Initial Report: Norwegian Cruise Line Holdings Ltd (NYSE: NCLH), 84.5% 5-yr Potential Upside (Aloysius LIM, EIP)

Aloysius LIM presents a "BUY" recommendation for Norwegian Cruise Line Holdings Ltd based on its fleet expansion programme, industry tailwinds, and financial de-risking.

Executive Summary

I am initiating coverage on Norwegian Cruise Line Holdings Ltd. (NCLH) with a Buy recommendation. NCLH is the world’s third-largest cruise operator, capturing approximately 13% of global cruise line revenue. In 2024, the company achieved record revenues, growing 11% year-over-year despite only a 3% increase in capacity. NCLH operates three distinct brands, Norwegian Cruise Line, Oceania Cruises, and Regent Seven Seas Cruises, targeting mainstream, premium, and luxury cruise segments, respectively. Robust travel demand has driven occupancy rates above 100%, with FY2024 occupancy at 104.9%, reflecting strong consumer interest and pricing power. Management’s “Charting the Course” strategy focuses on margin expansion and targets adjusted EPS of ~$2.45 by 2026, implying a 30%+ CAGR from 2024 levels. At current levels, NCLH is trading at $19.89 per share, significantly below its intrinsic value of $36.70 per share, derived using a WACC of 10.44% and a growth rate of 3%. This indicates a substantial upside potential of 84.5%, making it a compelling long-term investment opportunity.

Company Overview

Norwegian Cruise Line Holdings operates a portfolio of cruise brands with a combined fleet of 32 ships (~66,500 berths) visiting 700+ destinations worldwide.The company is domiciled in Bermuda with headquarters in Miami, and it primarily serves North American and international cruise markets.

Business segments

NCLH’s operations are divided among three cruise brands, each targeting a different customer segment and price point:

Norwegian Cruise Line (NCL): The flagship brand with ~19 contemporary ships ranging from medium to mega-size (2,000–4,000+ passengers). NCL offers “Freestyle Cruising” – a casual, resort-style experience appealing to mainstream and family travelers. Itineraries cover popular regions (Caribbean, Alaska, Europe, etc.)

Oceania Cruises: A premium cruise line with ~8 mid-size ships (typically 600–1,250 guests) known for destination-rich itineraries and culinary focus. Oceania targets upscale mature travelers with an interest in fine dining and immersive global itineraries.

Regent Seven Seas Cruises: An ultra-luxury line with ~6 all-suite ships (~500–750 guests each) offering all-inclusive, high-end experiences. Regent’s product features gourmet cuisine, personalized service, and exotic itineraries (world cruises, remote destinations) at top-tier pricing.

All three brands are supported by centralized corporate functions. Financially, NCLH reports as one operating segment (cruise vacations) with revenue primarily broken out into Passenger Ticket sales (~two-thirds of revenue) and Onboard & Other revenue (~one-third, from sales of drinks, casino, excursions, etc.).

Revenue drivers

Capacity and Occupancy: The fundamental driver of revenue is cruise capacity (available passenger cruise days) and how fully it is utilized. In 2024, NCLH operated at an average 104.9% occupancy (meaning ships were filled slightly above double-occupancy capacity) reflecting pent-up demand post-pandemic. Going forward, capacity is set to grow in 2025 with new ship introductions, and further in subsequent years as NCLH has eight newbuilds on order through 2027 adding ~20,000–25,000 berths.

Pricing (Net Yield): NCLH has demonstrated strong pricing power, evidenced by a record Net Yield increase of 9.9% in 2024. Net Yield (adjusted revenue per capacity day) is driven by ticket prices, onboard spending, and itinerary length. Drivers of pricing include the quality of ships and itineraries, demand relative to supply, and value-add offerings (e.g. beverage packages, specialty dining, etc.). In 2024, robust consumer demand and limited industry capacity growth enabled higher fares across all brands. The company expects continued pricing strength; for 2025 management guides Net Yield growth of ~3% on top of added capacity.

