Initial Report: Indosat Ooredoo Hutchison (ISAT.JK), 24% 5-yr Potential Upside (EIP, Jordan GOH)

Jordan believes that Indosat will be able to ride the telco network infrastructure investments and break record-high earnings once they have found the solution to provide their services.

Executive Summary

1) Strong synergy from Merger with Hutchison 3 Indonesia in 2022 has yet to reap maximum benefits.

2) Heavy focus on asset-light strategy to strengthen Balance Sheet even further.

Company Overview

Indosat Ooredoo Hutchison (IOH, IDX: ISAT) together with its subsidiaries and affiliates provides cellular services, ICT solutions, data centers, Fiber to the Home (FTTH), electronic payment services, financial services, and other digital services. The company was formed through the merger of PT Indosat TBK and PT Hutchison 3 Indonesia in 2022. Since the merger, ISAT has become one of the leading telecommunication companies in Indonesia, just one spot behind Telkomsel, which has the largest market share.

Fig 1: Indosat Ooredoo Hutchison Coverage Map (Source: Medium 2023)

Business Segments

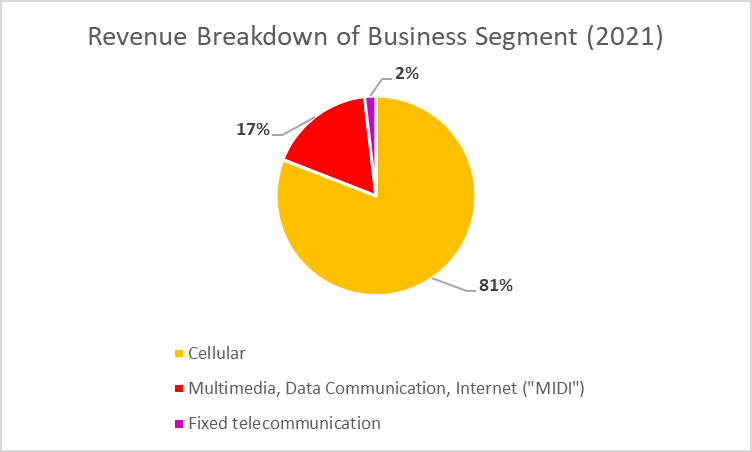

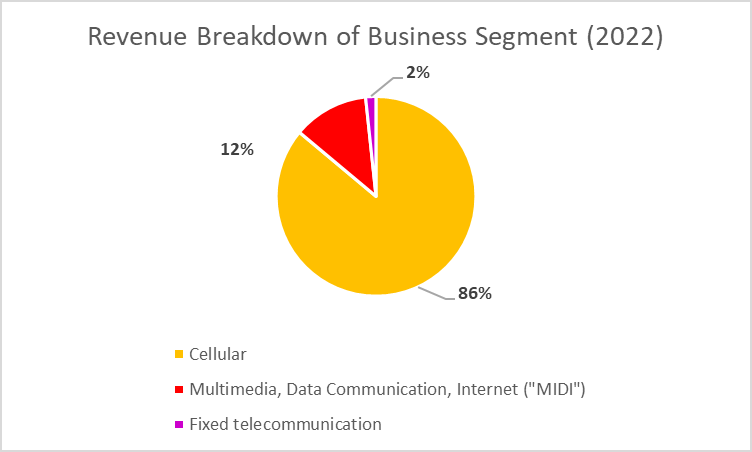

(IOH) operates in three main business segments, with Cellular business (86%) predominantly bringing the bulk of the revenue in 2022.

Fig 2&3: Revenue Breakdown of Business Segments in 2021 & 2022

1) Postpaid and Prepaid Products:

This segment includes a wide range of high-quality data and mobile voice solutions available on 2G, 3G, 4G, and 5G broadband cellular networks. These products are marketed under the main cellular retail brands IM3 and Tri.

2) International and Fixed Telecommunication:

IOH offers International Direct Dial (IDD) services, international roaming, and fixed line services. These services allow customers to communicate with others around the world or within the country.

3) Multimedia Interactive, Data, and Internet (MIDI) Services:

This segment provides services through its subsidiaries, including Lintasarta, IM2, and ISPL (Indosat Singapore Pte. Ltd.). It offers high-speed point-to-point International and Domestic Leased Circuits with broadband and narrowband capacity, IPVPN (Internet Protocol-Virtual Private Network), and MPLS (Multiprotocol Label Switching)-based services. Additionally, it provides Hybrid Cloud solutions, Managed IT services, Disaster Recovery Centre, Data Centre Services, and iSOC Security services.

