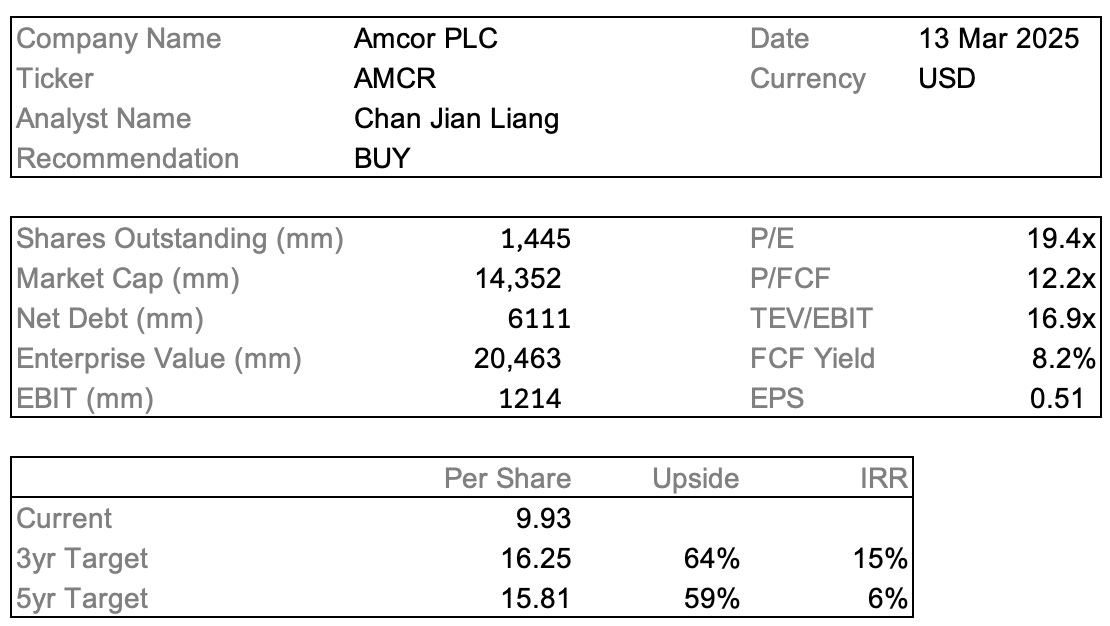

Initial Report: Amcor PLC (NYSE: AMCR), 59% 5-yr Potential Upside (CHAN Jian Liang, EIP)

CHAN Jian Liang presents a "BUY" recommendation for Amcor PLC based on its strong market position, innovative R&D capabilities, and strategic growth initiatives.

Note: The 3-year target price is higher than the 5-year target due to the initial momentum from Amcor’s merger with Berry Global. I expect that after three years, Amcor will reach a more stable growth phase, leading to a more moderated valuation beyond that period.

Executive Summary

Amcor plc (NYSE: AMCR), a global leader in sustainable packaging solutions, is recommended as a BUY due to its strong market position, innovative R&D capabilities, and strategic growth initiatives. Despite recent revenue challenges caused by destocking trends in the healthcare and beverage industries, these trends are expected to normalize by the end of FY2024, positioning Amcor for recovery and growth. The company’s merger with Berry Global enhances its leadership in sustainable packaging, unlocking $650 million in synergies and expanding its market share. Amcor’s commitment to sustainability, including achieving net-zero emissions by 2050 and making all packaging recyclable or reusable by 2025, further solidifies its competitive advantage. A standalone DCF valuation implies a share price of $15.81 (59% upside), reflecting significant growth potential. With robust ESG practices and a well-balanced capital allocation strategy, Amcor is strategically positioned for long-term value creation.

Amcor’s Business Operation

How Amcor approaches its Responsible Packaging is through the roadmap above.