Onboard Spending: Revenue is further enhanced by onboard expenditures by guests. This includes alcohol and beverages, casino gaming, shore excursions, spa services, retail shops, and internet packages. Onboard revenue per passenger has been rising as guests indulge in vacation experiences. NCLH reported strong onboard revenue in 2024, aided by initiatives like bundled offerings (e.g. NCL’s “Free at Sea” package) that encourage pre-cruise upselling. Growth in onboard revenue directly boosts total yield with minimal additional capacity.

Itinerary Mix and Length: Deploying ships on higher-yield itineraries (such as destination-intensive cruises or peak-season sailings) also drives revenue. NCLH’s ability to vary deployment such as the Caribbean in winter, Europe/Alaska in summer, etc. helps maximize yield. Longer cruises and exotic itineraries generally command higher rates. For instance, Regent’s world cruises (which can span 100+ nights) generate substantial ticket revenue per passenger. As international travel fully normalizes, itinerary optimization remains an important lever for revenue growth.

Cost drivers

Operating a cruise line is asset- and labor-intensive, with significant fixed costs. Key cost drivers for NCLH include:

Fuel Expense: Marine fuel is one of the largest variable costs, coming in at 9% of the OPEX in FY24 alone. NCLH is likely to consume ~990,000 metric tons of fuel in FY2025, and fuel prices (net of hedging) would average at ~$722 per metric ton. Volatility in global oil prices can materially impact cruise profitability. To manage this, NCLH employs a hedging program – 56% of 2025 fuel consumption is hedged at ~$597/ton, and 21% of 2026 at ~$526/ton, providing some protection against fuel price spikes. The company is also investing in more fuel-efficient ships (including a future methanol-capable vessel) to reduce consumption per capacity day. Nonetheless, fuel remains a swing cost that can affect voyage margins.

Crew and Payroll: Cruise ships are labor-intensive, with thousands of crew across the fleet (NCLH has ~41,000 employees total), making up ~17% of FY24 OPEX. Salaries, benefits, and training for shipboard and shoreside staff constitute a significant expense. Labor costs tend to rise over time (and there is upward pressure in a tight labor market). NCLH’s recent results reflect higher crew costs partly due to reinstating full staffing and incentive pay post-pandemic. The company manages this via efficient crew scheduling and productivity improvements, but maintaining high service levels (especially on luxury brands) limits flexibility to cut payroll.

Food, Beverage & Hotel Operations: Operating expenses include provisioning the ships (food, beverages, amenities), cabin supplies, entertainment, and onboard maintenance. These costs generally scale with passenger volume. NCLH has indicated that its Adjusted Net Cruise Cost Excluding Fuel (which includes all operating costs per capacity day except fuel) was ~$160 in 2024, up only ~1% year-over-year when excluding an elevated dry-dock impact. This minimal increase demonstrates effective cost control in food, hotel, and logistics expenses.

Marketing and Commissions: Travel agent commissions, advertising, and promotions to attract bookings are another cost component. As bookings have surged, NCLH spent more on marketing in 2024 to stimulate demand. Distribution costs (e.g. paying commission on higher ticket prices) do rise with revenue – a factor in net yield calculations. However, direct booking channels and past-guest marketing (loyalty programs) are being leveraged to improve cost-efficiency of sales.

Economic Moat and Market Position

NCLH operates in a highly concentrated industry alongside two major publicly listed competitors – Carnival Corporation (CCL) and Royal Caribbean Group (RCL) – which together account for the majority of global cruise brand shares.