Additionally, IOH provides IT services and software contracts, including IT outsourcing, business process outsourcing, systems integration & consulting, and more. It also offers IT software contracts in areas such as Enterprise applications, IT Security, Information Management, Cloud Computing, and IoT.

Revenue Drivers

For IOH's top-performing business segment, the company has improved network coverage as well as spectrum from post-merger network integration, creating a clear competitive advantage in the market. This was the catalyst for the high growth that IOH experienced in 2022 in their cellular business segment.

At the end of 2022, IOH’s total cellular sales grew by 58% to Rp40,243 billion. With the addition of close to 6 million new cellular customers, our total number of customers reached 102 million. This increase was attributable to the addition of new cellular subscribers, growth in data usage from IM3 and Tri, and improvements in network coverage and quality. IOH’s revenue from data services increased by 61% to Rp37,001 billion in 2022. Therefore, cellular revenue continued to be the largest revenue contributor.

Another metric to look at in the telecommunication industry is the Average Revenue Per User (ARPU) which has been increasing by 2.5% in 2023 compared to 2022. ARPU is the metric to calculate how profitable a mobile service providers at individual subscriber level. Given the dynamics of the mobile service pricing, ARPU serve as the simple metric to understand the price strategy from each company. players. In the case of IOH, they have dominant revenue from data service —The data service revenue price is relatively lower compared to voice and SMS services.

Fig 4: Cellular Services Operational Highlights

Cost Drivers

IOH has multiple cost drivers but the main bulk of their cost in their business goes to their operations. Telecommunication is an industry with high OPEX, requiring extensive network infrastructure to provide their cellular and fixed telecommunication services. Frequency fees, interconnection expenses, maintenance of infrastructure expenses, utility and rental expenses, circuit lease expenses. In 2022, cost of services made up to 45.2%.

Due to the increased number of network coverage from increased network infrastructure, depreciation and amortisation of their fixed assets are also a large component of IOH cost drivers. In 2022, Depreciation and amortization made up to 29.3%

Competitor Analysis

There are only 4 main players in the Indonesian consumer mobile sector today: Telkomsel, Indosat, XL, and Smartfren.

In general, Telkomsel is the leading player in the industry followed by IOH, which comes to a close second. There is evidently a large gap between IOH and the third spot in the telco market, when using certain metrics like 1)Mobile Customer Market Share, 2)ARPU, 3)Base Transceiver Station & 4)Spectrum to measure the achievements of the aforementioned Telco companies in Indonesia.

Fig 5: Mobile Customer Market Share (Source: Medium 2023)

Industry Analysis

Rise in connectivity after Covid & Expanded Network Coverages in rural areas of Indonesia

The Indonesian telecommunications industry experienced a surge in growth as a result of the lifting of pandemicrelated restrictions and the increase in customer mobility. With the forecasted rise in overall industry traffic by 12%, Indonesia saw an increase in mobile connections by 3.6% or 13 million, reaching a total of 370.1 million users in January 2022, which equals to 133.3% of the population. Furthermore, the median mobile internet connection speed in Indonesia experienced a 27% growth, reaching 15.82 Mbps in January 2022. Despite the promising growth of the telecommunications industry in Indonesia, there remains ample room for further expansion. Currently, only around 70% of the total population in Indonesia has access to mobile data, and many rural areas and small to medium-sized enterprises remain offline or in the early stages of digital implementation. With an average monthly data consumption of 13-14 Gb, the potential for increased cellular connectivity is substantial.

Investment Thesis

1) Strong synergy from Merger with Hutchison 3 Indonesia has yet to reap maximum benefits

Network integration was one of the vital post-merger challenges for IOH and a successful network integration would meant that operation would be the most efficient. The strategy comprises of a three-year framework agreeement for purchase of telecommunication system hardware, software and related services with the company Ericsson, Huawei and Nokia. The network was a strategic asset for IOH, allowing them to expand their coverage and improve overall customer experience. With the use of Multi-Operator Core Netowrk (MOCN) technology that was carried out in more than 46 thousands sites throughout Indonesia, IOH conducted a successful network integration project. With the integration of the networks, IOH recorded an increase of 30% in sites serving customers and improved coverage in previously underserved areas throughout 2022. The integration has positively impacted customer experience across Indonesia.

