Initial Report: First Solar Inc (NASDAQ:FSLR), 88% 5-yr Potential Upside (VIP, How Cheng TONG)

How Cheng presents a "BUY" recommendation based on the expectation that the US Inflation Reduction Act (IRA) will lead to industry-leading gross margins and significant revenue growth for First Solar.

“Little darlin', the smile's returning to the faces Little darlin', it seems like years since it's been here”

- From the song Here Comes the Sun by The Beatles

LinkedIn: How Cheng TONG

Executive Summary

I am recommending a BUY for First Solar Inc (NASDAQ: FSLR) with a 5-year (5Y) target price of $453.39. The 5Y target price is derived from a P/E valuation where I forecast First Solar’s P/E ratio to normalise to its historical 10Y median P/E ratio (as of Sept 2024) of 23.48. My main theses for this recommendation are:

The tax credits of the US Inflation Reduction Act (IRA) are expected to help maintain or even expand First Solar’s industry leading gross margin through to 2032.

The US IRA is expected to drive significant revenue growth for First Solar in the coming years.

Overview of the business and the company

First Solar Inc (“First Solar”) is a leading American solar technology company and global provider of photovoltaic (“PV”) solar energy solutions. First Solar manufactures and sells PV solar modules with an advanced thin film semiconductor technology. These solar modules are developed in its research and development (“R&D”) labs in California and Ohio. As of 2023, First Solar is the world’s largest thin film PV solar module manufacturer and the largest PV solar module manufacturer in the Western Hemisphere. According to Statista, First Solar has a roughly 45% market share in the thin film solar manufacturing market as of 2021.

Thin film PV modules vs conventional crystalline silicon PV modules

Thin Film: Cheaper per watt upfront but less efficient in converting sunlight into electricity, often leading to higher system costs in space-constrained applications.

Crystalline Silicon: More expensive per watt upfront but more efficient in converting sunlight into electricity, resulting in lower system costs in many residential or commercial installations.

For many residential and rooftop applications, Crystalline Silicon is often the preferred choice due to its higher efficiency. However, in large-scale solar farms where space is abundant, Thin Film can be the more cost-effective option.

How does First Solar’s thin film PV modules compare to conventional crystalline silicon PV solar modules?

First Solar’s PV modules have several advantages over conventional crystalline silicon PV modules:

Material Efficiency: First Solar’s modules use Cadmium Telluride (CdTe) as the absorption layer. CdTe has absorption properties that are well matched to the solar spectrum and can deliver competitive wattage using around 97% less semiconductor material as compared to conventional crystalline silicon modules. This makes manufacturing First Solar’s modules less carbon and water intensive as compared to conventional crystalline modules.

Performance in High Temperatures: They have a superior temperature coefficient, resulting in better performance in high temperature climates.

Performance in Humid Environments: First Solar’s modules perform better in humid environments where atmospheric moisture alters the solar spectrum.

Durability: They are immune to cell cracking, a common issue in crystalline silicon modules, ensuring more reliable performance over time.

How are First Solar’s PV modules made?

Figure 1. First Solar's PV manufacturing process

First Solar’s modules are manufactured in a high-throughput, automated environment that integrates all manufacturing steps into a continuous flow process (Fig. 1). This process eliminates the multiple supply chain operators and resource-intensive batch processing steps that are used to produce crystalline silicon modules, which typically occur over several days and across multiple factories. At the outset of First Solar’s module production, a sheet of glass enters the production line and in a matter of hours is transformed into a completed module ready for shipment (Fig. 2).

Figure 2. First Solar's manufacturing efficiency as compared to crystalline PV manufacturers

As of 2023, First Solar has a global manufacturing footprint which includes facilities in the United States (US), Malaysia, Vietnam, and India.

Revenue breakdown

First Solar’s revenue primarily comes from its modules business, which involves the design, manufacture, and sale of CdTe solar PV modules. These modules are mainly sold to utility scale solar project developers in the US. In 2023, these third-party module sales represented approximately 99% of First Solar’s total net sales.

Leadership overview

Mark Widmar has been the CEO of First Solar since 2016. Under his leadership, the company has achieved significant milestones, including:

Strategic Growth: Expanded manufacturing capacity and increased R&D investments, positioning First Solar as a leader in thin film solar technology.

Improved Financial Performance: Improved financial health, with notable earnings per share growth and a strong balance sheet.

Innovation: Focused on advancing thin film PV technology, contributing to sustainability and eco-efficiency.

Policy Advocacy: First Solar has actively engaged in advocating for fair trade policies to support US domestic solar manufacturing.

