Initial Report: S&P Global Inc. (NYSE: SPGI), 116.9% 5-yr Potential Upside (Wei Jing SIM, SC VIP)

Wei Jing SIM presents a "BUY" recommendation based on S&P Global's stable subscription-based segments and expanding margins, Generative AI integration opportunities and forecasted macro tailwinds.

1. Company Overview

SPGI is a prominent provider of financial intelligence and analytics to global capital, commodity, and automotive markets. The company's comprehensive suite of offerings encompasses credit ratings, benchmarks, analytics, and workflow solutions, which are integral to clients' operational processes across various industries.

SPGI has 5 key divisions:

This diversified business model, coupled with the company's entrenched market position and continuous innovation initiatives, positions S&P Global as a key player in the financial information services sector, serving a broad spectrum of global market participants.

2. Industry Overview

In terms of indices, SPGI stands out amongst competitors as one of the most recognisable companies in the entire world. SPGI is often known for its widely invested S&P 500 Index, alongside its Dow Jones Index. This presents its Indices segment with a strong economic moat, distinguishing itself from competitors through pure brand image as a benchmark for the US economy.

Source: SeekingAlpha

Moreover, in terms of financial data analytics, SPGI is also amongst the top players. Its widely used S&P Capital IQ is a staple amongst financial institutions. As such, it also has competitors like FactSet and Moody's Analytics. Moody's also competes with SPGI as a credit rating company.

3. Investment Thesis

3.1 Subscription-based segments give consistent cash flow, while market-dependent Ratings segment is projected to grow due to maturing debts peaking in 2028. Further, IHS acquisition synergies expected to reduce expenses.

SPGI's market leadership and diversified revenue streams mitigate risks from economic uncertainty while enabling steady growth across business cycles, providing consistent cash flows, whilst maintaining room to take advantage of market booms through market-dependent segments.

Source: SPGI Annual Report, FY24

To explain further, the Ratings segment is poised to benefit from increasing debt maturities through 2028, as a market dependent segment. (“Market dependent”: For example, if there’s more bond issuance, the Ratings segment will increase. The higher the AUM for the S&P500, the more revenue the Indices segment will generate.)

“We continue to expect favourable market conditions around stable rates and credit spreads, and we are encouraged by the robust maturity walls over the next few years, all of which inspires confidence that issuance will see positive growth in 2025. Our outlook for the Ratings division assumes the refinancing of 2025 maturities and modest pull forward from the 2026 and later maturities. We also expect some improvement in the M&A environment relative to the last couple of years, and there should be some tailwinds to issuance as a result.”

~ Martina Cheung, President & CEO, Q4 Earnings Call

This refinancing wave presents a favorable opportunity for credit rating agencies like SPGI. As companies issue new debt to replace maturing obligations, they will require credit ratings for these instruments. SPGI's ratings segment is a high-margin business that stands to benefit from increased issuance volumes driven by the maturity wall. Peaks in refinancing activity expected in 2028 align with SPGI's business model, which thrives on demand for ratings during periods of heightened debt issuance.

Source: Charles Schwab, 2024

Note: 2025 revenue guided to grow by 3%-5% amidst improving issuance volumes. However, in my model, I did not follow management’s guidance, as they were historically conservative in earnings calls, projecting high single-digit growth rates for each segment, despite easily having high-teens growth rates in actual figures, and beating earnings expectations.

Furthermore, synergies with IHS Markit are shining through, with both revenue and cost synergies delivering as expected. SPGI expected to deliver annual cost synergies of about $600 million, with approximately 80% of those expected in FY2023, and approximately $350 million in annual revenue synergies for an expected total run-rate EBITA impact of ~$810 million in 2026. As such, I have maintained stable cost projections in my model, with 0.5% y-o-y decreases to simulate cost synergies.

3.2 Generative AI Integration can improve customer experience, while ESG Leadership takes advantage of growing demand in European markets.

Leadership in ESG

“More importantly, there’s a shift from scores to data analytics, we have information about what’s called physical risk – buildings, ports, airports, how much carbon do they emit, what is their risk related to flooding, or to fire, or to climate change.”

~ Douglas L. Peterson, Former CEO, 2024 Barron's interview

However, there has been pushback from the US, particularly in the current Trump administration with the removal of many sustainability initiatives (including the Paris Climate Agreement). The good news is that many US companies are still publishing sustainability reports, ensuring that the value of S&P Global’s ESG data won’t go away.