The completed network integration in 2023 spearheaded IOH's strong 2023 financial performance and allowed the company to redeploy capital into increasing their network infrastructure to meet rising demand. The company's capital spending now averages $800 million a year. In addition to expanding its wireless network coverage to areas such as Kalimantan and the planned new capital of Nusantara, it also looks to bring high-speed fifth- generation wireless beyond the current handful of cities. Ultimately, this move will enable IOH to reach into the more rural areas of Indonesia and provide their cellular services to people. Overall, the synergy of the merger has been strongly positive in 2023 and shows no signs of stopping. I foresee that the company will be able to cut further operational costs as they follow through with their post merger network integration plans. The decision to come up with digital products to meet rising demand for digitalisation in Indonesia will put IOH ahead of their peers.

2) Heavy focus on asset-light strategy by rapid expansion of Partnership ecosystem to strengthen Balance Sheet even further

IOH has plans to make significant contributions to the growing Internet economy in Indonesia, and one of its strategies is to have an asset-light to support their growing brand equity, as a leading player in the market who has been around for over 50 years. This can be achieved primarily through strategic partnerships and collaborations.

These collaborations revolve around their goal to create a competitive advantage with their 5G network coverage in the upcoming years, partnering with several global ICT providers including the likes of Huawei and Tech Mahindra. These digital companies are able to allow IOH to tap into their advanced technology capabilities and expertise, enabling IOH to provide their customers with high-quality network assurance, improve value and customer experience. In that manner, IOH is able to deliver long-term cost savings and have increased customer loyalty.

To keep up with the ever growing consumer demand for their cellular services, and to adhere to the asset-light strategy, IOH have established Data Centers by forming a joint venture with BDx and Lintasara. Without the need to invest huge amounts of capital into building their own data centres, the partnerships forged will allow IOH to benefit and leverage on their partners' data center infrastructure for the company's day-to-day operations. Google Cloud is also one of IOH's partners to provide cost efficient cloud-based with 5G enabled digital solutions to micro,small and medium enterprises (MSMEs).

Increasing operational efficiency and having a strengthened balance sheet would mean that IOH is able to allocate more resources to their other business segments to generate further revenue. IOH is also planning to expand on their digital service segment and evolve from a telco to tech company and dive into smart-city technology. Actively seeking a competitive advantage will allow IOH to be able to catch up and match against the industry's leader Telkomsel.

Valuation

During the upcoming 5-year period, I foresee IOH breaking record highs EBITDA as they continue to improve their operational efficiency and have a concentrated strategy to take away market shares from Telkomsel. Supported by the Indonesian Government's vision to make Indonesia one of the world's leading digital powerhouse, IOH's 5G services as well as their digital service business segment, will continue to build up revenue. Assuming a conservative growth rate of 1.5% in IOH's net income, taking the forward 5-year P/E industry average, the implied value per share for IOH will reach IDR 11,621.3, a 24% upside from the current share price today.

Economic Moat

IOH's economic moat has been on the clear rise post-merger and they come mainly from two sources: (a) Operation efficiency & (b) Synergy with Partners.

Fig 6: Operating Expenses of Business Segments

Operation efficiency - Even though the cost of services increased from 43.6% in 2020 to 45.2% in 2022, it was due to rapid expansion in 2022 post-merger. The increase in revenue brought in for 2022 in comparison to 2020 is more than proportional to the increased cost of services. I expect that operational efficiency will only improve for IOH over time as the merger materialises even further.

Synergy with Partners - As mentioned in the investment thesis (1), synergy from exclusive partnerships is an economic moat itself. Diligently handpicking the right partners will enable IOH to leverage their partners' expertise and infrastructure to propel their growth.

Risk & Mitigation

1) Regulatory Risks: The telecommunications sector is heavily regulated, and changes in regulations can impact IOH's operations. For instance, changes in spectrum allocation policies or regulatory requirements for network infrastructure can affect IOH's ability to expand its services. Mitigation strategies could include staying abreast of regulatory developments and engaging in proactive dialogue with regulators.

2) Competitive Risks: The telecommunications industry is highly competitive, with frequent entry and exit of players. Competitors may launch aggressive pricing strategies or introduce innovative products, potentially eroding IOH's market share and start ups might eventually be a threat if customers were to ignore brand equity and choose a product based on the value they are getting. Mitigation strategies could include investing in product differentiation and continuous innovation, which IOH has already been doing for the past year since the merger.

