Initial Report: Funko Inc. (NYSE: FNKO), 30.4% 1-yr Potential Upside (Jun Rui NG, SC VIP)

Jun Rui NG presents a "SELL" recommendation for Funko Inc. based on the company's slowdown in its D2C pivot, margin contraction as short-term tailwinds reverse, and poor financial health.

Note: This idea is no longer actionable at the time of publishing as the memorandum was prepared in January 2025

EXECUTIVE SUMMARY

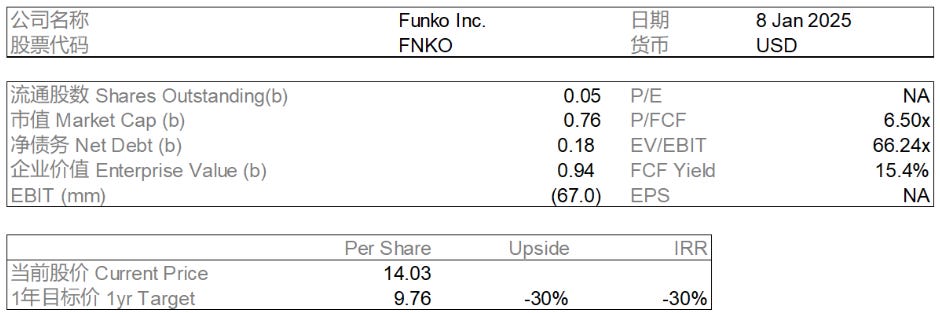

I am initiating coverage on Funko Inc. (NYSE: FNKO) with a SELL rating and a 1-year target price of $9.76, representing 30.4% downside from its current trading price of $14.03. This is based on Funko’s 5-year historical average EV/NTM EBITDA multiple of 8.72x (comps trade at 8.95x), applied to projected FY25 EBITDA of $89.5mm, assuming shares outstanding remains constant at 52.7mm. Funko is being hailed as a turnaround story as it attempts to grow its Direct-to-Customer (D2C) business after emerging from an inventory glut, but several issues loom: (1) slowdown in its D2C pivot, (2) margin contraction as short-term tailwinds reverse, and (3) poor financial health, exacerbated by two debt facilities maturing as soon as 2026.

BUSINESS DESCRIPTION

Funko Inc. (NYSE: FNKO) manufacturers and distributes licensed pop culture products such as collectibles, apparel, and toys. Funko manufactures most of its products in Vietnam, China and Mexico, and distributes its products across the United States, Canada and Europe via two channels: (1) big box & specialty retailers e.g. Amazon, Walmart, GameStop, and (2) its D2C website, funko.com. North America has historically accounted for ~70% of sales, while Canada and Europe account for the remaining 30%.

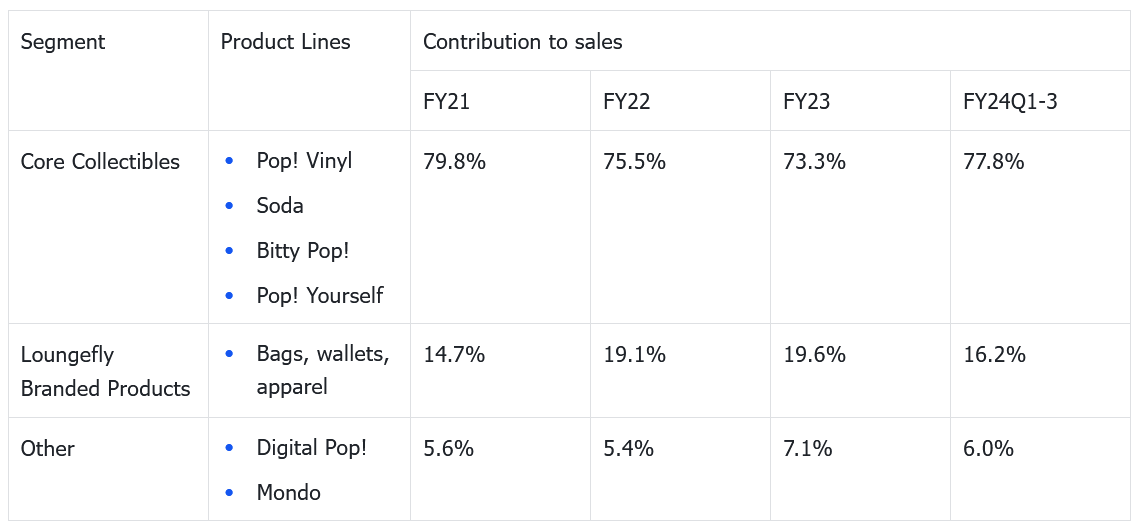

Funko reports on its product lines across three segments: (1) Core Collectibles, (2) Loungefly Branded Products, and (3) Other. While the contribution of the Core Collectibles segment to sales has been declining YoY, management has alluded to the Bitty Pop! and Pop! Yourself brands being key drivers of Funko’s sales engine moving forward.

