Initial Report: Luckin Coffee (OTCMKTS: LKNCY), 26% 3-yr Potential Upside (Ryan LEE)

Ryan presents a "BUY" recommendation based on its (1) ability to weather through major events, (2) rapid store expansion and cost improvements and (3) low prices and targeted marketing.

LinkedIn: Ryan Lee

Recommendation

Luckin Coffee (“The Company”) has seen rapid growth since its Nasdaq delisting in June 2020 as a result of accounting fraud (inflated sales by US$310m). After its delisting, the company removed key management involved in the scandal and the new management team led by Guo Jinyi (CEO) and Jing An (CFO) has done well in leading Luckin’s recovery from the scandal and the pandemic with rapid store expansion and unique product innovations. Accounting for a variety of macroeconomic, financial and operating metrics, I would like to propose a BUY for Luckin coffee due to its (1) ability to weather through major events such as the COVID-19 pandemic better than its competitors, (2) rapid store expansion and cost improvements and (3) low prices and targeted marketing.

Business Overview

Founded in 2017 and headquartered in Xiamen, China, Luckin Coffee (OTCPK:LKNC.Y) is a retailer of freshly brewed coffee such as Americano, Latte, Cappuccino etc. and specialty coffee based on market and seasonal trends such as coconut milk latte products, tea drinks, pre-made beverages and pre-made food items, such as pastries and snacks. Moreover, the company offers Luckin Pop premium instant coffee and inspirational cups through mobile apps and e-commerce platforms. Customers can purchase their products via the Luckin mobile app and pick up their coffee from the pick-up and relax stores that Luckin Coffee operates.

Business Model

Luckin Coffee’s adopts a cashless retail model utilising their mobile app to reduce the need for cashiers and increase convenience for customers that can purchase and collect their coffee from Luckin’s pick-up stores. As of 31 December 2023, Luckin had 10,470 pick-up stores (98.5%) and 158 relax stores (1.5%) strategically located in areas such as office buildings and shopping districts with high human traffic. Pick-up stores are smaller (20-60 square metres) with lower rental and decoration costs due to their small set up. Relax stores are larger (more than 120 square metres) and are used for branding purposes. Luckin also selectively partners with retail partners to explore new markets (e.g. lower tier cities) with limited capital requirements before opening their own stores.

Products

Luckin Coffee sources premium Arabica coffee beans from suppliers in Brazil, Colombia and China etc. and has been constantly innovating and developing new products, launching 80 new SKUs in 2023 coupled with blockbuster products such as Coconut Milk Latte. Some notable product series include Coconut milk, Velvet, Luckin Exfreezo and the Chinese tea coffee series.

Competition

Competition in the retail coffee industry is intense with Luckin Coffee facing intense competition from players such as COTTI COFFEE, Starbucks, KCOFFEE (KFC) and Costa Coffee in China.

COTTI COFFEE: Founded by the ex-founders of Luckin Coffee Lu Zhengyao and Qian Zhiya in 2022 with 7,000 stores nationwide. The ex-founders have been using the original strategy of Luckin to expand rapidly through cash-burning marketing campaigns (e.g. collaboration with Moutai), locating its stores near Luckin coffee stores and offering their products at low prices.

KCOFFEE: Operated by Yum China where they began serving KCOFFEE in-store in 2015, serving ~170 million cups per year by 2021. KFC China opened its first standalone KCOFFEE outlet in Shanghai in October 2022 and scaled the concept to 200 stores. The company is planning to open more than 1,200 stores annually over the next three years.

Cheap and fast coffee appears to be favoured by young Chinese consumers illustrated by the rapid growth of COTTI COFFEE and KCOFFEE compared to the premium coffee model at cafes provided by Starbucks and Costa coffee.

Starbucks: Sought to establish a first mover advantage when it opened its first cafe in China in 1999. However, Luckin Coffee that opened in 2017 had 3680 stores by fall 2019, compared to the 4130 stores that Starbucks built within 2 decades. Luckin’s business model of rapid store expansion to increase the volume of customer purchases coupled with the convenience it provides customers through its mobile app and delivery services has allowed it to grow at an extremely fast pace to surpass Starbucks. We must note however, that Starbucks branding is on providing premium coffee and environment for customers to relax in compared to Luckin’s cheap coffee that can be picked up or delivered to customers.

