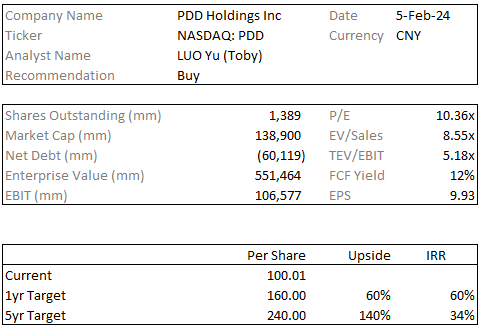

Initial Report: PDD Inc. (NASDAQ:PDD), 140% 5-yr Potential Return (Yu (Toby) LUO, VIP CC)

Toby presented a "BUY" recommendation based on its quality upgrades, strong subsidy program, supply chain advantage, growth potential, and effective management.

stock analysis")

LinkedIn: Yu (Toby) Luo

Overview

PDD Inc. (Pinduoduo) is the third largest Chinese e-commerce platform and currently traded at a $100bn market cap. Founded in 2015, PDD takes market share from Alibaba and JD.com through its low-pricing strategy and astonishing customer acquisition tactics. It consists of three businesses: the Pinduoduo main app, the grocery pickup service Duoduo Grocery, and the overseas retail platform TEMU.

Recommend LONG, TP at $130 (+90% upside to Dec-2025) based on 15x P/E multiple in 2025 (premium to peers) and 11.5bn RMB net profit in FY25.

Thesis: PDD’s main app is able to achieve a 4.7tn GMV in 2025 (60% of BABA) and increase its take rate to 5% (same as BABA), making its current trading price (18x of PE-TTM) attractive. PDD’s share price has dropped 66% from its peak ($212 per share in 1Q21). Besides the deteriorating US-China relation, the market concern that PDD cannot maintain a high earning growth due to 1) PDD encourages merchants to sell cheap but low-quality products so it cannot increase GMV by selling more brand products; and 2) the Chinese e-commerce penetration rate has peaked so PDD’s monetization is hard to increase. However, we believe those concerns are untenable due to the following reasons:

PDD is letting customers be aware that they sell products with good quality. First, the goods return mechanism enables customers to return bad-quality goods with no reason and merchants will be fined. Second, PDD is using the “ten billion subsidies” strategy to attract brand products to sell on platform at a discounted price.

PDD’s low-price advantage is not likely to be threatened by Taobao and JD. PDD is able to sell products in all categories at a low price for a durable time. This reflects PDD’s advantage in supply chain and operations management, as PDD deeply cooperates with OEMs and gives them more exposure. While Taobao and JD’s low-price strategies are hindered by Tmall and JD’s 1P business.

PDD can further grow revenue by increasing ARPU and take rate. PDD’s ARPU was only 2,810 Yuan per user in 2021, which is significantly lower than JD (5,785 Yuan) and Ali (9.240 Yuan). And its overall take rate is only about 4% in 2022, while Ali as a matured 3P platform discloses a take rate of about 5%. Considering PDD’s customer base is as large as Ali, it’s reasonable to expect PDD to raise its ARPU and take-rate in the next several years.

Catalysts: quarterly results beat market consensus; new business expansion faster than expected

Risks: US-China relations worsen; overseas regulation tightened for TEMU; market competition become fiercer than expected

Financials and Key Metrics

Stock performance:

Background

History: PDD was founded in 2015 by Mr. Colin Zheng Huang, a formal Google employee and successful serial entrepreneur. Before establishing PDD, Colin founded and ran several successful businesses including e-commerce agency operator Leqi, overseas DTC platform Lebei and gaming developer Xunmeng Games. In the early period, PDD stepped into the blue-sea market by connecting vast consumers in rural area with numerous OEMs abandoned by Taobao and JD. Colin, with rich experience in the e-commerce and gaming industry, realized consumers want cheap products and have fun in buying, so he developed various customer acquisition strategies including “group purchasing” and retweeting buying messages to friends to gain discounts. Those virus marketing tactics made PDD’s customer base increase by 200% CAGR and GMV increase by 103% CAGR from 2017-21, growing to become the 3rd largest e-commerce platform in China. With initial success in Chinese e-commerce market, PDD further expands to community grocery pickup with Duoduo Grocery in 2021 and started international expansion with TEMU in Jun-2022.

Investment Thesis

PDD is “upgrading” its good sold by punishing bad merchants and continuing ten billion subsidies

Though PDD have being long dismissed for selling cheap but low-quality products, it is currently “upgrading” its goods by adopting stricter quality standards and introducing brand products with ten billion subsidies. In the 1Q23 earning call, PDD announced it changed its slogan from “more discounts, more fun” to “more discounts, better service”. According to interviews with PDD customers and sellers, if customers receive bad products, they can return the goods within seven days for no reason and receive a full refund. Also, the platform adopts a new quality standard in early 2022 where the merchant will be fined as high as 300% of sales volume*selling price. Although PDD’s recommendation algorithm prefers low-price products in the same category, the punishment system ensures both cheap and acceptable quality of the best sellers.