In May 2022, private equity firm TCG and its consortium comprising of eBay, Robert Iger (former Disney CEO) and Rich Paul (Klutch Sports Group CEO), spent $263mm to acquire 12,520,559 Funko shares at $21 per share. This implied a valuation of 1.1x EV/LTM Sales and 8.2x EV/LTM EBITDA, multiples which Funko still trades near at. Pursuant to the agreement, (1) TCG Co-Founder Jesse Jacobs and Rich Paul were to join Funko’s board, and (2) eBay was to become the preferred secondary marketplace for Funko and partner with Funko to create exclusive product releases. Today, Rich Paul has left Funko’s board and the eBay partnership never materially impacted Funko’s growth. TCG has not adjusted its stake in Funko thus far.

Furthermore, Funko faced high management turnover over the past few years, which has resulted in inconsistencies in the company’s business strategy. Funko is currently managed by CEO Cynthia Williams and Acting CFO Yves LePendeven, who joined the company as recently as May 2024 and August 2024 respectively. Notably, Williams was previously the president of Hasbro’s Gaming Division, where she was criticised for amending Wizard of the Coast’s Open Gaming License (OGL), henceforth enabling Hasbro to receive a 25% royalty on the income of third party publishers and creators with annual sales exceeding $700,000. She was generally perceived as a scapegoat to make tough decisions for the company ahead of its 50-year anniversary.

NARRATIVE ANALYSIS

The street erroneously views Funko as a turnaround story. In 2023, Funko faced a content drought due to the Writers Guild strike, which coincided with an inventory glut owing to lower demand for products from large retailers. As a stopgap measure, Funko acquired short-term expansion space near its Buckeye facility to stage inventory and clear out its trailers, and found a third-party agent willing to accept the trailers on behalf of carriers, thereby lowering rental fees. Over the year, Funko halted the development of unprofitable product lines, eliminated 30% of stock-keeping units (SKUs), and carried out two rounds of workplace reductions. Despite these efforts, Funko’s fundamental business is waning and was only propped up in FY24 by non-recurring inventory releases and a recovering macro.

INVESTMENT THESIS

Slowdown of D2C pivot: Funko’s much-touted pivot toward its higher-margin D2C business appears to be losing momentum, as evidenced by YoY growth of the channel declining from 43% in FY23 to 6% (est.) in FY24. This slowdown comes despite earlier management commentary that products like Bitty Pop! (miniature figurines) and Pop! Yourself (custom figurines), both expected to drive topline growth through D2C, would invigorate this segment.

Price sensitivity: During FY24Q3 earnings, management commented that D2C sales “were kind of slow during full-price periods”, only picking up in September when a planned promotion was run. When further questioned, management conceded that this price sensitivity was primarily observed for Funko’s legacy Pop! figurines, which already are sold at fairly low price points from $12 to $15. This implies that the D2C segment relies heavily on discounts to drive volume. Even so, the overall revenue contribution is lacklustre.

Lack of transparency: Further compounding the issue, Funko ceased reporting D2C net sales figures since FY24Q1, instead reporting D2C as a percentage of gross sales, breaking continuity with past disclosures (the FY24 numbers used in the model were triangulated from other comments). While speculative, this change could be meant to obscure the D2C segment’s reliance on discounts and high return rates, which are excluded from gross sales but impact net sales. The lack of transparency and apparent decline in the D2C mix highlight potential headwinds for Funko’s ability to achieve the expansion originally envisioned from this channel.

Margin contraction: Since emerging from the pandemic in 2022, Funko’s gross margins have rebounded to pre-pandemic levels of 38% to 40%. In FY23Q4, former CEO Michael Lunsford cautioned that these margins would face natural limitations over time. However, throughout FY24, street expectations have been elevated by two primary factors: (1) declining freight costs, and (2) higher-than-anticipated sales of inventory reserves. I view both trends as transient, suggesting the current margin expansion may not be sustainable in the medium term.

Freight cost volatility: Lowered freight costs has been a key driver of margin expansion as the company emerged from the pandemic, accounting for 17% of cost of sales in FY23. While Funko subsequently benefitted from lower-than-expected freight costs and signs of stabilisation in FY24Q1, freight rates spiked sharply through Q2 and Q3, with major freight indices peaking in July 2024. The higher freight rates during the surrounding months would be capitalised onto the balance sheet for shipments made during that period and weigh on gross margins in FY25Q1 and Q2, which the street has overlooked.

Reserved inventory sales: In FY23, Funko recorded a $30.3mm inventory write-down, recognised as an increase in cost of sales. However, FY24 has seen unexpected gross margin favourability, with management attributing approximately 2.5 margin points in Q1 and Q2 to the monetisation of aged inventory reserves through value channels. While this unplanned windfall has temporarily supported profitability, this tailwind will unlikely extend into FY25. If the inventory release results in 2.5% margin favourability every quarter, I estimate that only ~$6mm out of the $30.3mm aged inventory will be left by FY25, thus the opportunity for further releases is rapidly narrowing, reinforcing the view that the current gross margin uplift is transient.

