Initial Report: BYD Co Ltd (1211), 168% 5-yr Potential Upside (VIP IC)

Time to buy into BYD? Let's see why our students think this is a great idea!

LinkedIn | Javier CHAN

Company Description

BYD is one of the world’s largest automobile manufacturers, headquartered in Shenzhen, China. They engage in the research, development, manufacture and sale of automobiles and related products globally. BYD started off as a rechargeable-battery factory and grew rapidly by supplying batteries to various mobile phone manufacturers. They manufacture and sell cell phone components and handsets to customers such as Nokia, Huawei and Motorola.

Highlights

In 2022, BYD surpassed Tesla to become the world’s largest EV producer by volume. 3QFY22 saw EV sales of over 537,000 units, an increase of 197% yoy [1]. Top 3 models – Song, Qin, Han, contributed over 56% of sales. As of March 2023, BYD holds a 45% market share in China’s overall EV market, and has expanded into foreign markets like Japan, Germany, Singapore, Australia, and India.

Business Segments

1. Automobiles and Related Products (112.49 Billion - 52% Revenue)

Comprises manufacturing and sale of: (1) Automobiles, (2) Auto-related Moulds and Components, (3) Automobile Leasing and ASS, (4) Rail Transport Related Business and (5) Medical Protection Products.

2. Mobile Handset Components, Assembly Service & Other Products (86.45 Billion - 41% Revenue)

Comprises the manufacturing, sale and provision of: (1) Mobile Handset Components, (2) Medical Products and (3) Assembly Services. BYD’s subsidiary company, BYD Electronic, falls under this segment.

3. Rechargeable Batteries & Photovoltaic Business (16.47 Billion - 7% Revenue)

Comprises the manufacturing and sale of: (1) Lithium-ion and Nickel Batteries, (2) Photovoltaic Products and (3) Iron Battery Products.

BYD has grown to become the 2nd largest battery supplier in China (behind CATL) and is the 3rd largest battery manufacturer in the world (11.8% market share). They are the largest Chinese manufacturer of rechargeable lithium iron phosphate (LFP) batteries.

Geographical Breakdown

Domestic PRC market remains its primary focus (70% of sales) although it has indicated its ambitions to expand overseas (30% of sales).

Industry Overview

TAM

As of 2021, global EV market estimated to be worth USD 170 billion (8m units) and is projected to reach over USD 1.1 trillion (39m units) by 2030, representing 23.1% CAGR.

ICE > EV Adoption

For many years, China’s EV market was primarily driven by policy. Combination of fuel economy regulations, new-energy vehicle quota system, government fleet mandates and direct purchase subsidies all added regulatory pressure and incentives for both automakers and consumers to go electric.

But today, EV adoption has now run well ahead of mere national interests, and conversion from ICE to EVs have become more organic. Drivers of conversion are lower operating costs, better/safer driving experience, environmental friendliness, and more readily available charging infrastructure.

Charging Infrastructure

Number of publicly available chargers in the world is increasing rapidly, growing by ~40% in 2021. China has a 65% share of public EV charging stations in the world with a total of 1.15 million stations. Of which, Guangdong Province has the highest number of charging stations of 343,595 stations. The development and construction of charging infrastructure globally helps to support the exponential rise in EV penetration and creates a conducive environment for further adoption.

Impact of Covid-19

The pandemic placed great stress on the automobile industry due to the halting of production, disruptions in global supply-chains and reduced consumer demand. Pandemic-led fluctuations in vehicle order quantities and lower capacity utilization proved to be detrimental to the profitability of the entire industry. The sales of cars declined by more than 40% due to the pandemic in China alone. Since then supply chain crisis has eased and demand recovery story has played out.

Investment Thesis

What the bears say:

Escalating battery raw material costs will put BYD’s margins under pressure. Prices of metals such as nickel, lithium, cobalt and manganese which are used to power EV batteries have soared in the past year. Batteries currently account for about 30-40% of EV manufacturing cost. Raw materials make up ~63% of the total battery cost; used mostly as material for the cathode and anode.

Observation: EV makers’ margins are extremely sensitive to any changes in price of these metals. Nickel spot price has risen by 20% yoy and is currently in contango (signals bullish sentiment moving forward). The increase in price of these metals have been attributed to supply shortages due to growing EV demand, as well as the ongoing supply chain disruption that has been exacerbated by the invasion of Ukraine by Russia.

What we think:

The street has overlooked measures that BYD has in place to safeguard their profitability. BYD’s (1) vertically integrated supply chain, (2) cheaper proprietary battery technology, and (3) product price hikes, will help to preserve their margins during this difficult period.

1. BYD sets themselves apart from competitors by keeping as much of its supply chain as possible under its own roof.

Unlike nearly all its peers, BYD produces its own EV batteries. They also make about 70% of the chips used in its EVs in-house and relies on outside vendors only for the higher-end chips such as autonomous driving chips. This allows them to bypass the average third-party sales markup of 82% (derived from the industry gross margin of 45%).

