Initial Report: Ulta Beauty Inc (ULTA) , 9% 5-yr Potential Upside (EIP, Finian SAW)

Finian recommends a “HOLD” on Ulta Beauty Inc as its share price is currently rather high.

1. Company Overview

Ulta Beauty Inc. (Ulta) is the largest American specialty retailer selling makeup, haircare products and tools, skincare, fragrances through its chain of company-owned retail stores, its ecommerce website and shops within Target. In company-owned stores, Ulta provides makeup, salon, nail and brow services to its guests.

Source: Glossy

With over 600 brands including its own private label and 25,000 products, Ulta offers a diversity of products at different price points across categories, from mass market to luxury. Ulta’s wide brand offering is in stark contrast to competitors such as departmental stores and Sephora who are more concentrated in prestige and luxury, and big box retailers who are concentrated in mass market.

Source: Ulta Investor Presentation 2023

Ulta is thus uniquely positioned to cater to its target customers which they have identified as Beauty enthusiasts, guests who are highly engaged in “all things beauty” and thus shop across price points and across categories. Ulta acts as the bridge between the siloed categories of products offered by different retailers, providing them all in one place to disrupt the industry dynamic and deliver their target customer’s desired shopping experience.

Ulta’s loyalty program, Ultamate Rewards, rewards its members with points per dollar spend on Ulta’s offerings across all its channels, including Ulta Beauty at Target. With approximately 95% of total sales being generated from Ultamate Rewards members and having more than 42.2 million active members which is 12.4% of the total US population and more than the entire Canadian population, it is a clear leader in the beauty retailer loyalty programs.

Source: Ulta Investor Presentation 2023

Due to Ulta’s unique and differentiated model, the company has been able to deliver consistently positive store same sales growth and operating margin in the past 5 years, within the range of 8.1% to 37.9% and 12.1%-16.1% respectively, with the exception of FY19-20 where the 4Q19 and the entire FY20 were negatively impacted by the COVID-19 pandemic.

2. Business Segments

Ulta only has one reportable segment, One-Stop Shopping, in its financial statements. As such, it is all encompassing, including product and service revenues from its company-owned retail stores, ecommerce revenue, and royalties from its Target partnership.

Ulta’s revenue segment is further broken down into 6 categories:

1. Cosmetics

2. Haircare products and styling tools

3. Skincare

4. Fragrance and bath

5. Services

6. Accessories and others (includes revenue from credit card programs, loyalty program, gift cards and royalties from the Target partnership)

In terms of geographic segments, Ulta currently operates exclusively in the US. Prior to the COVID-19 pandemic, there were talks of expansion into Canada. However, those plans seem to have been put on hold due to the pandemic.

3. Industry Overview and Growth Trends

Ulta as a beauty specialty retailer, is considered to be in the Consumer Discretionary sector as it offers non-essential products and services. Therefore, Ulta’s business is influenced more significantly by economic cycles and seasonality, with the 4th quarter of fiscal year (Oct-Jan) generating the largest share of revenue due to the quarter coinciding with the holiday season (Christmas, New Years, Valentine’s Day).

Source: Ulta Investor Presentation 2023

In 2022, the market size of the beauty products industry was estimated to be $104 billion in revenue and Ulta holds 9% of market share. As for the salon services industry, it is around $68 billion in revenue and Ulta holds 1% of the market share. Since salon service is not the key revenue category for Ulta, the focus of this section will largely be on the beauty products industry.

The beauty products industry faces intense competition and high fragmentation due to low barriers to entry. Ulta’s competition encompasses a diverse array of retailers, ranging from small to large entities, including regional and national department stores (Macy’s and Kohl’s), specialty retailers (LVMH’s Sephora and Sally Beauty), drug stores (CVS), mass merchandisers (Target, Walmart), locally owned beauty outlets, e-commerce companies (Amazon) and more.

In the North American beauty industry where Ulta operates in, sales growth is projected to grow at a 6% CAGR from 2022 to 2027 and is the 3rd highest in terms of absolute growth at 29.3 billion. Skincare is expected to experience the largest absolute growth in North America, at $10.9 billion, followed by haircare, colour cosmetics and fragrances.