Scale and Cost Advantages: As one of the largest cruise companies, NCLH benefits from economies of scale in procurement (food, fuel, supplies) and overhead. Carnival Corporation, with ~90+ ships, is the largest player, followed by Royal Caribbean (~64 ships including its Silversea and Celebrity fleets), then NCLH (~30 ships). Though NCLH is smallest of the “big three,” it is still orders of magnitude larger than any independent cruise lines (most of which operate only a handful of ships). The big three collectively can negotiate favorable terms with suppliers, secure priority berthing at ports, and spread fixed costs like marketing and technology across a large fleet. This scale advantage makes it hard for smaller lines to match the cost efficiency and global reach of NCLH and its peers. For example, NCLH’s record $2.45 billion Adjusted EBITDA in 2024, suggests significant operating leverage in its model. The company’s Adjusted Cruise Cost per capacity day increased only ~1% in 2024 (excluding fuel and dry-dock), underscoring cost containment that comes with scale.

Unique Assets: Cruise lines also cultivate moats via unique offerings that are hard to copy. NCLH has private island destinations (Great Stirrup Cay in the Bahamas and Harvest Caye in Belize) accessible only to its guests, enhancing the value of a Norwegian Cruise Line itinerary. The planned new multi-ship pier at Great Stirrup Cay will further increase guest throughput and experience on that island. Competitors have similar setups (e.g. Royal Caribbean’s CocoCay), but these exclusive destinations act as a differentiator from land-based vacations. Moreover, NCLH’s upcoming ships with new attractions.

Investment Thesis

Fleet Renewal & Capacity Growth Underpinning Revenue Expansion: NCLH is embarking on a fleet expansion program that will fuel growth for years to come. It has thirteen new state-of-the-art ships scheduled for delivery 2025 through 2036, representing roughly a ~41,000 increase in berth capacity. Importantly, these newbuilds are larger and more efficient on average, and targeted to high-demand market niches. For example, Norwegian Cruise Line’s Prima-class and next-generation ships (coming 2025–2027) each carry ~3,500–3,850 passengers and boast new entertainment features, likely commanding premium pricing. Oceania’s two new Allura-class ships (2023’s Vista and 2025’s Allura) refresh its premium offering, and Regent’s upcoming Seven Seas Grandeur (2023 delivered) and Seven Seas Prestige (2026) expand capacity in luxury, where demand often exceeds supply. Overall, capacity is set to grow ~6% CAGR through 2028 and 4% CAGR through 2036. Moreover, newer ships generate higher margins (with more balcony cabins, efficient engines, and attract newer cruisers with higher onboard spending). NCLH is also investing in guest experience upgrades, such as the new port facilities at its private island, which will support greater guest volumes and satisfaction. The fleet renewal not only drives top-line growth but also allows the retirement or sale of older, less efficient ships (if any remain from pre-2000 builds), further improving the cost profile over time. In summary, NCLH’s pipeline of new ships provides a tangible engine for growth over the next five years.

Strong Industry Tailwinds: Secular trends support cruising: an aging population (more retirees with time to cruise), increasing penetration of cruising among younger travelers, and growth of the middle class in emerging markets all point to a larger addressable market. After years of pandemic disruption, consumers are prioritizing experiences and travel, a trend which should persist. Importantly, the supply side is relatively constrained – the global cruise fleet is growing at a modest pace and some older tonnage has been scrapped, preventing over-capacity. With this environment of high demand and controlled supply has led to pricing power across the industry. Such broad-based strength suggests a rising tide lifting all operators. NCLH, with its focus on higher-end cruising, stands to particularly benefit as upscale travel demand remains robust (wealthier consumers are less affected by inflation or economic slowdowns). Additionally, cruising remains a value proposition relative to land vacations – as land resorts/hotels have raised prices, cruises offer an all-inclusive experience often at lower cost, attracting new customers. With the industry on track for record revenues and profits, NCLH will benefit from these macro tailwinds.

