaaS service of Alibaba and expanding cloud computing needs in the real economy. AliCloud experienced revenue growth of approximately 20% during the financial year 2022 and recorded a net revenue of RMB 74 billion in FY2022. Contributing to Alibaba’s revenue, cloud computing revenue grew 25% YoY in FY2022, which represented about 9% of total revenue. China’s contribution to world GDP reached 16% in 2018, but IT expenditure only represented less than 5%, indicating the imbalance between economy growth and enterprise information technology levels. China's cloud computing industry market size is growing at a CAGR of 26%, reaching approximately RMB 200 billion in 2022. Alibaba is currently the largest IaaS market player in China, representing over 40 percent of market share in 2022. Compared to IaaS and SaaS, Platform as a Service (PaaS) is still the smallest in scale. Market demand from the real economy and government promotions will cause China's cloud computing industry to continue to grow strongly. Expect to see further increases in IT expenditure from SOEs, private enterprises, and government agencies. New technologies such as cloud computing, AI, and big data will enrich the application scenarios.

COVID-19 has impacted the cloud industry, especially in 2020, from delaying contract winning and renewal to delaying project implementation and revenue recognition for both software and cloud projects. However, the impact has been gradually reduced, with the YoY decrease for software revenue slowing while the YoY growth for cloud revenue accelerates. The remote work demand has benefited cloud/SaaS companies by migrating offline workflows onto the cloud, and with the gradual resumption of offline sales projects, expect many software companies’ strong contract liabilities for cloud service to be fully reflected in cloud revenue growth in FY22. The cloud migration will be a multi-year trend driven by: (1) a rebounding IT budget in 2022; (2) digitisation demand across industries, particularly driven by business continuity and COVID-19; (3) government policy support, particularly the new infrastructure initiative during the 14th 5-year plan; and (4) preferential tax treatment.The COVID-19 pandemic has led to accelerated digitization and a shorter cycle of cloud adoption for many businesses, especially SMEs.

International Wholesale

The secular trend of consumers shifting to the Internet for shopping has been the biggest driver behind Alibaba's marketplaces, including AliExpress, which serves international customers and lets them buy goods from Chinese manufacturers. With growing Internet penetration, low-income groups are also moving towards online purchases. Recent reports that Alibaba could set up a global version of its C2C marketplace Taobao could accelerate its push into international markets. Alibaba is already positioned among the top e-commerce players in Russia and Brazil. And its recent investment in Paytm (an Indian mobile commerce player) will further accelerate its growth in the future. AliExpress is witnessing growth in the number of buyers from countries such as Russia, Brazil, and the United States, which is driving strong growth in the platform's gross merchandise volume (GMV). This suggests that there is an uptick in demand for Chinese products in international markets. While quality concerns may remain, there is a strong cost advantage to buying products from China, which is attracting buyers from all over the world. AliExpress has made it easy for Chinese manufacturers to export internationally. This will continue to drive growth in the marketplace GMV, and hence in Alibaba's international retail commerce revenues. The Lazada acquisition gives Alibaba a strong foothold in Southeast Asia. Lazada is the market leader in Indonesia, Malaysia, Singapore, the Philippines, and Thailand. Southeast Asia has a combined population base of 560 million, with over 200 million internet users. Lazada, Alibaba’s Southeast Asian e-commerce platform, continued to achieve robust growth in buyers and sellers and to benefit from the acceleration of digitalization across industries in Southeast Asia. Despite new waves of COVID-19 in many markets, order volume grew 100% Y/Y for the year and International Wholesale revenue grew approximately 30%.

Ant Group

Ant has agreed with the financial regulators to restructure into a financial holding company, which will almost certainly require it to hold more equity against the loans it originates. There are other details too, such as "removing the improper connection between Alipay and financial products like Huabei and Jiebei" and "breaking Ant’s information which imply a profound and qualitative change to Ant’s business model. These will surely lower Ant’s prospective valuation and thus the value of Alibaba’s 33% interest. Tighter lending could also impact consumers’ willingness and ability to spend on Alibaba’s marketplaces. following a second meeting with Ant Financial in late December. Regulators put forward five regulatory requirements, including setting up a holding company for Ant's financial businesses, which would be regulated similarly to a bank requiring more reserve capital, lowering Ant's valuation to $60B. Five regulatory requirements. 1) Focus on payment business, improve transactions' transparency, and promote fair competition; 2) obtain necessary licenses for its individual credit rating business and protect consumers' data; 3) set up a holding company for its financial services (credit, insurance, and asset management) with adequate reserve capital; 4) improve company governance; and 5) correct irregularities in asset securitization businesses.