Costa Coffee: British coffee shop chain that entered the China market in 2006. Focused on providing premium coffee based on the Starbucks model with ~400 stores in China as of 2022. It had a target of opening ~2500 stores by 2022 but was not able to do so due to tough competition and impact from the Pandemic. Costa coffee has tried various innovation initiatives such as offering drive-thrus in their stores and producing ready-to-drink products like coconut-flavoured coffee launched in 2023.

It is evident that the premium coffee business model adopted by Starbucks and Costa do not work well in China as younger consumers that are more inclined to drink coffee value convenience via smartphone technology, lower prices and more innovative drink products that Luckin Coffee is actively addressing.

Investment Thesis

(1) Ability to weather through major events such as the COVID-19 pandemic better than competitors: Luckin’s app-focused business model provided it an advantage over competitors like Starbucks and Costa coffee that rely on in-store purchases. More customers were inclined to order via the Luckin phone app and collect their coffee from pick-up stores. This is illustrated from net revenue growth from RMB 1544.4m – 2488.9m (+61.1%) from 1H20 – 2H20 and RMB 3182.5m – 4782.9m (+50.3%) from 1H21 – 2H21 compared to previous same time periods of growth (~28.0% - 34.0%).

Its strong focus on technology and its online payment platform coupled with marketing, promotions and discounts on the platform sets itself apart from competitors like Starbucks and costa coffee that do not have such a strong online platform. Moreover, the company recovery displays positive signs that it is resilient during such major events such as a pandemic and provides confidence that it can tide through similar situations compared to competitors due to its online payment business model.

Technology risk: Given that Luckin is heavily reliant on its cashless app payment system, it must ensure that constant checks are maintained so that the system will not face any faults or delays. Technical issues could affect the reliability of the technology that Luckin prides itself upon and lead to reduction in sales as people are not able to make purchases. Moreover, given that Luckin does not usually accept cash payments, this may pose a concern if such technical down periods such as the Microsoft CrowdStrike incident occur during peak quarters in Q2 and Q3. Keeping up with news updates and personally using the Luckin coffee app to make purchases in their Singapore would help in gaining a better understanding of the technology and if there are any potential issues that may arise.

(2) Rapid store expansion driving topline growth and operating expense improvements: Luckin Coffee’s rapid store expansion strategy using smaller pick-up stores has allowed it to capture a larger volume of customers per month which has been driving net revenue growth (L4Y 83.5% CAGR) from RMB 4033.42m – 24,903.17m from FY20 – 23.

Figure 1: Store operating metrics

As seen from the figure above, the self-operated stores that drive product sales are driven inorganically through the increase in new store openings that increase the average monthly transacting customers rather than organically through a greater number of customers in existing stores. This is illustrated through the decrease in same store sales growth from +94.85% in 1Q21 to +13.5% in 4Q23.

Gross margins have been trending at ~59.0% - 60.0% (as a % of net revenue) from 3Q21 to 2Q23 (gross margins declined from 3Q23 – 1Q24 at ~50.0% - 56.0% due to an increase in COGS as a result of rising coffee prices arising from El Nino conditions leading to drier weather (recovered back to ~60.0% in 2Q24 with a slow transition to La Nina conditions).

Additionally, despite Luckin’s rapid store expansion, it has seen improvements in its operating expenses (as a % of net revenue) apart from delivery expenses from FY20 – 23 as seen from the figure below. This has led to Luckin experiencing improvements in its EBITDA margin from (58.07%) to 14.58% from FY20 – 23. This is a positive sign that Luckin has been able to manage its store rental expenses and sales & marketing expenses (core to Luckin’s expansion strategy) despite rapid expansion. Store rental expenses that include (store rental, employee and utilities expenses) also saw improvements as a (% of net revenue) by +22%. Additionally, sales and marketing improvements by +13% (as a % of net revenue) could have been driven due to topline growth with the increased investment in branding via multiple channels.

Risk of rising costs and expenses: The company’s improvement in profitability is very much reliant on its topline net revenue growth, that is driven by rapid store expansion and the volume of product purchases. Luckin must ensure that they are able to manage their COGS and operating expenses well in the future given the seasonality of purchases where sales are generally lower in Q1 and Q4 of each year given that most people travel during the new year and are not present at their office workplace during these periods.