2. Market is also discounting BYD’s ability to manufacture batteries at a lower cost compared to peers.

BYD’s proprietary Blade Battery technology allows them to produce cheaper yet high-capacity EV batteries at scale. More energy dense but is about 42% cheaper than traditional LFP batteries. Currently, the blade batteries are present in all of BYD’s passenger EVs. In Sept 2022, BYD announced that they will be looking to implement its Blade Batteries into its commercial EVs as well.

As BYD continues to roll out implementation of Blade Batteries, company gross margins will widen from lower vehicle manufacturing costs, as well as additional leverage from the sales of Blade Batteries to Tesla.

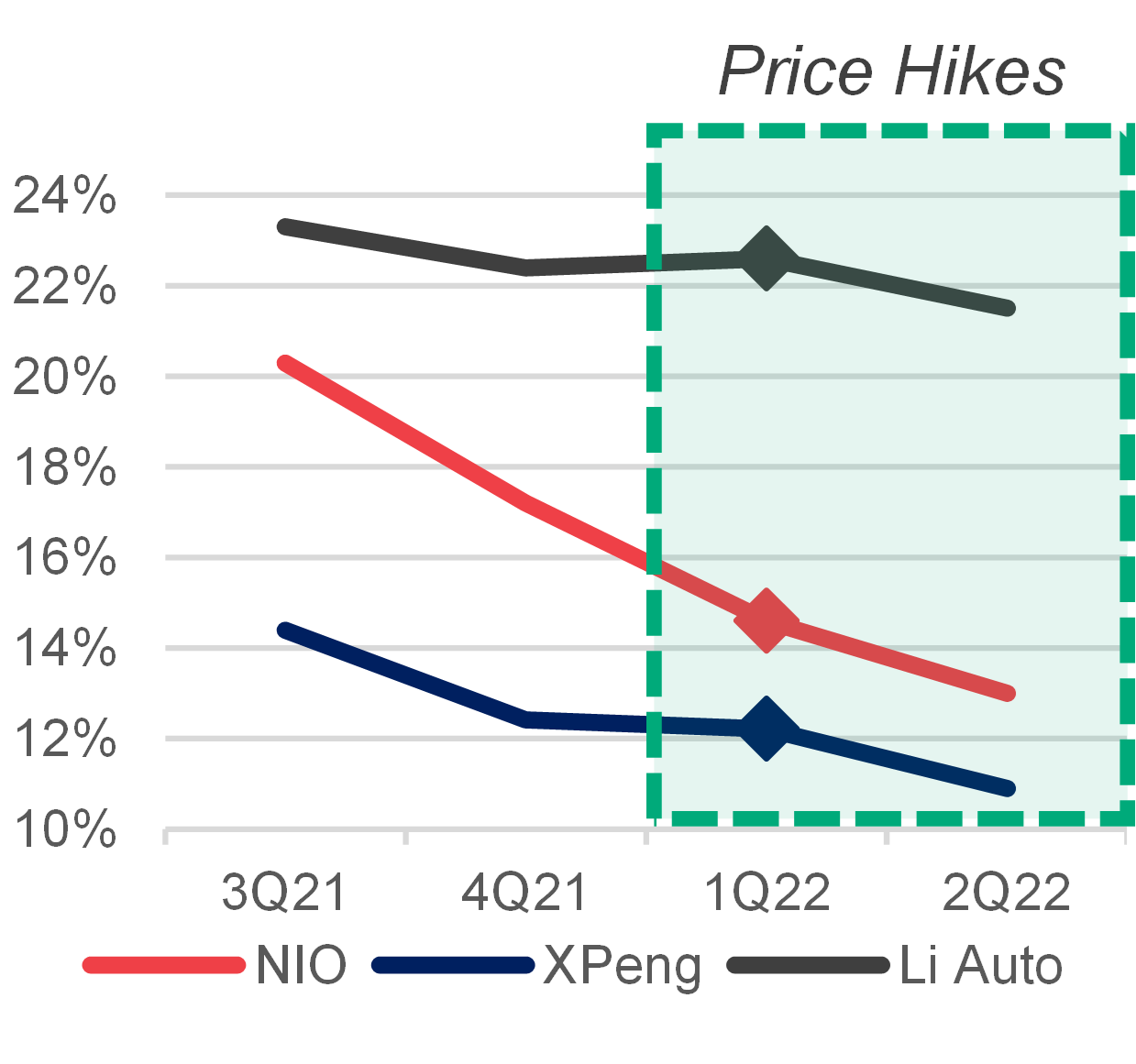

3. BYD has been hiking the prices of their EVs. In March 2022, BYD announced that they will raise prices on their cars by 3,000-6,000 yuan (US$471-942), citing raw material costs.

This was their second price hike of the year, with the first being a hike of 1,000-7,000 yuan in February, citing rising raw material costs and the cutting of government subsidies for NEVs.