Amcor operates a comprehensive packaging business that spans the entire value chain, from sourcing raw materials to waste management. The company sources materials and services from more than 36,000 suppliers worldwide, ensuring a steady supply chain. Through innovation and design, Amcor develops sustainable packaging solutions, with 89% of its flexible packaging portfolio having recycle-ready options and 95% of its rigid packaging being widely recyclable (according to 2023 figures). In manufacturing and operations, the company prioritizes environmental responsibility, implementing the Operation Clean Sweep methodology (a global program helping plastic resin handlers achieve zero plastic resin loss) at all sites using plastic pellets, powders, or flakes to prevent pollution. Amcor's customer packaging solutions ensure that products remain protected across complex distribution and retail channels. Additionally, the company actively engages in consumer education on recycling, participating in over 75 partnerships to promote a circular economy for packaging. Finally, Amcor collaborates across industries to improve waste management infrastructure, expanding strategic partnerships with Delterra, Mars, and P&G to provide recycling access to 10 million people and securing thousands of tons of certified-circular chemically recycled materials to drive sustainability forward.

Business Segments

Amcor has 2 main business segments: Flexibles and Rigid Packaging.

Flexibles Segment

The Flexibles segment develops and supplies packaging solutions, including Specialty Cartons, designed to cater to a wide range of industries globally. It is one of the world's largest suppliers of polymer resin (plastics), aluminum, and fiber-based flexible packaging, reinforcing its strong market presence. As of June 30, 2024, this segment employed approximately 35,000 employees across 160 significant manufacturing and support facilities in 36 countries.

Rigid Packaging Segment

The Rigid Packaging segment focuses on manufacturing rigid packaging containers and related products, including Closures, primarily for the Americas market. As of June 30, 2024, it operated with approximately 5,000 employees across 52 significant manufacturing and support facilities in 11 countries.

Based off its FY2024 Annual Report, Flexibles accounted for 76% of total net sales while Rigid Packaging accounted for the remaining 24%.

One notable note is that Amcor did not have sales to a single customer that exceeded 10% of consolidated net sales in the last 3 fiscal years. This is a positive indicator of diversification, as it suggests that Amcor is not overly reliant on any one client for its revenue. This reduces the risk of significant financial impact if a major customer reduces orders or terminates a contract.

Past 3 years Revenue Growth Rate by Geographic Distribution

Across all the countries for the “Flexibles” segment, the revenue growth rate has largely fallen to negatives significantly because of a global destocking trend in the healthcare industry (Hejl, 2025). This was also evident in the case of another organisation, named West Pharma, which mentioned that biotech clients have been depleting inventories that were built up during the pandemic-era supply chain disruptions (Reuters, 2025). This means that the revenue being affected was not a result of Amcor’s products or services, but rather a consequence from a market downturn.

Across the North America and Latin America for “Rigid Packaging” segment, revenue has fallen for North America due to a fall in overall North American beverage volumes that are discretionary beverages, which the fall reflects a combination of lower consumer demand and significant destocking that happened in the first half of the year. Evidence of this could be seen in the US Beverage alcohol market that faced headwinds in 2023, including imbalanced inventories and economic pressures on consumers (IWSR, 2024). However, despite the fall in Revenue for both Segments, I believe there will be an improvement for demand for the healthcare industry and beverage industry in future.

Revenue Split by Industries

68% of Amcor’s FY2024 net sales is attributed to Food (44%) & Beverage (24%), and the third highest industry attributed to 14% of its net sales is Healthcare.

Despite the destocking trend that happened significantly during FY2024 for Healthcare and Beverage, it is believed that the destocking trend has already ended by end of 2024.

Research suggests that inventory levels are expected to be normalised across end markets – namely food, beverage, beauty and personal care, and health and household — by the end of 2024 (Henkes et al., 2024).

For Healthcare, the life science tools industry, which provides equipment and technologies for drug research and development, and contract research organizations (CROs), which conduct clinical trials for pharmaceutical companies, are showing signs of recovery. Post-COVID inventory reductions in these sectors are nearing completion, and the biotech capital market, which funds innovative drug development and medical advancements, is rebounding. At the same time, the regulatory environment remains supportive, with the FDA continuing to approve new drugs and medical devices at a high rate. These factors reinforce the view that destocking in Healthcare is over and demand is stabilizing (Stephenson, 2024)