Industry Overview

Solar energy is one of the fastest growing forms of renewable energy with numerous economic and environmental benefits that make it an attractive complement to and/or substitute for traditional forms of energy generation.

In recent years, the cost of producing electricity from PV solar power systems has decreased to levels that are competitive with or below the wholesale price of electricity in many markets. This price decline has opened new possibilities to develop systems in many locations with limited or no financial incentives, thereby promoting the widespread adoption of solar energy. Other technological developments in the industry, such as the advancement of energy storage capabilities, have further enhanced the prospects of solar energy as an alternative to traditional forms of energy generation.

In addition to these economic benefits, solar energy has substantial environmental benefits. For example, PV solar power systems generate no greenhouse gas or other emissions and use minimal amounts of water compared to traditional energy generation assets.

With this expected growth in the solar industry, the global thin film solar cell market size, according to Precedence Research, is expected to grow at a CAGR of around 8.4% from 2023 to 2032.

Porter’s 5 Forces

Competitive Rivalry – High

First Solar faces intense competition, especially from crystalline silicon module manufacturers, many of which are linked to China.

Bargaining Power of Suppliers – High

Several of First Solar’s key raw materials and components, in particular CdTe and substrate glass, are either single-sourced or sourced from a limited number of suppliers. As a result, the failure of any of such suppliers to perform could disrupt First Solar’s supply chain and adversely impact its operations.

Bargaining Power of Buyers – Medium

In 2023, Lightsource BP was the only customer accounting for more than 10% of their module business net sales. This shows that no single customer accounts for a significant portion (over 25%) of First Solar’s net sales. However, a large customer like Lighthouse BP may have considerable bargaining power over First Solar.

Threat of Substitutes – High

Crystalline silicon modules are one of the key substitutes to First Solar’s thin film modules. Such silicon modules may be cheaper than thin film modules due to Chinese state support and economies of scale.

Threat of New Entrants – Medium

New entrants to the industry will have to spend substantial amounts of money on capital expenditure to build up their manufacturing capabilities and R&D costs to develop their own PV modules. However, these costs may be offset by significant government subsidies and support, such as that seen in China.

Investment Thesis

1. The tax credits of the US Inflation Reduction Act (IRA) are expected to help maintain or even expand First Solar’s industry leading gross margin through to 2032.

The IRA, passed in August 2022, is a major US federal law aimed at addressing various economic and environmental issues faced by the US. It primarily focuses on reducing inflation, promoting clean energy, lowering healthcare costs, and raising revenue through changes to the tax system. The climate and energy initiatives of the IRA represents the largest investment in climate change mitigation in US history, with about $369 billion allocated to promote clean energy in the US. It includes tax credits and incentives for renewable energy projects, electric vehicles, energy-efficient home improvements, and investments in clean technologies like hydrogen and carbon capture. All of this is with the aim of reducing US greenhouse gas emissions by 40% by 2030, compared to 2005 levels.

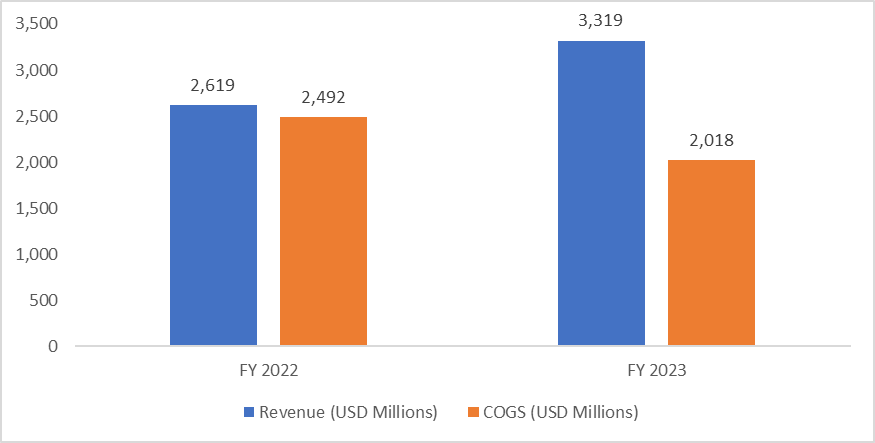

First Solar anticipates qualifying for the advanced manufacturing production credit under Section 45X of the IRA from 2023 onwards. This provides approximately 17 cents of tax credit per watt for each module produced in the US and sold to third parties. In FY 2023, the company has already recognised $687.2 million in Section 45X credits for FY 2023, which they used to reduce their Cost of Goods Sold (COGS) for FY 2023. This is because they actually sold their tax credits to a third-party (Fiserv Inc. (NYSE: FI)) and used the cash received to reduce their COGS for FY 2023 (See Fig. 4&5). Going into 2024, First Solar continued reduction in its COGS from tax credits has allowed First Solar to achieve industry leading gross margins as compared to its peers as of Q2 2024 (Fig. 3). With the 45X credits expected to extend to 2032, First Solar can tap into these credits to maintain or even expand its already industry leading gross margins through to 2032. This is expected to drive significant net income growth for First Solar going forward into the future.