Source: The State of Fashion: Beauty (McKinsey report)

Industry Growth Trend 1: The confluence of the beauty and wellness industries

The beauty industry used to purely focus on traditional aesthetic demands of its consumers, to improve their outward appearances in terms of youthfulness, style and glamour. However, the concept of beauty has grown to include wellness and self-care, to satisfy the increasing demand of consumers to not just look good, but also feel good through the use of beauty products. With the COVID-19 pandemic acting as a catalyst to consumer’s engagement with physical and mental wellness, the worldwide wellness industry is forecast to growth at a CAGR of 5-10% from its current $1.5 trillion, with the largest geographical market being the US at $450 billion in 2022. This presents an immense opportunity for beauty retailers like Ulta to capture consumers’ growing interest towards wellness inspired beauty brands and products in the coming years.

Industry Growth Trend 2: Necessity for strategic omnichannel approach to beauty distribution

Worldwide ecommerce growth in beauty revenue is expected to increase at 12% CAGR from 2022 and 2027, with speciality physical retail increasing at 7% CAGR in the same period. In the US, e-commerce is currently the biggest distribution channel and is forecast to grow to $45 billion by 2027. Despite ecommerce leading sales growth, brick and mortar shops remain as the most preferred channel at 45% compared to ecommerce at 40% according to McKinsey research, likely due to the importance of the sensory experience to consumers when exploring and shopping for beauty products. Hence, it is imperative for beauty retailers such as Ulta to have a sound omnichannel strategy to maximise the sales of both channels.

4. Investment Thesis

1. Ulta’s forward looking execution of its unique selling proposition being the retailer that is “All things beauty”, all in one place is key to driving revenue as it enables Ulta to continually connect with its target customer and poises Ulta to capture emerging growth opportunities in the beauty industry.

Ulta is able to continually delight its customers through their ever-growing pipeline of brand partners, with both established and up and coming brands, through their rigorous brand exploration and effective brand cultivation process. Ulta’s team evaluates 2000-3000 brands annually for great brand propositions and only less than 5% are launched in Ulta’s channels. Of those selected brands, Ulta places great emphasis on how it will take those brands to market, tell brand stories and make an impactful launch. This is particularly prized by independent, early-stage brands who see Ulta as a place of growth. MUSE Accelerator and SPARKED are two Ulta initiatives whereby BIPOC and digital native beauty brands respectively are provided training and mentorship from industry professionals to gear up them up for success in an omni-channel retail environment and make their first launch at a major retailer. These platforms provide a win-win situation; brands are nurtured for enduring success while Ulta is able to constantly inject newness at all price points and across categories with these “hidden-gem” brands, attracting customers to return and explore these new brands. Successful alumni of these initiatives include Pound Cake Beauty by Camille Bell and Half Magic by Donni Davy, head makeup artist for hit show “Euphoria”.

Source: Ulta

With Ulta’s unrivalled brand diversity and partnership strategies, they have been able to ride upon structural trends in the beauty industry such as the growth of wellness in beauty as seen in how more than 25% of Ulta’s brands (>150 brands out of 600) already have wellness offerings, at all price points. With increasing interconnectedness between wellness brands and luxury, Ulta’s steady expansion of its luxury assortment in the past year and its existing stronghold in wellness is poised to compete for market share from luxury focused retailers such as Sephora.

Source: The Beauty Independent

2. Revamped shop format and expansion strategy to drive revenue and lower operating costs.

Ulta currently has 1,374 company owned stores with the goal of having close to 1,700, indicating that approximately 50 stores will open per year up till FY28. Alongside company store expansion, Ulta is also continuing with its Target “Shop-in-shops” partnership where there are mini-Ulta Beauty stores at Target stores (UiT). The function of these UiT stores is not to generate direct revenue for Ulta from the sale of UiT products as Ulta only receives up-front royalty payments from Target which form <3% of Ulta’s revenue. Instead, UiT stores serve as a gateway for Ulta to expand its reach to Target’s customers (almost 8 out of 10 US shoppers are Target customers), to get them to have their first experience with Ulta with a curated assortment, and then entice them to explore full offerings at Ulta stores. This strategy will grow foot traffic for Ulta stores and increase revenue per square foot. For existing Ulta guests, these UiT act as another convenient touchpoint with the Ulta brand. Given that UiT sales quadrupled in 2022 from 2021 figures and that there is an expected opening of around 290 more UiT, up from its existing 510 stores in 3Q23, it is indicative of the success of the partnership in delivering benefits to both Ulta and Target and the rollout over the next few years is expected to continue growing Ulta’s customer base and revenue.