Furthermore, Europe has also seen constant resilience in the sustainability initiative. Thus, S&P Global’s diversified revenue segments ensures stability. This leadership in sustainable finance data analytics can attract ESG-focused investors while expanding SPGI's total addressable market.

AI as an opportunity

“In the past it was numbers that were digitised, and you were able to start using information tools like traditional machine learning AI to gather information from your numbers. But the generative AI is allowing you to use large data sets that the artificial intelligence, or LLMs, as they call them…It means that we can use our data with generative AI models and provide faster, even more well-informed answers to our customers.”

~ Douglas L. Peterson, Former CEO, 2024 Barron's interview

SPGI also recently taken it a step further, acquiring ProntoNLP in Jan 2025, further boosting its Generative AI capacities. Thus, SPGI’s leverage as a data analytics company will bring about value for its customers.

For leadership, SPGI’s AI capabilities are in the hands of Chief AI Officer, Bhavesh Datalji. Bhavesh has been amongst the chief executives of Kensho Technologies Inc. ever since July 2014 (Source: LinkedIn, 2025). For context, Kensho was previously acquired by SPGI in 2018, and thus Bhavesh brings in a tremendous amount of experience in AI, facilitating new initiatives to improve SPGI’s AI offerings.

Therefore, AI-driven products like ChatIQ for Capital IQ Pro and Chat AI for Platts enhance client analytics capabilities, boosting customer retention rates and premium pricing potential.