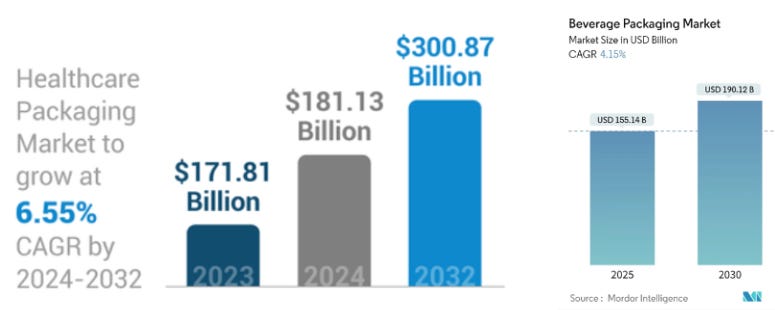

Growth of Healthcare Packaging and Beverage Packaging market

For the Healthcare packaging market, it is expected to grow at a CAGR of 6.55% from 2024 to 2032. This market is very important in the world due to the global Aging population and relevance of chronic diseases. With significant increase in the number of elderly individuals (Fortune Business Insights, 2025) and a rise in chronic diseases (Hacker, 2024), long term medication is essential and these oftentimes require healthcare packaging solutions that cater to the needs of the elderly. These require easy-to-open packaging, and chronic diseases would require specialized packaging that can maintain the stability and efficacy of medications over extended periods. whereas for the Beverage packaging market, its expected CAGR is 4.15% from 2025 to 2030. The Beverage industry is undergoing significant transformation where companies are increasingly adopting eco-friendly beverage packaging solutions, with a particular focus on recyclable materials and reduced plastic usage (Mordor Intelligence, n.d.) The needs of the Healthcare and Beverage packaging market are able to be fulfilled by the services of Amcor plc.

Investment Thesis

1. Amcor’s merger with Berry Global would make Amcor be the Go-to market leader in using Sustainable Packaging solutions, with significant enhanced market share while improving operational efficiency and overall profitability.

In early January 2025, Amcor plc and Berry Global Group, Inc. (“Berry”) (NYSE: BERY), a leading manufacturer of sustainable packaging solutions, have announced a merger through an all-stock transaction (Berry shareholders will receive a fixed exchange ratio of 7.25 Amcor shares for each Berry share held upon closing), valued at USD$8.4 billion. Berry is also a global leader in innovative packaging solutions, particularly within the Healthcare packaging market, known for creating patient-centered packaging design and sustainable solutions in the healthcare market.

Operational Synergies

Amcor’s acquisition of Berry serves to be a complementary boost to their overall operational synergies, because Berry earns a higher revenue from its Rigid Packaging solutions (accounting for 56% of its net sales in fiscal year 2024) due to its significant containers and closures business whereas Amcor earns more from its Flexibles segment. This results in Amcor being able to boost its Rigid Packaging solutions segment’s revenue in future from adopting the best practices that Berry has. For Healthcare, Berry’s specialty containers business aligns well with Amcor’s Flexibles, enhancing its healthcare exposure through advanced multicomponent delivery systems. Berry’s regulatory expertise (due to its in-house FDA compliance, labelling verification, and material safety reviews) combined with Amcor’s strength in its R&D platforms will contribute to an estimated combined revenue towards the Healthcare market of USD$3 billion, marking the Healthcare market as the one with the highest margin to Amcor’s growth.

Besides Healthcare, the merger will also strengthen Amcor’s existing position in its other key categories including Protein, Pet Food, Liquids, Beauty & Personal Care, and Food Service, with an average growth rate of 4.42% across all the sectors by having greater ability to meet the needs of different markets through its greater offering of sustainability packaging solutions.

Berry’s portfolio also significantly complement and boost Amcor’s existing R&D platforms

From the image above, Berry's R&D focus on sustainable material science and the development of specific, innovative solutions in recyclability, lightweighting, PCR utilization, Fiber-based alternatives, and carbon footprint reduction offers a strong complementary synergy with Amcor's existing R&D platforms. This could enable Amcor to diversify its product offerings or enhance its existing product lines by integrating more sustainable features, improving recyclability, reducing material usage, lowering carbon emissions, and offering alternatives to traditional materials.