Ulta Beauty at Target (Source: Target Corporation)

Additionally, Ulta has been optimising its store formats for different markets. The trialling of smaller 5,000 sqft formats, down from their regular 10,000 sqft for smaller, remote markets has been successful and will be implemented for new store expansions in such areas. With a lower physical footprint while still being able to deliver the target revenues, Ulta is able to maintain or even grow their revenue per square foot while operating stores at lower cost.

Ulta’s full store layout has also been refreshed to be more “intuitive to shop the whole store”, with product categories bundled together and a larger emphasis on Ulta’s salon services. These improvements translate to greater exposure to the large and ever evolving range of brands and products Ulta Beauty has to offer, and increases the likelihood of additional, cross-category purchases with each trip.

3. Completion of ecommerce overhaul by 1H24 will drive customer spend.

Ulta has been investing a multiyear transformation to upgrade its digital architecture with the goal of achieving a seamless and more engaging omnichannel experience, whereby guests can transition between Ulta’s physical and ecommerce channels with ease. The investment in digitalisation will be a major game-changer in terms of compounding beauty spend per guests as it will further enhance both the online and offline shopping experience, encourage guests to engage in both Ulta’s ecommerce and retail channels. According to Ulta’s analytics, when store-only guests begin shopping on Ulta’s ecommerce channel, their total expenditure jumps 2.5 times and these guests end up making more visits to physical stores, resulting in omnichannel guests spending 3 times more than a retail-only guest. With the upgrading of digital infrastructure expected to be completed by 1H24, Ulta is expected to see a larger proportion of omnichannel guests, which will mean higher revenue per guest.

4. Valuation (Discounted Cash Flow Model)

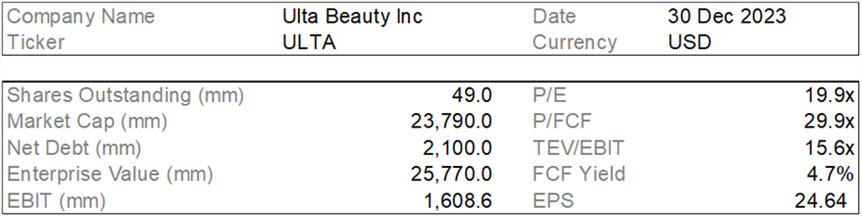

This report utilises the DCF model as its primary valuation methodology. Since Ulta’s management has high confidence in hitting the upper range of 1,500-1,700 of its target store count, assuming that Ulta expands to 1,650 stores by FY28 by opening 49-50 stores per year and that Ulta’s revenue per square footage of stores will grow at a CAGR of 6% between FY24 and FY28 due to its partnership, store expansion and omnichannel distribution strategies, Ulta’s revenue is projected to grow at a CAGR of 8%. Using a WACC of 9% and a terminal growth rate of 3%, the 3-year and 5-year target prices of Ulta are USD$530 (8% upside) and USD$533 (9% upside) respectively, in comparison to the current price of USD$489.99.

5. ESG Assessment

The following are the ESG ratings from 3 different rating agencies, namely Sustainalytics, MSCI and Bloomberg. All three ESG ratings assess Ulta’s exposure to ESG risks and how well Ulta manages risk compared with industry peers. Across the three ratings, Ulta has proven to be a leader in terms of lower exposure to ESG risks and good management of those risks, although do note that each rating’s methodologies and industry universe differ significantly and cannot be directly comparable.

MSCI: AA (Leader)

It is worth noting that MSCI’s ESG rating has steadily increased over the last 5 years from BB to AA. Although the exact rationale to each upgrade is not disclosed publicly for free, it can be inferred that the improvement of Ulta’s rating in the past AA is possibly due to strong management of two key issues material to the retail consumer discretionary industry as identified by MSCI: Corporate behavior (which pertains the management of business ethics, encompassing issues like fraud, executive wrongdoing, corrupt practices, money laundering, and anti-trust violations) and Product Carbon Footprint (which pertains product carbon intensity and reduction of carbon emissions).

Source: MSCI

Sustainalytics

Source: Sustainalytics

According to Sustainalytics, Ulta has low exposure to ESG risk and average management of ESG material risk, aggregating to an overall 15.9 Low Risk Rating (the lower the rating the better). The top material ESG issues identified by Sustainalytics are Corporate Governance, Human Capital, Data Privacy and Security, Operational energy use and greenhouse gas (GHG) emissions.