Figure 3. Comparison of First Solar’s gross margins with comparable peers (as of Q2 2024)

Figure 4. Ways for First Solar to realise the benefits of its 45X tax credits

Figure 5. First Solar's Revenue and COGS comparison (FY 2022 & 2023)

2. The US IRA is expected to drive significant revenue growth for First Solar in the coming years.

The tax credits and incentives of the IRA is expected to drive significant growth in new solar projects in the US in the coming years. The US Energy Information Administration (EIA) forecasts that US solar power generation will grow 75% from 163 billion kilowatthours (kWh) in 2023 to 286 billion kWh in 2025. This expected huge growth in solar power generation is expected to drive demand for First Solar’s PV modules in the coming years. This is because US solar developers are incentivised to use US produced solar panels in their projects under the bonus credits scheme of the IRA. Therefore, I feel that First Solar, being the largest PV solar module manufacturer in the US, can effectively capitalise on this demand for US made solar modules in the coming years.

In fact, we might be seeing this demand manifesting itself through a substantial year over year (YoY) increase in First Solar’s contracted backlog at the start of 2024. At the start of 2024, First Solar’s total contracted backlog stood at 78.3GW. This amounted to an aggregate transaction price of $23.3 billion. First Solar expects to recognise these as revenue through 2030 as it transfers control of the modules to the customers. This represents an increase of around 27.5% as compared to its contracted backlog at the start of 2023 (61.4GW). Ultimately, this expected demand growth is expected to drive significant revenue growth for First Solar in the coming years.

Figure 6. First Solar's contracted backlog growth (2019 to 2023)

Catalysts

1. Possible Fed rate cuts over the coming years.

Possible multiple rate cuts by the Fed over the coming years may lower the cost of borrowing for solar project developers in the US. This may help to lower the cost of undertaking such projects and hence may lead to an uptick in such projects in the US. This uptick may drive demand for First Solar’s modules, which bodes well for First Solar’s revenue growth. This expectation of increased revenue growth may help to drive up First Solar’s stock price after the Fed rate cuts.

2. Possible exceeding of management’s sales revenue and diluted earnings per share (EPS) guidance over the coming years.

As of Q2 2024, First Solar’s management has reiterated sales revenue guidance of $4.4B to $4.6B and diluted EPS guidance of $13 to $14 for FY 2024. If First Solar is able to exceed this sales revenue and diluted EPS guidance for 2024 and for subsequent years after 2024, it may boost investor’s confidence in First Solar’s financial growth. This may help to drive up First Solar’s stock price in the coming years.

Financial Analysis

Analysis of past financials

Revenue

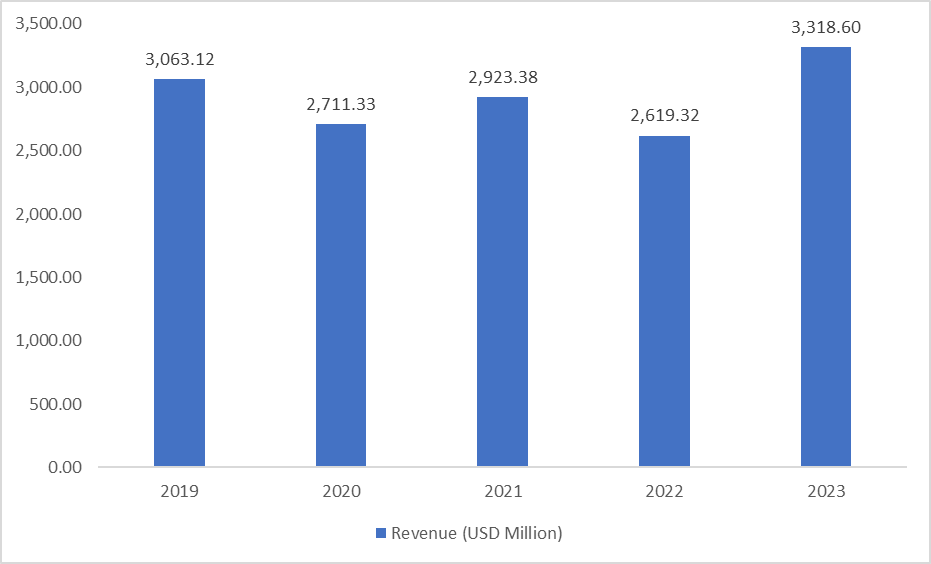

From 2019 to 2023, First Solar’s revenue has grown at a CAGR of around 1.62% (Fig. 7).