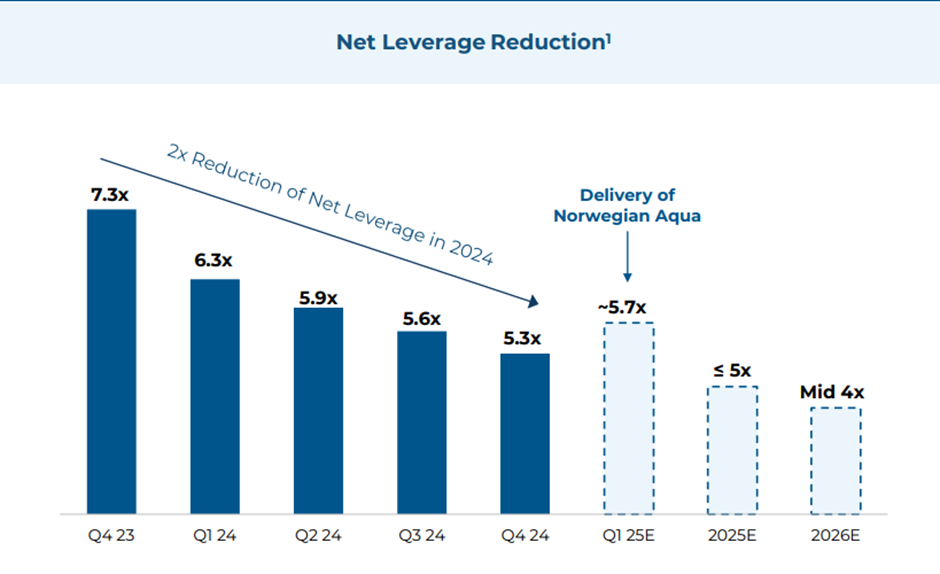

Deleveraging and Financial De-Risking: NCLH’s heavy debt burden from the COVID period has been a overhang, but the company is now in a position to aggressively pay down debt and reduce risk. In 2024, NCLH used its cash flow to cut net leverage from 7.3× to 5.3× EBITDA. Absolute net debt fell by roughly $750 million in the year to $12.91B. Looking ahead, management expects net leverage to fall to ~5× by end of 2025 and mid-4× by 2026, driven by EBITDA growth and scheduled debt amortization. Each turn of leverage reduction meaningfully lowers interest expense (currently ~$700M for FY25), freeing up more earnings for equity holders. For 2025 and 2026, newbuild capex is largely financed via export credit facilities (covering ~$1.5B of ~$2.4–2.5B annual newbuild spend) , keeping net capex around $1B per year which the operating cash flows can support as FY24 & FY23 had ~$2B in OCF . As the balance sheet de-risks, the equity becomes less speculative and more of a normal earnings story, which should attract a broader investor base. There is a credible route for NCLH to materially de-leverage over 5 years, given no further black swan events: strong cash from operations, tapering capex after 2027, and no foreseeable dividends.

Valuation

Currently, Norwegian Cruise Line Holdings Ltd. (NCLH) is trading at $19.89 per share, while the intrinsic value, based on a DCF analysis using a WACC of 10.44% and a growth rate of 3%, is estimated to be $36.70 per share. This suggests a substantial upside potential of approximately 84.5%. The difference between the current market price and the intrinsic value reflects NCLH’s growth prospects, driven by the company's recovery from the pandemic, expansion of its fleet, and improvements in profitability. As NCLH executes its strategic initiatives and reduces leverage, the stock is likely to approach its intrinsic value. The stock presents an attractive opportunity for investors, offering significant upside potential as the company strengthens its financial position and the industry continues its recovery.

Risks and Mitigation

R1 - Macroeconomic and Demand Risk: Cruises are a discretionary luxury purchase, and a global economic downturn or recession could soften demand. If consumers cut back on travel spending, NCLH could face lower bookings or need to discount fares, hurting yields. So far, demand has remained resilient – management noted no detectable change in booking behavior despite economic “noise” in early 2025.

M1 - Mitigation: NCLH can flexibly adjust itineraries and marketing to stimulate demand (for example, shorter, more affordable cruises during downturns). The staggered deployment of new capacity also allows scaling growth to demand – ships can be redeployed to stronger markets if needed. Additionally, a significant portion of bookings are from a relatively affluent customer base (especially for Regent and Oceania), which would be insulated in a mild recession. NCLH also holds substantial advance deposit liabilities (customers pre-paying), which provides a cushion of booked business. In a severe scenario, NCLH could use promotions or value-add offers (rather than pure price cuts) to maintain volume.