Besides the above mentioned, Berry has no presence in the North American beverage segment, making this a complementary acquisition with Amcor. Additionally, Berry’s closures business, which includes dispensing systems and pumps, strengthens Amcor’s portfolio—especially after divesting its Bericap joint venture stake. This strategic fit reinforces Amcor’s growth in high-value packaging solutions, making the acquisition highly attractive.

Financial Synergies

Amcor will hold approximately 63% of the combined company, whereas Berry Global will own 37%. The companies will have combined revenues of $24 billion and adjusted EBITDA of $4.3 billion.

Through its merger with Berry, Amcor expects to realize $530 million in cost-saving synergies by the end of Year 3, primarily driven by its Procurement efficiencies. Additionally, $60 million in incremental earnings will be generated from $280 million in new growth synergies (increased exposure to high-growth sectors, enhanced innovation capabilities, and a broader commercial platform). Another $60 million in financial synergies will stem from better access to working capital and reduced financing costs. These combined synergies result in a total of $650 million in run-rate synergies, which I believe will position Amcor to significantly reduce its cost of sales, improve operational efficiency, and achieve gross profit margins well above the current 20%

Comparing the current model to new model, despite the relatively similar ratio of annual cash flow : capital expenditure being 3x for both, the positive information to note is that Amcor’s dividend yield has decreased from 4-5% to 3-4% with higher EPS.

Under the new merged model, Amcor will be spending 2.5x to 3x more on acquisitions / share repurchases, meaning Amcor’s EPS and ROE will increase significantly. This can make the company appear more attractive to investors, improving its stock price. Also, by doing buybacks now, reducing equity (by buying back shares) increases the company’s debt-to-equity ratio, making Amcor look more leveraged. This can make it easier for Amcor to take on additional debt because lenders might view the company as more financially efficient and able to handle more leverage. A higher debt-to-equity ratio can also reduce the company’s cost of capital, making debt financing more attractive for acquisitions.

This means Amcor could be strategically positioning itself with more flexibility for future acquisitions. Repurchasing shares could help them manage their capital structure so they are better prepared to make an acquisition when the right opportunity arises.

With Amcor increasing both share buybacks and dividend allocations, capital appreciation and dividend payouts per share would increase due to fewer shares outstanding. As a result, total shareholder value will improve (from 10-15% to 13-18% per annum). With these, Amcor’s adjusted free cash flow has also increased to USD$952 million, up 12% from last year. In my opinion, Amcor’s capital allocation strategy balances share repurchases with a growing dividend. By buying back shares, Amcor reduces the number of shares outstanding, which increases earnings per share (EPS) and allows for a higher dividend per share. This means the company can raise dividends without significantly increasing the total payout. The strategy also frees up cash for reinvestment in operations, debt management, and acquisitions, ensuring long-term growth and flexibility.

Overall, the merger will bring about significant improvements to Amcor’s business model such as increased portfolio offering, improved R&D expertise along with increased compliance expertise to regulations (for the Healthcare market) and greater operational efficiency with strong synergies in cost savings and growth. The merger will also expand Amcor’s presence in North America and Europe, boosting Amcor with a larger market share in the global packaging solutions market.

2. Amcor’s R&D and Innovation are very thorough and well-developed in catering and specialising packaging to a wide range of industries, with a high degree of sustainability.

Merging with Berry, the combined company will have extraordinary innovation capabilities and scale. The combined R&D investment will be USD$180 million annually, supported by approximately 1,500 R&D professionals across 10 innovation centres worldwide and a portfolio of over 7,000 patents, registered designs, and trademarks. Amcor’s existing innovation centres are already a strong value proposition to Amcor’s business, as they are very client-centric. Amcor’s core R&D approach lies in its Catalyst™ program, a collaborative innovation approach that helps customers find packaging solutions by engaging directly with Amcor's experts to explore new packaging concepts and solve challenges, focusing on consumer needs and market dynamics. The services that the experts can provide are extensive, from consumer research to prototyping, graphic design, industrial design and technical trials. Additionally, clients can get access to Amcor’s global network of state-of-the-art innovation centres too. Amcor’s key innovation centers are in 1. Ghent, Belgium 2. Manchester, Michigan and 3. Neenah, Wisconsin.

