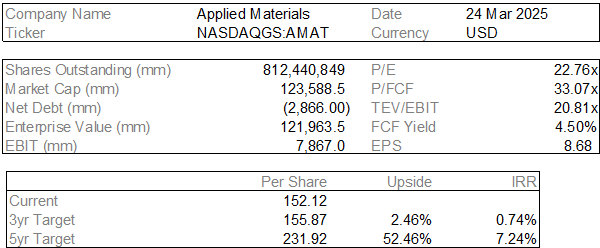

Initial Report: Applied Materials (NASDAQ: AMAT), 52.46% 5-yr Potential Upside (Zhi Qing YEOH, EIP)

Zhi Qing YEOH presents a "BUY" recommendation for Applied Materials based on heightened demand for advanced chips and a depressed stock price due to market overeaction.

1. Executive Summary

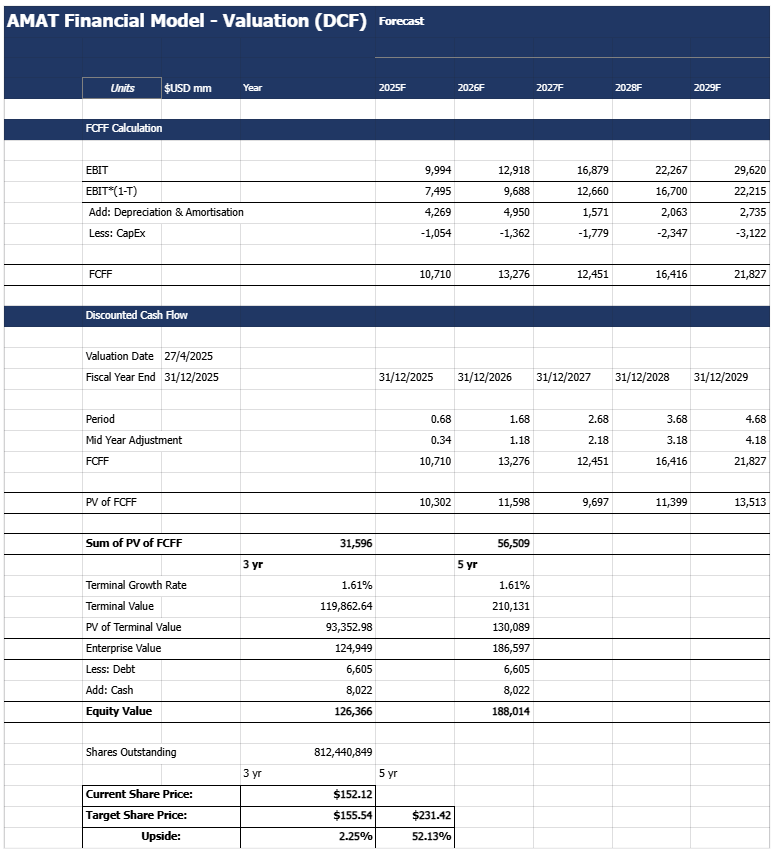

I initiate coverage on Applied Materials, Inc. (NASDAQGS : AMAT) with a BUY recommendation and a target price of US$231.42, representing a +52.13% upside based of its current price of US$152.12 as of 24/3/25. The target price was derived using a simple Discounted Cashflow valuation analysis. Applied Materials (AMAT) is a leader in materials engineering, providing unique and highly innovative equipment solutions used to produce virtually every chip and advanced display worldwide. My analysis indicates that AMAT’s role in the heightened demand for advanced chips is being largely overlooked by the market and its current depressed stock price due to market overeaction presents a compelling investment opportunity.

2. Company overview

Applied Material (AMAT) is a global leader in the area of Materials Engineering solutions used in virtually all semiconductor and advanced display. Incorporated by Delaware in 1967, AMAT boasts a diverse portfolio with a broad and deep range of products, catering to a wide variety of end uses. AMAT plays a key pivotal role in driving technological advancements by empowering its clients to achieve superior manufacturing processes.