The team managing suppliers must actively negotiate for better terms to lower the COGS to make new innovative products e.g. Brown sugar boba latte and extend or maintain the accounts payable days. The COGS (as a % of net revenue) has improved by 5.73%, but there present more room for improvement and slight concern with the language barrier and the effectiveness of negotiations given that most of the management staff is not fluent in English (illustrated during the transcript recordings where most of the management team spoke in Chinese and required a translator). Negotiations with a translator may be less effective if the parties representing Luckin cannot speak English and are negotiating with suppliers from Brazil.

Lower rental costs in China Tier 1 cities: The company’s rapid expansion may be driven by lower rental prices in Tier 1 cities such as Beijing (-1.28% QoQ), Guangzhou (-1.28% QoQ) and Shanghai (-2.12% QoQ) in 3Q23. If the lower rental prices persist, this will help in driving cost improvements in store rental expenses for Luckin coffee and allow it to maintain its pace of rapid store expansion in areas with high human traffic in Tier 1 cities where consumers have higher income and purchasing power. Observing the rental prices in Chinese tier 1 cities for the next few quarters is key to observing the impact of this catalyst.

(3) Low prices and targeted marketing: Luckin Coffee has invested a substantial amount of capital in sales and marketing to boost its branding. This has resulted in strong branding in a short span of 2 years since its inception in 2017 and has allowed it to tide through from bankruptcy after the accounting fraud scandal and through the pandemic period. Some examples include the collaboration with Moutai and the release of the Jiangxiang Flavoured Latte launched in September 2023 that sold 5.42m cups on the release day and 45.83m cups at the end of 2023 (RMB900m sales). The Luckin Coffee x Kweichow Moutai “Four Seasons and Eight Solar Terms” theme store was also launched in April 2024. Such initiatives have allowed to attract more younger customers that are more open to trying more unique coffee products.

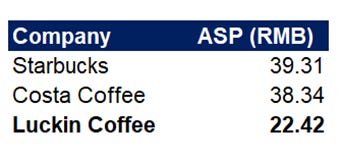

Moreover, Luckin is able to price its coffee products at a lower average price compared to key competitors like Starbucks and Costa coffee as seen from the figure below.

Figure 2: ASP of key players in the China retail coffee market (Source: China Ping An Group)

Risk of maintaining low prices: Possible increase in COGS due to rising coffee prices arising from weather conditions such as droughts, floods, fires etc. could affect the gross margins and profits of Luckin coffee given that it would be hard for the company to increase prices in the event of a rise in COGS. Management will need to take into account of such conditions such as the transition from El Nino to La Nina and how these would affect the countries such as Brazil and Columbia where Luckin sources premium coffee beans from. Possible diversification with alternative backup suppliers in the event of supply shocks and high coffee bean prices need to be in place to reduce the impact when these situations occur.

Expected lower temperatures due to La Nina: However, the rise in coffee bean prices is likely to mitigated and catalysed by the expectation of La Nina in 2H24 where temperatures are likely to cool from the hot El Nino period. This La Nina period is expected to last for 9-12 months and would maintain lower coffee bean prices in the key supplier regions such as Brazil so that Luckin coffee can maintain its COGS at ~(40.0%) and maintain its low pricing compared to its peers. Tracking the impact of La Nina and coffee bean prices in Brazil etc. via USDA through weather prediction models is key to observing how the prices of coffee beans and COGS will be affected.

Valuation

Based on a trading comps analysis, I have identified the closer peers of Luckin to be Starbucks, Tim Hortons, McDonalds, Yum China Holdings and Nayuki holdings based on their geographic presence in China, the coffee and food products that they sell as well as the market cap of these businesses. The multiples that the peers are trading at can be seen below:

Luckin Coffee Trading Comps (Source: Capital IQ)

I decided to use the higher range of the EV / NTM EBITDA multiples for the valuation of Luckin Coffee based the current trajectory of growth which gives me conviction that they should be valued at a higher multiple. Based on the EV / NTM EBITDA multiples, I decided to use a 19.0x EV / NTM EBITDA multiple. At 19.0x, it would yield an intrinsic value per share of US$29.0 per share, implying an upside of +25.81% based on the current stock price of US$23.05 per share.

Conclusion

In summary, I recommend a BUY for Luckin Coffee based on the 3 key reasons mentioned above coupled with the expected valuation in the next 3 years. With the company's strong resilience in major events, its rapid store expansion and low prices with targeted marketing, I am confident in the company's ability to grow and achieve its target price to achieve the expected returns.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.