In 2020, it experienced a revenue decline of around 11.48%. This was mainly due to the global COVID-19 pandemic which caused disruptions across the solar energy sector. Supply chain disruptions, restrictions on construction activities, and delays in project timelines significantly impacted First Solar's ability to complete and deliver solar projects in 2020.

In 2022, it experienced a revenue decline of around 10.4%. The decrease in revenues for First Solar in 2022 was driven by a combination of delays in project timelines, and the company’s strategic shift away from its legacy project development business toward module manufacturing.

Figure 7. First Solar's Revenue (2019 to 2023)

Net Income

From 2019 to 2023, First Solar experienced a situation of negative net income in 2019 and 2022 respectively (Fig. 8).

In 2019, it experienced a situation of negative net income ($-114.93) due to the combination of high costs associated with the Series 6 module transition, production inefficiencies, delays in project sales, impairment charges, restructuring expenses, and pricing pressure in the solar industry.

In 2022, it experienced a situation of negative net income ($-44.17) due to inflationary pressures and supply chain disruptions. This caused the costs of key raw materials, such as glass, aluminium, and other components used in solar modules, to increase substantially. In addition to higher material costs, logistical challenges and rising transportation costs made it more expensive to source and deliver products.

Figure 8. First Solar's Net Income (2019 to 2023)

Credit Analysis

As of 2023, First Solar has an interest coverage ratio of 69.75. This means that First Solar has $69.75 of EBIT to cover for every $1 of interest expense generated by its liabilities. Furthermore, as of 2023, First Solar has a quick ratio of 2.69. This means that it has $2.69 of liquid assets to cover for every $1 of its current liabilities. Ultimately, I feel that all of this shows that First Solar is financially healthy and has little risk of a credit event occurring in the next 1 year.

Financial Projections

I project First Solar’s modules produced to grow based on the average of the high and low guidance given by management for FY 2024 to FY 2026. I then project modules produced to grow at a modest CAGR of 2% from FY 2027 to 2028. (Fig. 9)

Figure 9. Production and revenue forecasts (2024E to 2028E)

Valuation

The 5-year (5Y) target price of $453.39 is derived from a P/E valuation. Under this valuation, I forecast First Solar’s P/E ratio to normalise to its historical 10Y median P/E ratio of 23.48 (as of Sep 2024) (Fig. 10).

Figure 10. First Solar 5Y target price

Investment Risks

1. First Solar’s growth story hinges on the benefits of the IRA.

While a full repeal of the IRA is unlikely, a new Republican administration under Trump could hinder the climate law through executive action by tightening limits on tax credits, holding back some of its loans and grants, or revising treasury department rules that have not yet been finalised. If this happens, this may negatively affect First Solar’s gross margins and also its revenue growth going forward.

Mitigation: First Solar’s total contracted backlog stood at 78.3GW as of the start of 2024. This amounted to an aggregate transaction price of $23.3 billion. First Solar expects to recognise these as revenue through to 2030. This may help to mitigate a possible slowdown in revenue growth until 2030.

Furthermore, studies have shown that Republican states have actually benefitted the most from the Democrat-led climate law. This is a bias that could help soften the impact of a new Trump administration on the IRA. Republican states account for 58% of the projects announced under the IRA, Democrat states 32%, and swing states 10%, according to research from Fidelity.

2. Fluctuations in raw materials and logistics prices may negatively affect First Solar’s earnings.

Fluctuations in the prices of raw materials like aluminium, steel, and natural gas can increase manufacturing costs for First Solar. Increases in shipping, handling, and storage costs can also affect overall profitability.

Mitigation: First Solar employs various hedging instruments to mitigate the effects of such fluctuations (E.g. Commodity Swap Agreements; Forward Contracts etc.).

3. Fluctuating solar panel prices may pose a threat to First Solar’s revenue.

Solar panel prices may experience extreme pricing volatility due to various factors such as geopolitical risks and supply and demand cycles. This may negatively affect the selling price of First Solar’s modules.

Mitigation: First Solar primarily employs forward contracting to sell its modules. Forward contracting is a strategy where a company enters into agreements to sell or buy a product at a predetermined price for future delivery. This helps First Solar to secure a fixed selling price for its modules, protecting it against market volatility.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.