Higher SG&A: During the FY24Q3 earnings call, management floated specific initiatives such as further developing the current Enterprise Resource Planning (ERP) system and building a customer data platform to grow the D2C business through personalisation efforts. These would depress margins in the near-term. Furthermore, management also stated that the cost savings accrued from streamlining operating efficiencies thus far will be reallocated into ramping up marketing efforts for newer products e.g. Pop! Yourself. Therefore, I model for a 0.5% increase in SG&A as a percentage of revenues.

Poor financial health: Funko has two debt facilities owed to a large consortium maturing next year. They have the following features:

Financial covenants: Crucially, an amendment made in February 2023 imposed financial covenants requiring Funko to maintain: (1) a Net Leverage Ratio (NLR) of 2.5x, and (2) a Fixed Charge Coverage Ratio (FCCR) of 1.25x, starting in FY24Q1. Currently, Funko has a NLR of 3.5x, thereby contravening a covenant. Lenders have the right to enforce the credit agreement and demand repayment.

Low lender confidence: Furthermore, it is telling that since the inception of the credit agreement, the maximum amount borrowable under the RCF was adjusted downwards twice. Even if lenders do not eventually demand immediate repayment, Funko will likely remain in a poor liquidity position and be forced to restructure its debt on unfavourable terms.

STREET EXPECTATIONS

Topline growth: The street is modelling for FY25 sales to come in at $1,124mm, implying a growth rate of ~8%, largely driven by the Pop Yourself! and Bitty Pop! product lines. However, I am of the view that revenue contributions from both product lines cannot drive this level of growth, particularly when management has guided that wholesalers are ordering less as consumers are looking for value (which also explains why reserved inventory was sold off quickly). For my base case, assuming sales of evergreen products and the traditional Pop! product line declines by 4% in FY25, the ~$40mm step-down will offset the potential $90mm uplift from Pop! Yourself and Bitty Pop!, thereby driving topline growth of ~5%, below consensus estimates:

Pop! Yourself: In FY24Q3 earnings, management reported that over 1 million Pop! Yourself figures were sold in the last 12 months. As the average Pop! Yourself experience costs $30, the implied sales uplift is $30mm, which is 6% of management’s midpoint FY24 sales estimate of $1.04bn. When management expanded its D2C shipping capability to include Canada, average daily volume doubled. Assuming this momentum continues, Pop! Yourself can at best drive a revenue uplift of $60mm in FY25.

Bitty Pop!: In FY24Q2, management reported that sales of Bitty Pop! doubled compared with the same quarter last year, but provided little colour as to the contribution to sales. Seeing as it is described as a key revenue driver alongside Pop! Yourself in FY24, I model for a $30mm revenue uplift consistent with FY24 contributions, absent of any catalysts raised by management.

Lowered freight costs driving margin expansion: The street has largely ignored former CEO Michael Lunsford’s warning that gross margins would be capped around 38% to 40%. The consensus FY25 estimate is 40.4%, which in my view is overly optimistic given that the elevated freight rates from June and July 2024 will weigh down on FY25 margins. During the FY24Q3 earnings, management tried to allay the street’s concerns by stating that approximately 70% of current freight rates were under contract by the time of the earnings call, suggesting a degree of insulation from further volatility.

Timing: However, details on the timing and scope of these contracts remain unclear. If these contracts were not in place to cover the June and July 2024 shipments while freight rates were at their highest, the gross margins in 1H25 will be weighed down when those batches of inventory are sold. Even if those shipments were under contract, they would likely be unfavourable to Funko since they were negotiated when freight rates were increasing. This also means that these rates will be locked in even if the macro subsequently becomes more favourable, affecting margins as far down as 2H25. I therefore issue a more reasonable estimate of FY25 gross margins at 38%.

Capacity: Furthermore, fresh out of its inventory glut and operational streamlining, Funko currently has limited capacity to take on more inventory. In FY24Q3 earnings, management stated that if retailers push to get more products quickly into the United States as a response to tariffs, Funko would have difficulties coping. Under the unpredictable Trump administration, even the threat of tariffs might be sufficient to cause panic on retailers’ ends. Even if Funko is able to withstand a restocking rush, previously freed up working capital would be tied up in inventory again, weighing down on Funko’s already meagre free cash flow.

CATALYSTS

Potential unwinding: The partnership between TCG and the rest of the investor consortium in 2022 has largely dissolved at this point. However, Funko’s stock is currently surging on its turnaround story. If TCG accepts the fundamental weakness of Funko’s business and is seeking to recoup its losses, it might unwind its position as the stock nears $21, the price at which TCG bought the stock. This would apply downward pressure on prices.

Tariffs: Any announcement of harsher tariffs would place downward pressure on the stock. Beyond the fact that 1/3 of Funko’s products are from China, the company would be thrown into an inventory glut yet again as retailers rush to import as much as possible.