Business segments

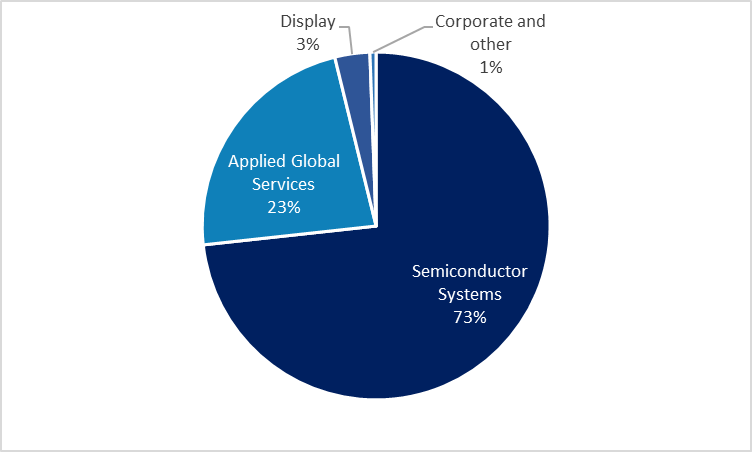

AMAT operates in 3 main segments:

1) Semiconductor Systems (73% of revenues)

2) Applied Global Service (43% of revenues)

3) Display (3% of revenues)

AMAT Revenue Segments

Source: AMAT Annual Report 2024

In Semiconductor Systems, AMAT focuses mainly on the production of equipment used in 300mm semiconductor chip fabrication. AMAT serves a broad spectrum of markets within this segment—Foundry, Logic and Others, DRAM, and Flash Memory—strategically positioning itself to offer clients a comprehensive and integrated manufacturing process and achieve greater market share.

In the Applied Global Services segment, AMAT provides servicing, spares and factory automation software to customers. As the bulk of this segment comprises of subscription-based contracts, customer demand and revenues in this area are highly sticky.

The Display segment comprises of products used in the manufacturing of Liquid Crystal Displays (LCDs), Organic Light-Emitting Diodes (OLEDs) and other display technologies used for consumer-oriented devices.

Revenue Drivers

With the emergence of new industry demands for advanced technology such as Artificial Intelligence (AI), there is an influx of demand for efficient semiconductor manufacturing equipment to enhance productivity. This opens up new opportunities for AMAT to leverage on and continue growing its revenue.

Cost drivers

Supply chain disruptions pose huge cost burdens on AMAT, heightening the cost of operations.

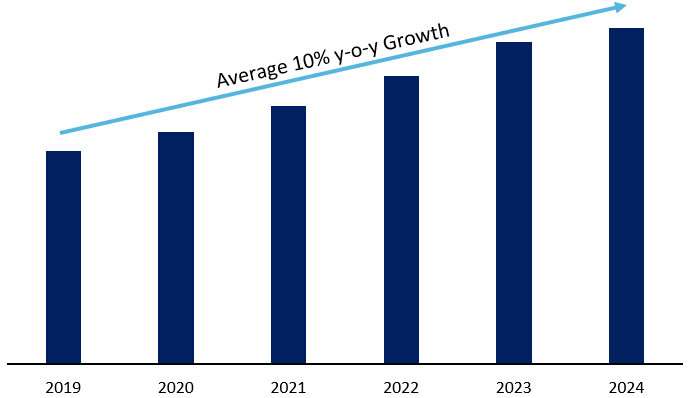

Additionally, AMAT invests heavily and continuously into Research & Development (R&D), with >$22 Billion of its profits having been reinvested in 2024.

AMAT's Yearly R&D Spending

Source: CapIQ

ESG considerations

Environmental

70% of electricity used by AMAT globally, including 100% of that used by the United States, comes from renewable sources. Furthermore, AMAT has successfully reduced its Scope 1 and 2 emissions by 4% compared to 2022, putting it on track to achieve its goal of reducing both emission scopes by 50% by 2030.