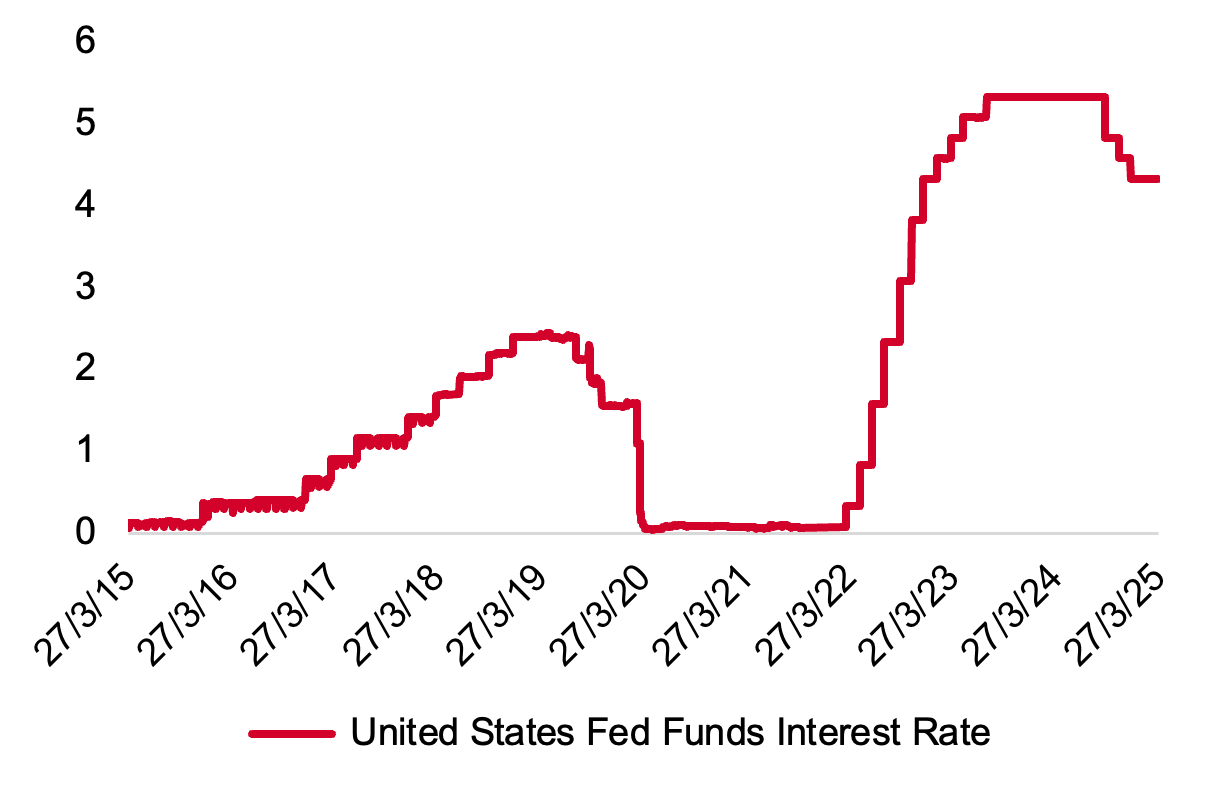

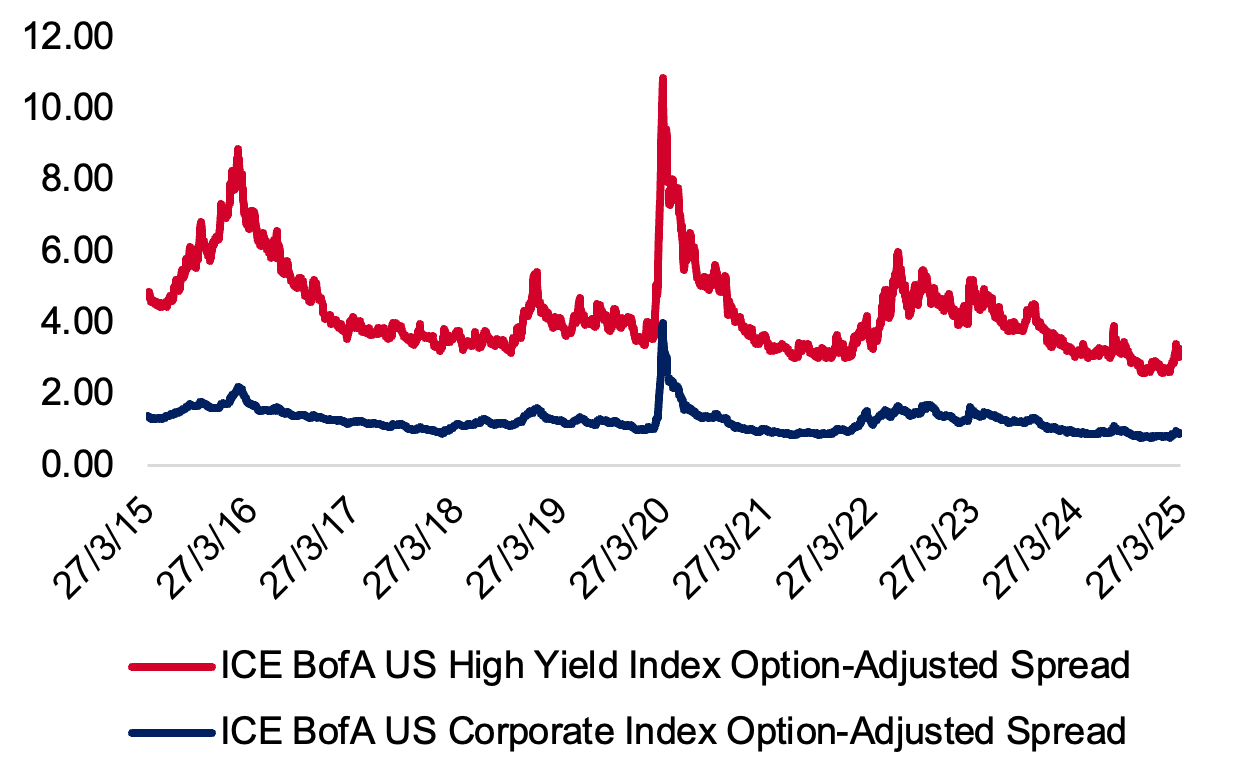

3.3 Constant watch on Fed rate cuts and global interest rates may boost corporate lending. All-time lows for high-yield credit spreads and low-yield credit spreads.

Goldman Sachs has also recently updated its interest rate projections, forecasting additional rate cuts in July, September, and November. Concurrently, economic challenges, such as the impact of tariffs introduced during the Trump administration, are expected to dampen economic growth and contribute to rising unemployment. These conditions may create favorable opportunities for SPGI, particularly within its Ratings segment, as the economy faces headwinds.

This is despite the recent March meetings, in which rates were held steady. Jerome Powell mentioned: “If the economy remains strong, and inflation does not continue to move sustainably toward 2%, we can maintain policy restraint for longer,” he said. “If the labor market were to weaken unexpectedly, or inflation were to fall more quickly than anticipated, we can ease policy accordingly.”. However, given the current economic outlook, it is likely cuts are coming soon.