Besides meeting the clients’ needs, Amcor’s R&D investments are also used for new developments and innovations. An instance is its Asia Pacific Innovation Center (APIC) in Jiangyin, Wuxi. Its APIC has The Ideation and Prototyping Innovation Lab and The Analytics & Application Lab. For The Ideation and Protoyping Innovation Lab, their lab-based prototyping process could help to shorten a client’s product development journey by up to 50%. For The Analytics & Application Lab, it is designed to identify and resolve issues such as unforeseen material performance and production inefficiencies by simulating real-world production scenarios, enabling a smooth and cost-effective transition from design to manufacturing. What’s even cooler is that its APIC developed the Amcor Eye, an augmented reality tool that provides virtual real-time support, allowing customers to remotely explore production stages, run trials, and collaborate with Amcor's experts from anywhere. All these help to provide greater convenience and guidance for a client’s production needs, by streamlining the innovation process for clients to understand the production process behind it while enhancing their customer experience.

Notably, Amcor integrates its innovations with a high degree of sustainability too which I believe this is the core of its competitive advantage. By adopting its customer-centric Catalyst program along with the R&D expertise by its various innovation centers and its many patents, this drives the development and adoption of more sustainable packaging solutions, focusing on recyclability, the use of recycled and renewable content, and minimizing environmental impact throughout the value chain while solidifying its leadership through its strong patents and trademarks.

The combined company will enjoyed enhanced capabilities by leveraging its corporate venturing partnerships to access new and groundbreaking sustainability solutions (substrates, barrier, fiber and recycling), digital solutions and disruptive ideas in adjacent businesses and technologies.

Amcor actively partners with start-ups and scale-ups through its corporate venturing approach to identify and accelerate the growth of innovative technologies aimed at advancing circularity in packaging. This allows Amcor to tap into cutting-edge developments and integrate them into their R&D efforts, potentially leading to more sustainable and efficient packaging solutions faster than relying solely on internal resources.

An example is the partnership with advanced recycling technology pioneer, Licella in Australia by investing in one of Australia's first plastic advanced recycling facilities. This initiative aims to create a local circular economy for soft plastics, advance Amcor's target of 30% recycled content by 2030, and utilize Licella's Cat-HTR™ technology to produce food-grade recycled content locally. This demonstrates Amcor's commitment to exploring and scaling up novel recycling solutions.