Additionally, AMAT strives to lower the average per-wafer energy use with changes in the mix of products sold, enabling them to achieve their goal of reducing energy consumption per-wafer pass for semiconductor products by 30% by 2030.

Social

AMAT is committed to creating an environment that is able to retain, attract and develop a capable team of employees. With Employee Stock Incentive Plans, Stock Repurchase Plans, healthcare and retirement benefits, parental and family leave and tuition assistance, AMAT provides its workforce with high quality holistic welfare. Employees are also engaged in their experiences and satisfaction at the workplace through all-employee surveys. Leaders and managers gain actionable insights on ways to enhance employee inclusion and satisfaction.

AMAT invests in the training of their employees and provides them with learning opportunities. A model of 70% learning on the job and 10% collaborative learning and 10% formal training is used by AMAT to provide holistic employee learning and development.

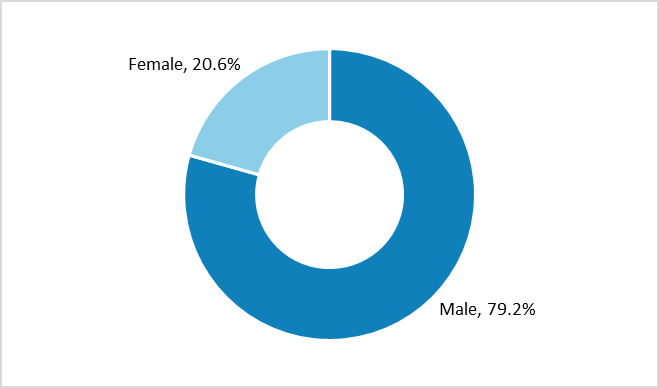

With a diverse team of employees, AMAT promotes inclusivity in their workforce, both in terms of gender inclusivity and minority representation. AMAT also boasts a 30% female representation on its Board.

Gender Diversity in AMAT's Global Workforce

Source: 2024 AMAT Annual Report

Minority Representation in AMAT's Global Workforce

Source: 2024 AMAT Annual Report

Governance

With a 90% independent Board, this Board of Directors is responsible for the oversight of assessing major risks affecting AMAT, with an Audit Committee overseeing the cybersecurity risks and its management program. A Standards of Business Conduct; a code of ethics, is in place and applied to every employee and member of the Board of Directors. Should any changes be made to this code of ethics, AMAT will disclose the nature of the amendment on their website, ensuring transparency and fortifying the trust in their business operations.

Additionally, an Insider Trading Policy is present to govern the purchase, sale and other dispositions of their securities by their directors, officers, employees and other individuals associated with AMAT to promote compliance with insider trading laws and regulations.

3. Competitor analysis

Financial Analysis

Comparing the Financial ratios of AMAT with its industry peers, AMAT, 2.60, is seen to have a higher than average Current Ratio, 2.34. This suggests that AMAT is better positioned to service its current liabilities given its better liquidity in capital than its peers.

For Return on Equity and Return on Assets, AMAT sees high returns on both, with 48.04% and 16.65% respectively, compared to the respective averages of 45.06% and 13.63%. This means that AMAT is better able to utilise its equity and assets to generate higher revenue returns; higher profitability.

AMAT's EV/LTM EBIT is the lowest at 20.81. This means that AMAT is undervalued in comparison to its earnings capabilities.

Similarly, AMAT's Price/Book ratio of 9.01 is significantly lower than the average of 15.23. This further reinforces my belief that AMAT is undervalued, considering its strong profitability.