Apart from raising quality standards, PDD continues the “ten billion subsidies” launched in 2019 to raise the sales volume of brand products. PDD provides subsidies for brands like Apple to let them sell at a discount. According to sell-side estimates, 3C digital products sold on PDD have an average 15% discount compared with the original price, while JD has a 9% discount and Tmall has no discount. The “ten billion subsidies” allow consumers to buy high-quality brand products at a fair price and serve as consumption upgrade. The GMV of brand products comprised 33% of total GMV in 2022, compared with 10% in 2016.

PDD’s low price advantage is backed by supply chain advantage and is unlikely to be threatened by TB and JD’s low-price strategy

In Mar-23, JD announced its own version of the “ten billion subsidies” and decided to adopt the “low-price strategy in every category”, while Ali’s new president Joseph Tsai also declared that Ali would re-focus on Taobao instead of higher-end Tmall. However, we believe that competitor low price strategy won’t threaten PDD’s pricing advantage. First, PDD has deeply cooperated with OEMs of industry goods and farmers to strengthen its supply chain. Specialists would give them advice on high-efficiency production to lower production and logistics costs. Besides, PDD’s recommendation algorithm gives more exposure to merchants with lower prices, while Taobao and JD’s algorithms give more exposure to merchants pay higher advertising bidding fees. Therefore, merchants with highest selling volume on PDD have higher price advantage.

Second, Ali and JD’s low-price strategies are hindered by interest parties within the group. For example, JD have spent much resource and capital in its 1P business to maintain a “good and fast” shopping experience. Lowering selling price would harm 1P business’ profit and would receive huge rejections from the department. Meanwhile, Ali has long relied on Tmall as its main revenue source. Re-focus on Taobao would lead to fewer active buyers on Tmall and therefore may lead to negative earning growth in the short-to-medium term.

PDD can maintain higher-than-average revenue growth by increasing ARPU and take rate

Some investors question whether its earning can further grow as China’s e-commerce penetration rate has peaked. They underestimate PDD’s ability to increase revenue and profit by increasing its ARPU and take rate. PDD’s ARPU was only 2,810 Yuan per user in 2021, which is significantly lower than JD (5,785 Yuan) and Ali (9,240 Yuan). And its main app overall take rate is less than 4% in 2021, while Ali as a matured 3P platform discloses a take rate of over 5%. Considering PDD’s customer base is as large as Ali, it’s reasonable to expect PDD to raise its ARPU and take-rate in the next several years.

PDD’s meritocratic management team with strong execution power is a plus

Zheng Huang was vigilant that PDD may become as bureaucratic and low-efficiencies as Alibaba in the long run. Before his retirement, he made a speech to all employees, suggesting the company should “blow up the top of the pyramid”, which means all the managers should be promoted based on business performance rather than other factors like relationship with the founder. PDD’s current management team have been long-term business partners with Zheng Huang. They share the same value and have already proved themselves through early achievements. Current CEO Lei Chen, in charge of R&D and overseas expansion, is a renowned programming specialist and built up PDD’s recommendation algorithm from scrap. And the newly promoted Co-CEO Jiazhen Zhao, who focuses on the main app’s governance, is a veteran in the supply chain department and led the Duoduo Grocery project when first launched.

Furthermore, the management team has strong execution power and adopts different strategies depending on cases, as is shown in Duoduo Grocery. When the project was launched, PDD selected 13 in-line managers for different regions nationwide. The announcement was made in the morning and some managers cancelled their house leased near the headquarter and directly flew to the governed region in the late afternoon. PDD was famous for strict obedience to orders, but the headquarter allowed each Duoduo Grocery’s in-line manager to freely design strategies according to each region’s characteristics. That was one of the key reason that Duoduo Grocery outperforms other rivals like Taocaicai and Jingxi.

Valuation Analysis

Earning forecast: e-commerce platform’s net profit can be calculated using GMV*take rate*net margin. PDD’s main app GMV was 3.5 trillion Yuan in 2022. Given that consumers value cost-to-performance more as economic growth slowdown, we expect PDD’s main app GMV to be 4.5 trillion Yuan in 2025, growing at 10% CAGR in 2022-25 and outperforms the average. Assuming the main app take rate increases to 5% as previously discussed, it implies revenue in 2025 to be 220bn Yuan. PDD’s main app remains a 40% net margin after 2021 due to less marketing expense and we expect the net margin to maintain, this means a net profit of 90bn Yuan. For new businesses like Duoduo Grocery and TEMU, the competition is fiercer and more unpredictable, and I conservatively expect they achieve break-even in 2025.

Valuation: E-commerce business doesn’t require high CAPEX and has a relatively high profit margin so I think the industry worths a P/E of 12 in the long run. Since PDD has higher growth potential and better management than BABA and JD, I give it a valuation premium of 15 P/E in 2025. This implies a 19bn dollar market cap which is a 90% upside in less than three years, yielding an annual return of 30%.

Risks and Mitigants

Risk 1: US-China relations worsen may result in PDD being delisted. PDD has not dual-listed in HKEX, so it faces a higher risk of being delisted from the public market. However, the Chinese gov’t has allowed PCAOB to inspect audit reports of Chinese companies listed in the US, and PCAOB agrees to take routine inspections. This progress reduced the risk of PDD being delisted.

Risk 2: Overseas regulation tightened for TEMU. The market concerns that TEMU will face greater regulatory pressure in overseas markets (like TikTok in 2021) and PDD may be forced to sell this promising business. But PDD has already taken caution and is transferring TEMU to be a US-based company not affiliated with Chinese entities.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.