Future competitive strategy

Alibaba Group Holding (Alibaba) announced that it will waive some marketing tool fees for merchants. This is aimed at helping merchants improve ROI and enhance operating efficiency on their platform. In order to acquire new merchants and retain existing ones, management stated that it will continue to focus on assisting merchants in optimizing operating costs and lowering entry barriers for doing business on its platform. In the future, increasing numbers of mature marketing tools are to be offered for free for merchants to support their business operations, according to management, which could, in our view, enhance Alibaba’s market leadership and fuel long-term revenue growth. Diverse product offerings to aid merchant revenue growth Alibaba has a diverse product portfolio to aid the business development of merchants on its Taobao and Tmall platforms and help merchants better reach potential customers, backed by its technological capabilities. The long-term trend of improving monetization rates remains intact. Fee waivers could propel more merchants to use Alibaba’s services offerings and help merchants conduct business more efficiently on its platform, which, in our view, could help convert more paying merchants for advanced packages and for other services offerings. Alibaba has established infrastructure capabilities that can help merchants improve efficiency and achieve sustainable margins, which could support long-term monetization expansion. Commissions on transactions, where merchants pay a commission based on a percentage of transaction value generated on Tmall and certain other marketplaces. The commission percentages on Tmall typically range from 0.3% to 5.0% depending on the product category.

Alibaba intends to continue investing in new businesses to penetrate lower-tier cities via Taobao Grocery and Taobao Deals. It has a proven track record of converting loss-making businesses to profitability over time, such as the cloud, by prioritizing long-term growth over short-term profitability. For Taobao Grocery, we consider the key competitive edges of BABA to be wide product selection across fresh and FMCG, as well as technological strengths in logistics and fulfillment. Community group purchasing is in the early stages of development, and Taobao Grocery could benefit from the Taobao app with increased usage frequency. We view Taobao Grocery, Taobao Deals, neighborhood shopping, and other new businesses as in investment mode. On the other hand, we expect BABA to invest in other strategic areas such as geographical expansion in local services and Lazada for the long term. FY22 will be a year of investment. In its earnings call, management iterated that it will invest aggressively in new initiatives, focusing on Taobao Grocery, Taobao Deal, and Eleme. (1) Groceries initiatives: The recent formation of the MMC segment and the new leader's appointment showcased Baba's commitment to the CGP Taobao Grocery business. Over RMB 20 billion in investment is being benchmarked against competitors. The Taobao deal will also have a margin drag on user acquisition. (2) Local service: Eleme onboarded more quality restaurants with the COVID situation and antitrust limits on the "2-select-1" practice, making the platform better positioned to acquire new users. Hence, expect more investment for user acquisition and retention.

Valuation

Currently, Alibaba Group Holdings is trading at an extremely undervalued price of HKD 110 with a market capitalization of approximately USD 330 Billion. With the continuous slowdown but still fast growth of mature technology companies having a PE Ratio of 25x and forward PE Ratio of lower than 20x. By using a SOTP analysis on different segments of Alibaba business we can value the business as a whole clearer. Ant Financial value has decreased from USD 300 Billion to USD 60 Billion thus with a 33% stake in Ant Group the value of the stake to Alibaba is at around USD 20 Billion through SOTP analysis. By evaluating it using the bear case scenario. The potential upside for Alibaba’s at almost 100% from current share price.

Regulatory Setbacks, Risks and Future Potential Effects

In the case of Alibaba, the key source document is the State Administration for Market Regulation Guidelines for Anti-Monopoly in the Platform Economy Draft, released in November 2020, which triggered a flurry of activity and no shortage of panic. In April 2021, the company was fined US$2.8 billion for breaching regulations. By July, Alibaba and Tencent faced the possibility of opening up their services. Tencent was also asked to retract its exclusive music rights. Concerned that these giants were using their market dominance to stifle competition, in August new drafted rules were released. On November 3, 2020, the IPO of Alibaba-owned Ant Group was suspended and the decline in Alibaba’s share price accelerated, assisted by concerns over the ADR and VIE structures and a slowing Chinese economy. With Alibaba missing its earnings targets, brokers slashed their forecasts.