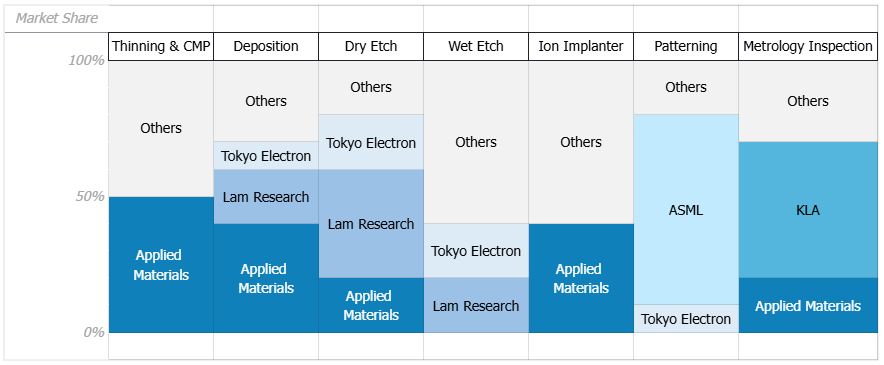

Economic moat

In comparison to other competitors in the industry, AMAT boasts a highly diverse portfolio that serves nearly all parts of the fabrication manufacturing process chain of semiconductor chips. Given the highly integrated chain of equipment AMAT has, this plays into the economic moat of 'Switching Costs'. AMAT customers will incur heightened costs should they switch out their AMAT equipment from their manufacturing process chain as such equipment is highly sensitive to changes. Equipment bought from other manufacturers may cause disruptions or lower efficiencies in production. Therefore, AMAT's wide portfolio will enable it to build up customer loyalty, translating into sticker revenue streams and opportunities for gains in market share.

Wafer Fabrication Equipment Vendor Market Share 2023

Source: Yole 2024

4. Investment thesis

Thesis 1: Enhancing Economic Moats Drives Resilient Revenue Growths

Widening Economic Moats

With continued co-innovation with clients, AMAT has been able to adapt their products to meet the direct needs of clients. As such, their products are highly optimized, increasing the depth of their portfolio. This enables AMAT to drive greater production efficiency and expand their production further, constituting greater economies of scale in each operating segment. Since AMAT is able to produce highly tailored solutions for customers through collaborative innovation, this deepens their economic moat whereby clients now incur higher switching costs should they change from AMAT. Furthermore, AMAT's products are highly interconnected, given their wide range of products for each step in the manufacturing process chain, clients' will experience costs to recalibrate their equipment, or even incompatibility, if they change to another brand. This further deepens AMAT's economic moat of switching costs, which increases the barriers for entry of new entrants, reinforcing their strong market standing.

Moreover, AMAT has previously primed itself towards producing equipment for manufacturing greater energy efficient chips, as seen in their investments into new segments like advanced packaging and backside power architecture, becoming competitively positioned to gain 50% share in these markets. With more new products in the works, AMAT will be able to grow their available market and strengthen their leadership through leveraging on their materials engineering expertise.

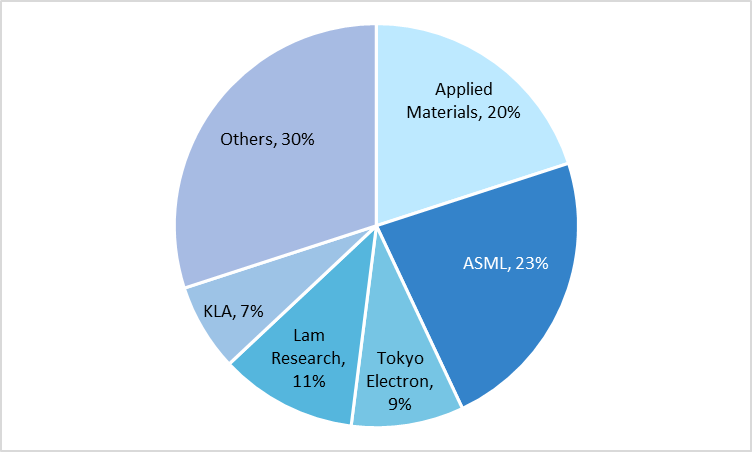

This dedication to building on the widening of their economic moats by expanding on the breadth and width of their portfolio is paying off well for AMAT with the continued heightening demand for next-generation chips, posing new opportunities to expand their market share beyond the current 20%.