As interest rates are projected to decline in the coming years, bond issuance is anticipated to increase. This trend is further supported by historically low high-yield and investment-grade credit spreads, which reflect reduced borrowing costs and improved market conditions for corporate lending. SPGI's Ratings segment stands to benefit from this environment, driven by heightened demand for credit ratings amidst increased corporate bond market activity. As such, we will need to keep a close eye on the Fed's rates, as well as Trump's tariffs.

Source: MacroTrends, 2025

Source: FRED, 2025

4. Valuation

The stock was initially priced at $494.27 as of 18 March 2025.

When analysing 3-year historical EV/EBIT multiples, SPGI hovers at a mean of 31.28x, with a high of 36.72x and low of 25.34x. I further analysed a TTM EV/EBIT multiple, which gave me an average of 31.54x. Here I see an opportunity to invest, as multiples signal a decrease, with an average of 22.20x forward EV/EBIT.

Therefore, I assumed a conservative ratio of 30.00x for my first year projections, which gave me a 17.2% upside in my first year. I then assumed a 31.00x multiple for my second year, aligning closely with historical EV/EBIT figures, which gave an upside of 45.3%. Lastly, I assumed a 32.00x multiple for my final third year’s projections, which gave me an upside of 79.3% over a 3-year time horizon. I finally assumed a constant 31x EV/EBIT ratio, whilst EBIT steadily increased with tapered down YoY growth rates for revenue segments, arriving at a 5-year price of $1072.20, with a 116.9% upside.

5. Risks and Mitigations

5.1 Current Trump administration presents economic uncertainty

Tariff escalations or trade conflicts could reduce corporate expansion, M&A activity, and deal-related revenue for SPGI. Protectionist policies may slow global GDP growth, indirectly affecting SPGI’s Market Intelligence & Commodity Insights segments.

However, market volatility may also increase demand for financial risk assessments and data analytics, boosting SPGI’s Market Intelligence subscriptions. SPGI’s global diversification strategy, (not overly reliant on any single economy) hedges against U.S. trade disruptions.

5.2 Competition in AI & Market Intelligence

Financial institutions are investing in in-house AI-driven analytics, which could reduce reliance on third-party providers like SPGI. Competitors like Bloomberg, Moody’s, and MSCI may capture market share in financial data & ESG analytics.

However, as previously mentioned in the thesis, SPGI is aggressively investing in AI & automation (e.g., ChatIQ, Platts AI, Doc Intelligence) to maintain its competitive edge.

6. Conclusion

There was a quote in the early 2000’s by mathematician Clive Humby, stating “data is the new gold”. In my opinios, this quote is applicable more than ever in today’s economy, with the persistent rise of AI and prevalence of data analytics.

Thus, I believe that despite SPGI’s current price of $494.27, it is still a strong buy given its current trading multiples relative to both peers and historical averages. SPGI’s strong market position, combined with consistent subscription-based revenue streams, and growing market-dependent segments, proves to be a good business to buy into. Lastly, SPGI is globally diversified, and is widely used in the finance industry to extract data. Their “Powering Global Markets” vision presents a compelling story on providing institutions and investors with data needed by everyone. After all, it is likely that you have used and will continue to use Capital IQ throughout your finance careers! I know I definitely did!

7. Appendix

SPGI Annual Reports:

https://investor.spglobal.com/sec-filings-reports/10-qs-10-ks-other-filings/

Charles Schwab Bonds Report:

https://www.schwab.com/learn/story/will-maturity-wall-matter-investors

Barron's Interview:

ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2):

https://fred.stlouisfed.org/series/BAMLH0A0HYM2

ICE BofA US Corporate Index Option-Adjusted Spread (BAMLC0A0CM):

https://fred.stlouisfed.org/series/BAMLC0A0CM

United States Fed Funds Interest Rate:

https://www.macrotrends.net/2015/fed-funds-rate-historical-chart

FY24 Q4 Earnings Call Transcript:

https://www.fool.com/earnings/call-transcripts/2025/02/11/sp-global-spgi-q4-2024-earnings-call-transcript/

FY23 Q4 Earnings Call Transcript:

https://www.fool.com/earnings/call-transcripts/2025/02/11/sp-global-spgi-q4-2024-earnings-call-transcript/