China likes to fix the roof when the sun is shining. Right now, rain is falling. Although monetary and fiscal easing in the coming months, the macro environment is challenging. This makes further action even less likely. Regulators are also signaling they’re moving on. The deputy head of SAMR recently said the practice of small merchants having to pick either Tencent or Alibaba as their online store has "basically disappeared." Tencent and Alibaba are also making moves to divest parts of their empires to satisfy regulators' concerns. The resources released should accelerate domestic innovation and allow more investment in overseas businesses, which are already growing rapidly. Such decisions are likely to be viewed favorably by regulators. With the Securities Regulatory Commission saying it "respects" where Chinese companies seek to list, delisting fears are also overstated.

Beyond these concerns, there looms a bigger issue. If China is to achieve the goals of common prosperity outlined in the speech by Xi Jinping last August (To Firmly Drive Common Prosperity), Alibaba is more of a partner than a target. To assist in controlling prices and getting food to people, the regulator has asked ecommerce and delivery platforms to help support the city, thus proving their might. The objectives of common prosperity imply a collaboration between the state and big tech rather than an adversarial one. If China’s long-term growth trajectory is to continue through the development of a larger, consumption-based economy and an expanding middle class, Alibaba is less of an obstacle than a key player. As evidence, consider the company’s pre-eminence in e-commerce. Through Tmall and Taobao, Alibaba is responsible for almost half of China’s e-commerce activity. With 950 million users and 1.24 billion annual active customers generating US$1.2 trillion in gross merchandise value, the company has an expanding range of alluring mousetraps. To meet the GDP and income growth objectives, these numbers are more likely to expand than shrink. Innovative ideas like Taobao Deals and group buying are engines for disposable income growth. Deals allow customers to receive goods directly from factories in just 24 hours.

Rural expansion Community group buying is also taking off in rural areas. With a population of 400-500 million, many of whom are underserved, rural expansion offers much growth potential for Alibaba. Rural Taobao is another example. Since 2014, it has successfully expanded access to rural areas. Research from the World Bank and Alibaba says that "E-commerce is associated with increased growth, income, and employment in rural communities." The government presumably wants to see programmes like this expand to meet its common prosperity goals. One must also consider the extent of the company’s e-commerce ecosystem. From payments, logistics, local services, food delivery, on-demand delivery, core ecommerce, healthcare, and finance, Alibaba is everywhere in the value chain. The stickiness of this network Alibaba’s retention rates are extraordinarily high, is underappreciated and, at current prices, is undervalued. Even if this segment of Alibaba grows at 10% per year over the long term with lower EBITDA margins, it will be worth at least US$200 billion in a decade. The company has also successfully exported its knowledge to overseas markets. Alibaba-owned Lazada operates the second-biggest ecommerce market in Southeast Asia. Alibaba recently announced the goal of becoming number one, aiming to service over 300 million customers and generate a GMV of US$100 billion. The company is also expanding in Europe, and the AliExpress mobile app is already the most popular in Russia.

As Facebook and Google have proved, it is natural for software companies to expand from one jurisdiction to the next. China’s regulators want its big tech companies to become dominant overseas. Then there is Alibaba Cloud. Already the biggest service in China, it is spreading across Asia, growing revenue at about 50% a year. With the development of its own server CPUs and domestic and international expansion, it is conservatively worth around US$40 billion, and potentially far more. As for Ant Financial, it facilitates about a fifth of China’s unsecured consumer debt. Although this will be difficult to expand given the new capital requirements, the availability of credit is central to the kind of consumer-based society China wants to build. Still, Ant has been damaged by regulatory action. The attempted listing was believed to be at a valuation of over US$300 billion. The tendency for investors to concentrate on short-term perceived threats at the expense of a longer-term perspective on the assessment of Alibaba’s intrinsic value in the bear case and its current market capitalization. With the company calling 2022 an investment year, do not expect much growth. Indeed, the upcoming earnings will likely disappoint. But expect the investments the company is making to pay off, especially now that the regulatory impacts are ameliorating. The risks of further action and, indeed, a deteriorating Chinese economy, are already reflected in the share price.

Financials and Balance Sheet

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.