3) Technological Risks: Rapid advancements in technology pose a risk to IOH's operations. For example, if competitors adopt newer technologies faster than IOH, it could disadvantage IOH in terms of network efficiency and customer experience. Mitigation strategies could include investing in cutting-edge technology and forming strategic partnerships with technology leaders. IOH's partnership with Cisco Systems and the most recent partnership with China's state-owned China Mobile to leverage on their competence as infrastructure investment costs pile up.

4) Operational Risks: Operational issues, such as network failures or cyberattacks, can affect IOH's reputation and customer trust. Security of Data is important to IOH's customers and these risks will cause them to lose trust and even turn to other competitors' services in the market. Hence, building a resilient and secured network is equally as important as providing fast and reliable network to customers. Mitigation strategies could include robust security measures and having contingency plans in place.

ESG Assessment

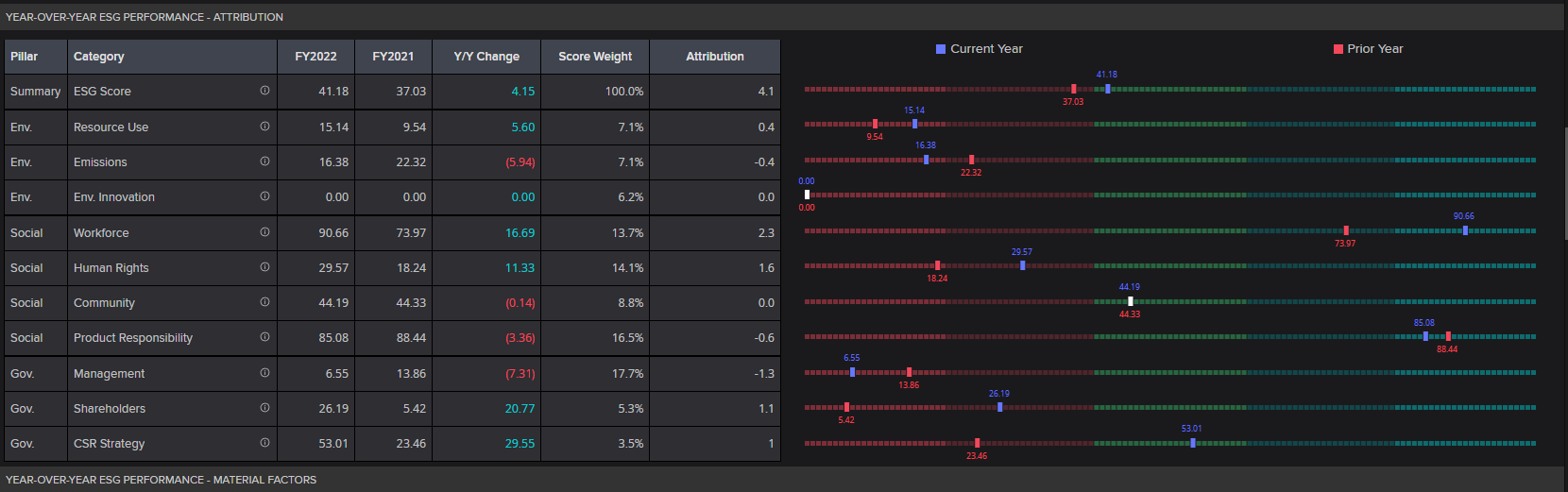

Fig 7: ESG Performance for 2022 & 2021 on Refinitiv

From the figure, you can see that ESG performance for IOH improved generally from 2021 to 2022. Although the emissions from FY2021 are lower than FY2022, this can be explained by the massive merger. Surprisingly, this increase in scope(1) + scope(2) is not as high as expected from the merger, given that IOH's customer base had expanded massively.

Fig 8: Annual GHG Emissions of Indosat Ooredoo Hutchison on Refinitiv

A positive note would be that from Fig 7, IOH seems to be doing relatively better in Diversity & Inclusion (D&I). Having a diverse representation in the company will only allow positive feedback loops, and to build a strong foundation of company culture, especially since the company is 'new' after the merger. It will be interesting to see the Annual GHG Emissions in 2023 where data will be more accurate as they consolidate and identify areas to minimise as much GHG emissions from their core businesses.

Conclusion

Considering that Indonesia will be one of the leading economies soon in 2050 and how the Indonesian government is pushing the digital economy agenda aggressively, IOH will be able to ride the telco network infrastructure investments and benefit positively from it. I feel that IOH will be able to break record-high earnings once they have found the solution to provide their services to the growing MSMEs and, of course, when securing customers from the more rural areas for their cellular services.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.