Wafer Fabrication Equipment (WFE) Market

Source: Yole 2024

Thesis 2: Fortified Market Dominance Through Strategic Expansions

Strategic product portfolio investments

Major device architecture inflections in the semiconductor industry have been identified by AMAT early on. AMAT has focused its strategy and investments towards delivering innovations that strengthens their position in these main technology high transition areas of Logic, Memory and Advanced Packaging that are critical to the development of energy-efficient AI. AMAT has continuously invested and innovated in these major inflection areas for ~4 years, representing ~$13B of R&D investments.

Additionally, AMAT works closely with their clients to produce unique and co-optimized technologies that enable comprehensive solutions for them. As they serve key players in the semiconductor foundries industry; such as TSMC and Intel, the drive in collaboration allows AMAT to have a more comprehensive and first-hand insight in the trends and considerations of their clients and the markets they serve, giving them a first-mover advantage.

Through their close client relationships, AMAT can continuously focus on strategically growing their portfolio towards major market inflections early on. Robust traction in the industry as major players ramp up on GAA transistors into high-volume wafer fabrication manufacturing coupled with AMAT’s steady strategic investments into enhancing the depth and width of its products portfolio enables it to maintain their strong competitive positioning at the top of the market with relevant leading-edge logic, high performance 3D DRAM, DRAM die stacking, advanced packaging and power electronics solutions.

AMAT's Innovation Strategy

Source: AMAT 2025 Proxy Statement

Unparalleled market leadership

Leveraging on strong market demand for leading-edge Logic, DRAM, Advanced Packaging and NAND, AMAT’s market leadership is strengthened with their unique and most diverse portfolio that has a strong focus on these key areas. AMAT is committed towards achieving improvements in chip Performance, Power, area, Cost and Time to market (PPACt) with its materials engineering innovations and expertise. Reinvestments into R&D to support their technology growth stands at a total of more than $22B in the past 10 years, with yearly growths at a CAGR of 8%, with a targeted ~$3B being invested annually in R&D.

This drive for innovation further differentiates AMAT’s portfolio, strengthening their position at major inflections.

Comparison of R&D Investments between WFE Market Players

Source: CapitalIQ

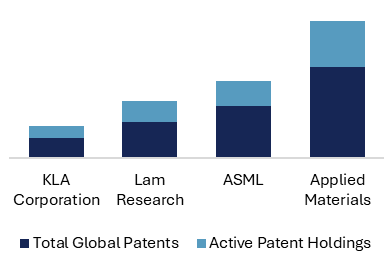

Furthermore, AMAT holds more than 29,000 active technology patents worldwide, surpassing other WFE industry players by a significant margin. These patented technologies showcases and maintains AMAT’s unmatched leadership and scale with its diverse irreplicable novel products and solutions.

Number of Active Global Patents & Active Patents Held

Source: Insights by GreyB

Thesis 3: Riding The Tailwinds of Global Tech Market Inflections

New opportunities with global tech market shifts

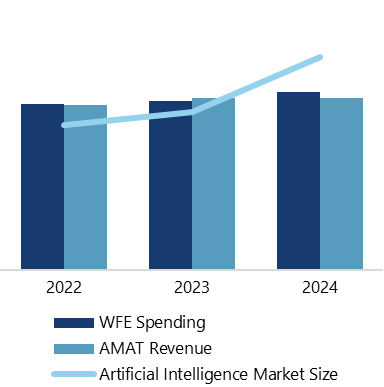

Booming demand for semiconductors is underpinned by robust high growths, enabled by the Artificial Intelligence (AI) megatrend, in the Tech industry. Semiconductors are at the foundation of these transformative shifts in technology that will alter the future global tech ecosystem. Increasing complexity in AI has expanded demands for immense computational power. This in turn drives the need for advances in chip energy-efficiency. Moreover, as stated in Moore's Law, recent disruptive innovations in the tech industry have driven energy consumption and AI costs lower, fueling the race for greater energy efficiency. These inflections grow the global Semiconductor market and increases the need for materials engineering innovations in the production chain.