R2 - Fuel Cost and Commodity Risk: Fuel price volatility can quickly impact operating costs and margins. A sharp rise in oil prices (due to geopolitical events or supply cuts) would increase NCLH’s fuel expense, given the company expects to consume nearly 1 million tons of fuel in 2025.

M2 - Mitigation: NCLH’s fuel hedging program is a direct mitigating action – with over half of 2025 consumption hedged, the company has partial protection in the near term. It has also hedged a portion of 2026 needs. Longer term, new ships are more fuel-efficient (reducing per-unit fuel burn), and the company can implement energy-saving practices (optimized routing). In the event of a fuel spike, cruise lines have shown ability to introduce fuel surcharges or adjust itineraries to manage costs.

ESG

Environmental (E)

Cruise ships have a significant environmental impact, and NCLH, like its peers, faces scrutiny to minimize its footprint. Key points in NCLH’s environmental performance:

Carbon Emissions: As NCLH is in the cruise industry, I expect high greenhouse gas (GHG) emissions from its fleet. However, the company has set clear targets to address this: a 10% reduction in GHG emission intensity by 2026 (versus 2019) and a long-term ambition of net zero by 2050. To achieve these, NCLH is investing in emissions reduction technology – for instance, exploring alternative fuels (the 2027 newbuilds are designed to be “green methanol-ready” which can significantly cut carbon if that fuel becomes available at scale. NCLH also deploys energy-saving initiatives like itinerary optimization

Waste and Oceans: Environmental stewardship extends to waste management. Cruise ships produce large volumes of waste water (grey water, black water) and solid waste (food waste, plastics). NCLH’s vessels are equipped with Advanced Wastewater Purification Systems that treat sewage to near-drinking-water standards before discharge, exceeding many regulatory requirements. The company adheres to MARPOL regulations for waste and has a zero discharge policy in protected areas. NCLH has pledged to eliminate certain single-use plastics and in fact was the first major cruise company to be single-use water bottle-free.

Social (S)

Social factors cover NCLH’s treatment of its workforce, guests, and the communities it touches:

Employee Well-being and Diversity: NCLH’s 41,000 employees hail from over 120 countries, making diversity and inclusion inherent in its operations. The company prides itself on a multicultural workforce and has diversity in corporate leadership as well.

Community Engagement: NCLH contributes economically to communities by bringing tourists who spend money locally. But it also gives back: through its “Hope Starts Here” hurricane relief campaign, NCLH raised millions for rebuilding Caribbean islands hit by storms. The company has a partnership with the Alaska Native-owned Huna Totem Corporation for developing a new cruise pier in Alaska, ensuring locals benefit from cruise tourism. Additionally, the Norwegian Cruise Line Holdings Charitable Foundation supports education and disaster relief in various regions.

Governance (G)

NCLH’s governance structure and practices ensure that the company is directed and controlled in the interests of shareholders and stakeholders:

Executive Compensation and Alignment: Executive pay at NCLH is tied to performance metrics. The 2024 compensation plan, for instance, included targets for Adjusted EBITDA, Net Yield, and individual strategic goals. In 2020, management took pay cuts and eliminated bonuses as the company was in crisis – showing a willingness to share pain. Conversely, retaining talent was arguably critical. Going forward, I expect compensation to normalize with a strong pay-for-performance orientation. The new CEO Harry Sommer’s pay package is public and includes stock-based awards that vest over multiple years, aligning him with long-term stock performance.

Transparency and Shareholder Communication: NCLH provides detailed financial disclosures and holds regular investor calls. It also has been transparent about its “Charting the Course” three-year plan, publishing specific financial targets for 2026.

Risk Management: The tumult of 2020–2021 tested NCLH’s risk management – they managed to avoid bankruptcy through timely capital raises.