Financial Analysis

Ratios

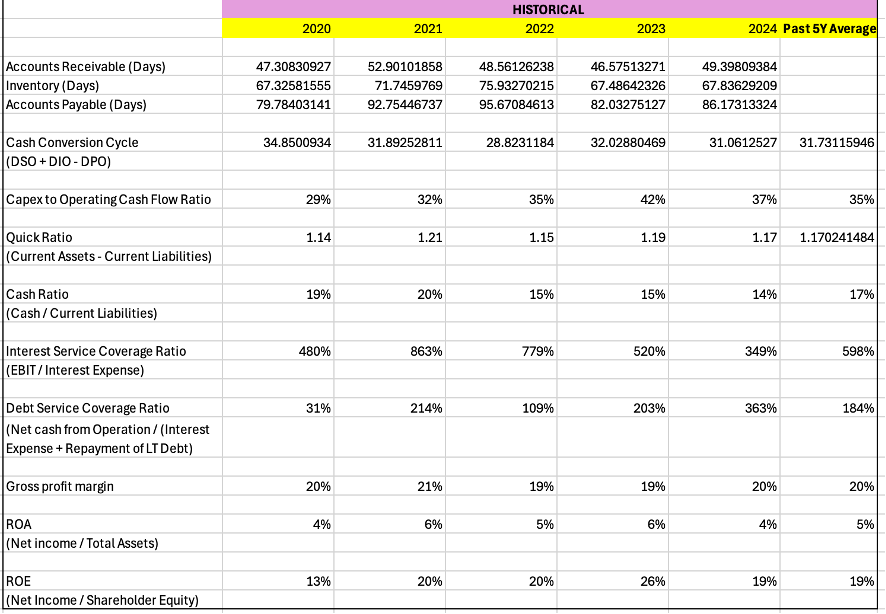

Refer to Appendix for breakdown of each ratio for the past 5 years

Amcor maintains strong financial stability with mixed liquidity, solid operational efficiency, and good profitability, though there is room for improvement. The cash ratio of 17% suggests limited cash reserves for short-term liabilities, but a quick ratio of 117% and a debt service coverage ratio of 184% indicate strong overall liquidity. Operationally, Amcor is efficient, with a CAPEX to operating cash flow ratio of 35%, reflecting reinvestment in growth, and a 32-day cash conversion cycle, signaling effective working capital management. Profitability remains decent, with a 20% gross profit margin and a 5% ROA, suggesting opportunities to optimize costs and asset utilization, though a strong 19% ROE reflects solid shareholder returns. Amcor’s solvency is robust, with a 598% interest coverage ratio, demonstrating its ability to meet long-term obligations with minimal financial risk.

DCF Valuation

This DCF model is not a M&A Model that took into account the merger with Berry Global due to my limited technical expertise, however, despite this, I have focused on forecasting Amcor’s standalone growth and projecting its future performance based on the potential improvement Amcor could gain by the merger with Berry Global. I then obtained an implied share price of USD$15.81, which is 59% higher than its current share price of USD$9.93. This valuation is based on Amcor's growth potential, including anticipated improvements in revenue and profitability. The model reflects the company’s ability to generate strong cash flows, which, even in the absence of the merger synergies, suggest that Amcor is positioned for growth in the coming years.

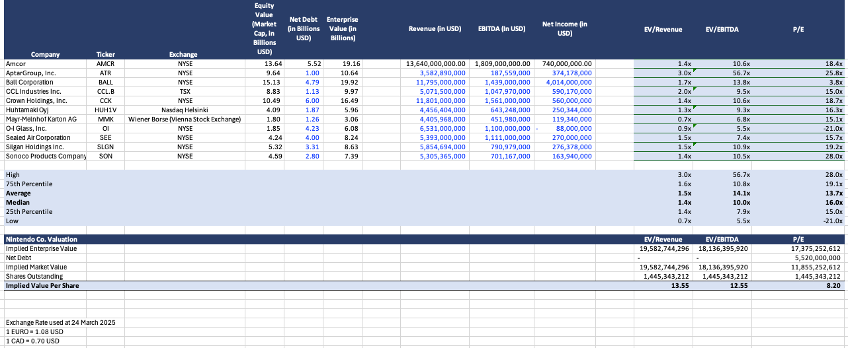

Comparable Companies Analysis

From Amcor’s annual report, the competitors are the one being studied in my Comparable Companies Analysis table.

Comparing Amcor’s EV multiples and P/E Ratio with its industry peers (against the median), Amcor is quite aligned with its industry peers but being slightly more overvalued due to its higher EV/EBITDA and P/E Ratio multiples. This is attributed to its very large market capitalization compared to its other peers where majority of them (except BALL) are smaller. Using the multiples to derive the implied share price for Amcor, the implied share price for Amcor ranges from USD$8.20 to USD$13.55, where Amcor’s current share price of USD$9.93 (as of 13 March 2025) lies within the range. This suggests that the stock is fairly valued based on peer comparisons. The higher multiples could signal that investors are willing to pay a premium for Amcor’s potential growth or competitive positioning. I believe this would be even more convincing, especially after Amcor has merged with Berry Global and occupy a much larger market share in the global packaging solutions market.

ESG profile

Environmental

Amcor has demonstrated a strong commitment to environmental sustainability, as evidenced by its 'AA' rating from MSCI ESG for five consecutive years. The company has set ambitious goals, including making all packaging recyclable or reusable by 2025 and achieving net-zero emissions by 2050. Significant progress has been made towards these targets, with a 14% reduction in absolute greenhouse gas emissions and a substantial increase in renewable electricity usage to over 70% in the most recent fiscal year. Amcor's commitment to circular economy principles is further demonstrated by the purchase of over 254,000 metric tons of recycled materials, surpassing its 2025 goal of incorporating 10% post-consumer recycled (PCR) plastic content a year early. Additionally, the company has set a longer-term target to achieve 30% recycled content across all products by 2030. Amcor has reduced waste sent to disposal by 33% over the past three years, with 121 sites achieving zero waste-to-disposal. Furthermore, Amcor's portfolio now includes 94% flexible packaging with recycle-ready solutions and 95% rigid packaging deemed recyclable at scale. These achievements highlight Amcor's leadership in driving sustainability within the packaging industry and its dedication to creating innovative solutions that align with global recyclability standards.