AI Market Size In Comparison To Total WFE Spending And AMAT Total Revenue (Rebased)

Source: Statista & SEMI

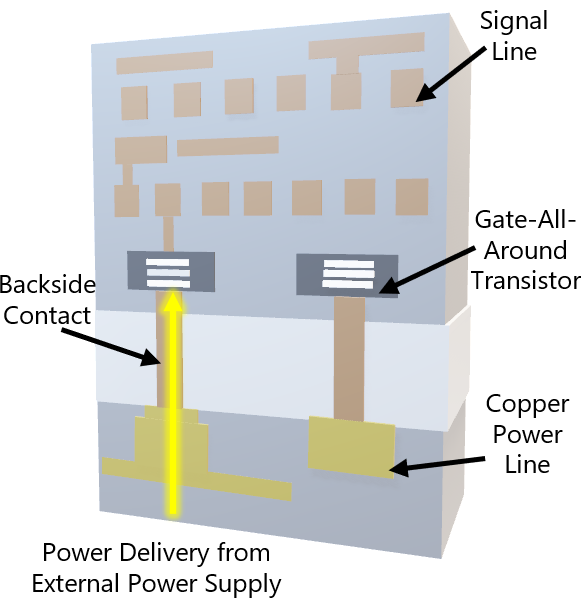

Being a leader in materials engineering expertise, AMAT is primed to leverage on these global inflections especially in the areas of chip architecture and backside power delivery, to deliver greater chip power-efficiency. Given historical strategic investments in Research and Development (R&D), AMAT has a wide materials engineering products portfolio that includes next-generation gate-all-around transistors, backside power delivery, 4F-squared and 3D DRAM, advanced packaging, compound semiconductors for power electronics and silicon photonics, allowing AMAT to be strongly positioned to benefit from these major industry inflections and gain market share.

Backside Power Delivery Wiring with Gate-All-Around Architecture

Source: AMAT 2021 Logic Master Class

AMAT’s introduction of new Backside Power Delivery wiring; which increases logic density and improve on power and performance, will enable the growth of its wiring Serviceable Addressable Market (SAM) to ~$7B. AMAT’s latest gate-all-around transistor architecture at 2nm; which enables greater transistor scaling with low variability and increased performance and power, will see strong market momentum with increasing high-volume manufacturing for advanced technology nodes, growing AMAT’s transistor SAM to ~$7B. Together with AMAT’s cutting-edge innovations in Advanced Packaging, they present opportunities for AMAT to grow revenues by ~30% for the same number of fab capacity as they offer solutions to the market demands for energy-efficient chips.