BYD has strong brand equity among their consumers and still delivers the most value for less. We believe that BYD has the pricing power to continue raising prices to offset any potential margin dilution.

Analysing their track record of price hikes, we can observe that their price hikes have been accretive to gross margins - 12.4% > 14.4%.

This implies that the demand for their vehicles are potentially more price inelastic, in contrast to peers such as NIO and XPEV that have seen compressing margins in the past few quarters. Ability to raise prices will serve as a strong safety net for them to preserve margins. These profit guarding measures will be difficult for competitors to replicate, and this will grant them superior ability to offset any further increases in raw material costs.

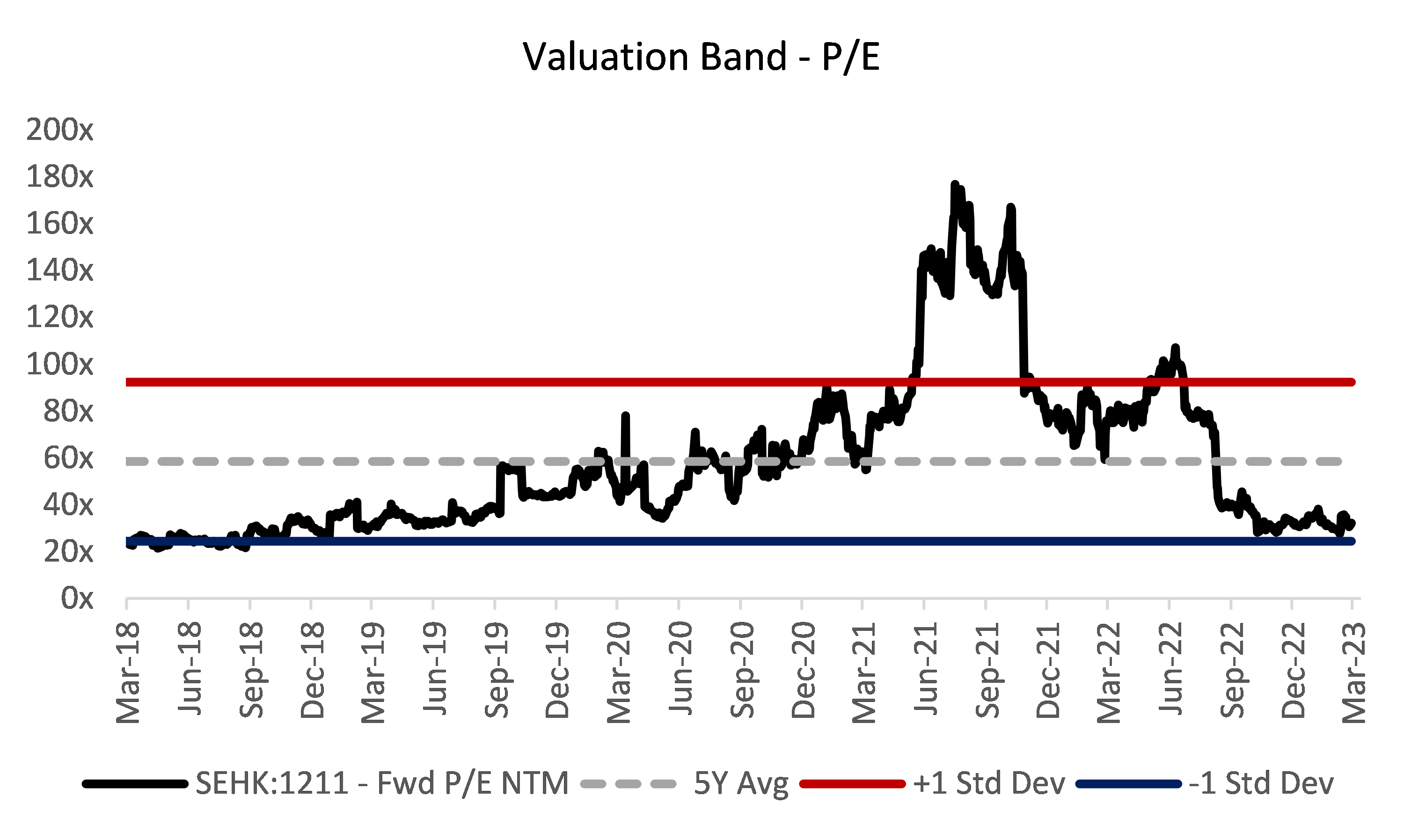

Valuation

EPS growth of 53% CAGR past 3 years.

Assuming similar earnings growth, we can expect FY24 EPS of about 8 RMB.

Current fwd P/E = 32x

Implied share price = 256 RMB (24% upside, 12% IRR)

Most likely IRR range between 6-23%, limited risk of further derating.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.

[1] https://www.counterpointresearch.com/global-ev-sales-q3-2022/