Social

On the social front, Amcor has prioritized employee safety and inclusivity, achieving significant progress. The company reported a 12% reduction in injuries compared to the previous fiscal year, with more than 70% of sites remaining injury-free for 12 months or more. This marks Amcor's safest year on record, with a milestone achievement of a 1.36 recordable case frequency rate (RCFR) and a 0.27 total recordable injury rate (TRIR). Regarding diversity and inclusion efforts, Amcor has made substantial strides. The company has developed a comprehensive global Diversity, Equity, and Inclusion (DE&I) strategy based on four key pillars: talent, community, awareness and training, and data and reporting. Employee Resource Groups (ERGs) continue to play a vital role in fostering inclusivity, with ABENDI, the ERG for Black employees, creating an inclusive environment that empowers and develops Black colleagues. Amcor has implemented specialized DE&I training designed for production workers, addressing the challenge of reaching colleagues with different shift patterns. The company's 2024 Sustainability Report showcases various global initiatives driving progress in inclusion and belonging. These initiatives demonstrate Amcor's commitment to creating a more diverse, equitable, and inclusive workforce. As the company continues to evolve its DE&I strategy, it could consider exploring opportunities to hire neurodivergent individuals in packaging processes, leveraging their potential skills for sustained attention on repetitive tasks. This approach could further enhance Amcor's inclusive workplace while potentially benefiting from unique talents in specific roles.

Governance

Governance-wise, Amcor has taken concrete steps to integrate sustainability into its business strategy. The company's long-term carbon reduction targets have been approved by the Science Based Targets initiative (SBTi), aiming to achieve net-zero greenhouse gas emissions across its value chain by 2050. This commitment includes significant absolute reductions in scope 1, 2, and 3 emissions. Amcor has also set near-term targets aligned with a 1.5-degree Celsius trajectory, targeting a 54.6% reduction in absolute Scope 1 and 2 emissions and a 32.5% reduction in Scope 3 emissions by fiscal year 2033. The launch of the TRANSPARENCE sustainability program for its closures and capsules business unit further demonstrates Amcor's commitment to establishing clear objectives and measurable actions, focusing on three strategic pillars: reduce, recycle, and respect. This program aims to provide transparency and assurance to wine and spirits brands regarding sustainability initiatives

Additional achievements include recycling 77% of operational waste, certifying 153 sites as "zero waste-to-disposal," and implementing water management plans across all sites. Amcor has also engaged its supply chain in sustainability efforts, hosting a Supplier Sustainability Summit focused on GHG emissions reduction with over 110 suppliers participating.

Overall

These combined efforts showcase Amcor's comprehensive approach to ESG, addressing environmental concerns, promoting social responsibility, and implementing strong governance practices to drive sustainable business operations. Therefore, I believe Amcor is the rising sustainable packaging solutions company in the market.

Investment Risks

Economic Vulnerability

Amcor faces significant exposure to macroeconomic fluctuations that directly impact consumer demand for packaged goods. Recent challenges including geopolitical conflicts (Russia-Ukraine, Middle East), international tensions (China-Taiwan), persistent inflation, and elevated interest rates have created headwinds for the business. In economic downturns, customers typically respond by reducing orders, delaying purchases, or extending payment terms. This pattern was evident in fiscal year 2024, particularly in the first half, when Amcor experienced volume declines primarily due to inventory destocking and reduced consumer demand. The company's performance is intrinsically linked to consumer spending on food, beverages, healthcare, and personal care products. While Amcor implements various measures to offset inflationary pressures through pricing adjustments and operational efficiencies, there's often a time lag between cost increases and the company's ability to pass these on to customers. This delay can temporarily compress margins and impact cash flow during periods of economic volatility.