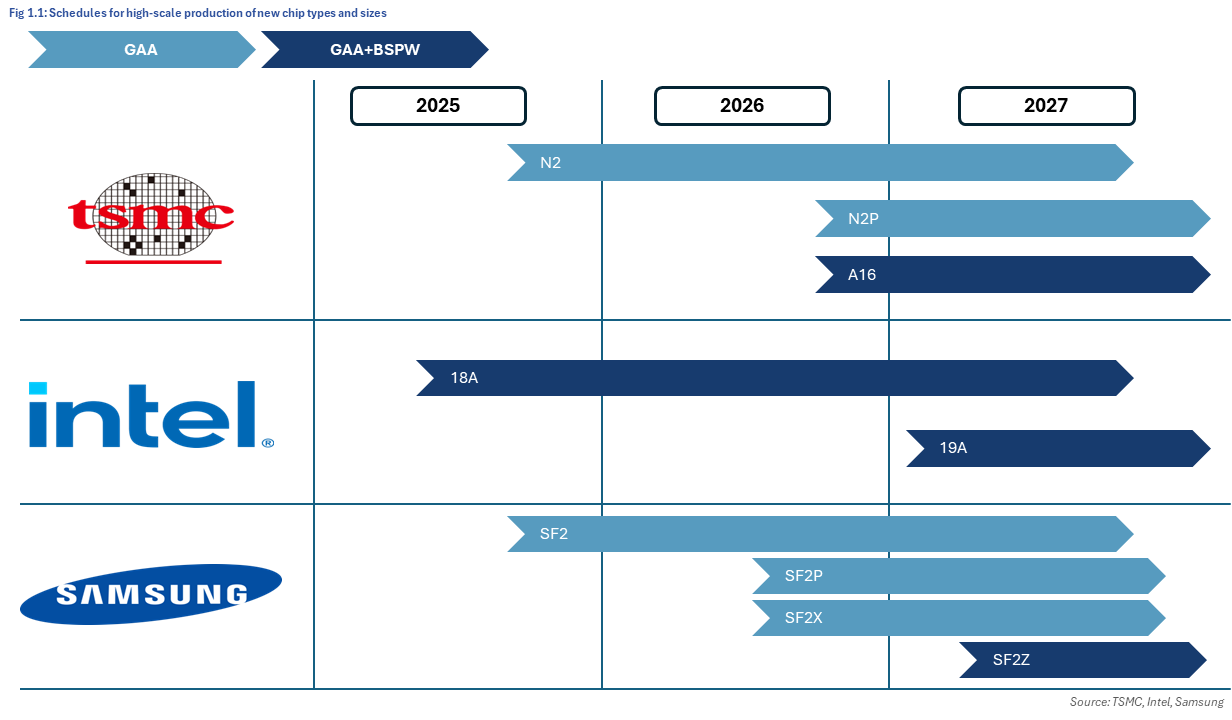

Furthermore, AMAT’s key clients; TSMC, Intel, Samsung, have announced the shifting of their production towards including Backside Power Delivery wirings and Gate-All-Around (GAA) architectures. All three large foundries are set to introduce real high-volume GAA in 2025 for 3nm processes and moving towards GAA combined with Backside Power wiring processes and 2nm processes in the years after. AMAT’s strategic investments in its innovations competitively positions it to meet their major clients’ new demands, generating long-term profits from these market inflections.

Schedule for High-Scale Production Of New Chip Types And Sizes

Source: TSMC, Intel, Samsung

Resilient revenue expansion despite volatility in the geopolitical landscape

In relation to Jevon’s Paradox, the recent strides of increased technological efficiency is driving heightened demand for, and increased consumption of AI. This poses huge opportunities for AMAT to leverage on their diverse connected portfolio to offer clients unique, connected and high value solutions that competitors cannot replicate, increasing their revenues. Wafer production growth will boost sales of deposition, etching, and metrology and inspection (M&I) equipment, with large investments in epiwafer production in markets. The Semiconductor Wafer Fabrication Equipment (WFE) demand sees stable levels of market demand and is expected to grow at a CAGR of 4.1% to around $130B in 2029, from which, AMAT projects to generate a strong~$5.3B in its semiconductor systems segment in Q2 2025.

Furthermore, AMAT has increased their focus on driving worldwide R&D collaboration with clients and partners to accelerate the innovation and commercialization of new technologies. This will be further enhanced when the construction of the EPIC Center in Silicon Valley is completed in 2026. This collaboration strategy brought together players in the semiconductor ecosystem by AMAT positions it to benefit from breakthroughs in semiconductor innovations at a faster production volume and lower cost. New innovations that offer higher-value solutions which difficult for competitors to replicate, will allow AMAT to expand their SAM in both their domestic market and in the markets of countries who are less affected by trade restrictions. Moreover, by deploying their advanced service products to help customers improve their production processes, AMAT benefits from having a sticky revenue stream of subscriptions through long-term agreements which accounts for a high proportion of its $6.2M revenue from Global Applied Services business segment.

With strong momentum in WFE, AMAT will be able to continue experiencing resilient low double-digit annualized revenue growths in the long-term and a strong revenue position of ~$7.1B in 2025.