Supply Chain and Input Cost Pressures

As a packaging manufacturer, Amcor's profitability is heavily dependent on stable access to raw materials, including polymer resins, aluminium, paper, and various chemicals. These inputs are subject to significant price volatility driven by factors beyond the company's control—including commodity market fluctuations, currency movements, resource availability constraints, transportation disruptions, and geopolitical conflicts.

Energy costs represent another critical variable affecting Amcor's operations, with recent years demonstrating extraordinary volatility. Additionally, changing trade policies and tariffs can disrupt supply chains and increase costs unexpectedly, as evidenced by the retroactive duties assessed on certain aluminium imports from China in fiscal 2024.

While Amcor employs various risk mitigation strategies—including customer contracts with price adjustment mechanisms, alternative supplier development, and strategic hedging—these measures cannot guarantee complete protection against sudden input cost increases or supply disruptions. The timing gap between raw material cost increases and corresponding price adjustments to customers can temporarily strain working capital and affect profitability.

Operational Resilience Challenges

Amcor operates a complex global production network vulnerable to various operational disruptions. These include mechanical failures, technological outages, natural disasters, geopolitical events, and supply chain interruptions. For instance, severe weather events linked to climate change have already impacted agricultural productivity, affecting demand for meat packaging in fiscal 2023-2024 following drought-related reductions in U.S. cattle herds.

Beyond operational disruptions, Amcor faces counterparty risks across its value chain, particularly during periods of economic instability. Customer or supplier insolvency can lead to bad debt exposure, contract defaults, and production interruptions. Finding replacement suppliers or customers during turbulent market conditions typically comes with higher costs and transitional inefficiencies.

The interconnected nature of these operational risks means that disruptions in one area can quickly cascade throughout the business, potentially affecting multiple product lines, regions, or customer segments simultaneously. This complexity requires sophisticated risk management systems and contingency planning to minimize potential impacts.

Appendix

Appendix 1: Breakdown of the different Financial Ratios

References

Amcor plc. (2024). Annual Report 2024. https://downloads.ctfassets.net/f7tuyt85vtoa/4NIqgqYVvuDbLh72xmPssW/0f5370531ddae8a742926ea03c0da6bc/Amcor_Annual_Report_2024_WEB.pdf

Amcor plc. (2024). Sustainability Report. https://sustainability.amcor.com/en

Hejl, A. (2025, February 21). 1 healthcare stock to hold forever and 2 to ignore. Yahoo!Finance. https://finance.yahoo.com/news/1-healthcare-stock-hold-forever-130119374.html

West Pharmaceutical forecasts 2025 results below expectations, shares drop . Reuters. (2025, February 13). https://www.reuters.com/business/healthcare-pharmaceuticals/west-pharmaceutical-forecasts-2025-results-below-expectations-shares-drop-2025-02-13/

US beverage alcohol market set for slow recovery after “reset year.” IWSR. (2024, June 26). https://www.theiwsr.com/insight/us-beverage-alcohol-market-set-for-slow-recovery-after-reset-year/

Henkes, T., Cloetingh, J., Winters, A. D., & Moss, J. (2024, April 12). Annual Packaging Study 2023: The Great Stocking/Destocking Saga and Its Aftermath. L.E.K. https://www.lek.com/insights/ind/us/ar/annual-packaging-study-2023-great-stockingdestocking-saga-and-its-aftermath

Stephenson, J. (2024, January 16). Healthcare investing - 2024 outlook brighter on compelling valuations and easing headwinds. BNP Paribas Asset Management . https://www.bnpparibas-am.com/en-sg/institutional/portfolio-perspectives/healthcare-investing-2024-outlook-brighter-on-compelling-valuations-and-easing-headwinds/

Healthcare Packaging Market Size, Share, Trends Report, 2032. Fortune Business Insights . (2025, March 10). https://www.fortunebusinessinsights.com/healthcare-packaging-market-110539

Hacker K. (2024). The Burden of Chronic Disease. Mayo Clinic proceedings. Innovations, quality & outcomes, 8(1), 112–119. https://doi.org/10.1016/j.mayocpiqo.2023.08.005

North America Functional Beverage Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030). Mordor Intelligence. (n.d.). https://www.mordorintelligence.com/industry-reports/north-america-functional-beverage-market