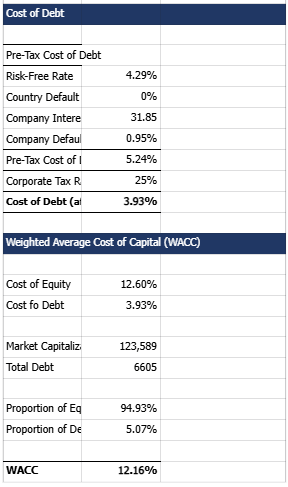

5. Valuation

6. Risks and mitigation

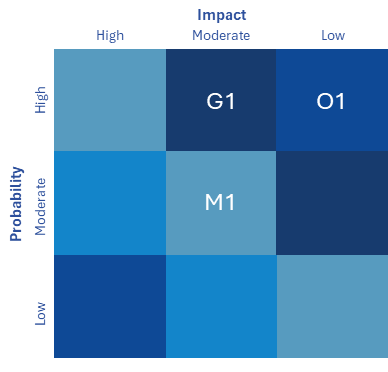

Risk Matrix

Operational Risk

O1 | Heavy Dependence on Capital Expenditures

Probability: High | Impact: Low

With relation to Moore's Law, new products and innovations released quickly become outdated. The rapid pace of technological advancements results in the indispensable need for AMAT to constantly innovate in order to prevent product obsolence and keep up with the highly volatile markets that it operates in. This has led to AMAT's increasing reliance on Capital Expenditures (CAPEX), particularly in R&D, with investments growing year after year.

Mitigation: Applied Materials has demonstrated prudent financial management by maintaining a net cash position, with cash reserves, exceeding its debt obligations. This financial stability allows the company to invest strategically without over-reliance on external capital. Furthermore, on 24 February 2025, AMAT secured a $2 Billion credit revolver facility, underscores Applied Materials' efforts to strengthen its capital structure and support ongoing operations and potential future investments and CAPEX with a strong supply of liquidity.

Market Risk

M1 | Intense Industry Competition

Probability: Moderate | Impact: Moderate

AMAT operates in highly competitive industries — Semiconductor, Applied Global Services and Display, facing competitors of various scales and sizes. These industries face rapid continued changes and advancements, with companies striving to achieve innovation breakthroughs and products to gain a first-mover advantage in the market.

Increased competition has also emerged from domestic equipment manufacturers in China, driven by local government incentives and fundings.

Failure to match competitors’ technological capabilities and product offerings could result in AMAT losing market share to more agile competitors, compromising on their expansion and growth.

Mitigation: AMAT demonstrates a strong ability to swiftly detect market shifts and adapt its product portfolio to meet evolving client and market demands, sustaining its competitive advantage. AMAT’s strong and expanding R&D investments highlights its commitment towards strengthening and growing its economic moats, remaining highly competitive in the industries they operate in.

Global Risk

G1 | Macro-Economic and Regulatory Headwinds Threaten AMAT’s Market Growth

Probability: High | Impact: Moderate

With increased volatility and tensions between countries, especially between the 2 world powers, there is increased operational uncertainty, escalation of operational costs and global supply chain disruptions within the semiconductor industry.

The present landscape presents challenges for AMAT who faces shrinkages in SAM, heightened operational risks and supply chain disruptions, with an estimated $400B impact from trade disruptions and a reduction in percentage of revenue to below the normalized level of 30% for China alone.

Tightening of export controls imposed by the US government on semiconductor manufacturing equipment to Chinese companies has increased in recent years.

This will materially affect AMAT’s SAM given that their biggest market remains China.

This may potentially worsen AMAT’s order backlogs of $15B as of 2024.

Additionally, United States’s export controls restricting certain technology sales to Chinese customers have given AMAT’s international competitors an advantage.

Mitigation: AMAT has turned towards greater developing and commercializing the most enabling technologies for the industry across leading-edge logic, memory, advanced packaging and ICAPS.

7. Conclusion

In conclusion, I think that AMAT is posied for accelerated growth given their competitive positioning to benefit from the growing technological advancements and trends. Their strong market leadership, coupled with their continued investments and innovations in improving their product portfolio, provides AMAT with a significant competitive edge despite the volatile geopolitical scene.

Therefore, I reiterate my BUY call on AMAT with a target price of US$231.42, representing a +52.13% upside.