Bloomberg

Bloomberg gave Ulta an overall ESG Score of 4.45/10, which can be broken down into an environmental, social and governance score of 1.01/10, 6.79/10, 6.83/10 respectively. Only Ulta’s Environmental (E) score was computed to be below median versus industry peers while social and governance are leading, however I find the E score unreliable as it was lower due to the fact that Bloomberg was still in the midst of calculating the impact on certain metrics to the E score, resulting in those metrics not being factored into the E score.

Source: Bloomberg

Analysing Ulta’s ESG report, it is observed that Ulta has extensive disclosures which adhere to two reporting standards, Sustainability Accounting Standards Board (SASB) which focuses on financial materiality of industry specific issues and Task Force on Climate-related Financial Disclosures (TCFD) which provides disclosures that aid in the assessment and pricing of risk related to climate change.

One of the most impressive statistics related to SASB’s required disclosure of discussing strategies to reduce the environmental impact of packaging is that 37% of product packaging sold sold by Ulta is sustainable, meaning that it is either refillable, recyclable or made from bio-sourced or recycled materials. With the goal of 50% of sold product packaging to be sustainable by 2025, Ulta is setting the benchmark for other specialty beauty retailers since such an ambitious goal is not shared by its competitors Sephora or Sally Beauty.

Homing in on one of the top material issues for Ulta, GHG emissions, Ulta has recently announced new near-term climate targets. Ulta is aiming for a 90% reduction in absolute Scope 1 & 2 emissions and a 28% reduction in absolute Scope 3 GHG emissions covering use of sold products 28% by 2030 (from a 2019 base year). Ulta further commits that 68% of its suppliers by emissions covering purchased goods and services will have science-based targets by 2027. These goals are approved as Science Based Targets, which assures their validity. However, while 90% reduction in Scope 1 and 2 seem ambitious, considering that 95% of Ulta Beauty’s emissions are Scope 3 (largely due to purchased goods from brand partners and customer use of products such as aerosol sprays and hair drying tools, which have high emissions), much more progress would need to be made in terms of Scope 3 emissions when net-zero goals are set in the future.

6. Risks and Mitigation

Risk: Failure to accurately identify and respond promptly to emerging beauty trends and shifting consumer preferences

If Ulta is unable to anticipate and adapt to changing beauty trends and consumer preferences, and then translate them into viable product offerings ahead of competitors, there will be significantly negative impact on sales.

A crucial tool to mitigating this risk is Ulta’s loyalty program, Ultamate Rewards. Ulta’s loyalty program is more attractive than its competitors’ due to better loyalty points redemption rates and has resulted in 95% of total sales being made by Ultamate Rewards members and a membership of 42.2 million active members. With a membership pool of approximately 12.4% of the total US population, Ulta's loyalty program is able to collect vast amounts of valuable data on customer preferences, purchase history, and behaviour. By applying predictive analytics to this data, Ulta can gain insights into individual and collective consumer trends, helping the company anticipate and respond to shifts in demand.

The loyalty program also allows Ulta to personalize offers, promotions, and product recommendations for its members based on their preferences and purchase history. This targeted approach ensures that customers are presented with products that align with their tastes, increasing the likelihood of making a purchase.

Risk: Inventory loss (shrink) as a result of organised retail crime (ORC)

Ulta Beauty faces a potential adverse impact on its operating margin if it fails to effectively counter the risk of inventory loss, commonly known as shrink. The retail industry inherently contends with inventory shrinkage due to factors like damage, theft, and other causes. Despite unavoidable levels of shrink, Ulta has experienced higher-than-historical rates of ORC theft and increase in violence during the incidents, negatively affecting its financial standing and operational outcomes. ORC is theft conducted by groups of professionals on a large-scale, who make profits by reselling stolen products on the black market and online distribution websites. According to the US National Retail Federation (NRF), there was a 26.5% spike in ORC in 2023 compared to 2022 among retailers.

To mitigate this risk, Ulta has been collaborating with local law enforcement and other retailers by sharing information on theft patterns and working together to apprehend perpetrators. Ulta has also stepped up employee training and education countrywide and increased the number of store and security staff at various locations. Additionally, by the end of 2023, luxury fragrance products will be kept in locked cabinets in 70% of Ulta’s stores to prevent theft of higher end products.

7. Conclusion

Overall, this report recommends a “HOLD” on Ulta Beauty Inc (NASDAQ: ULTA). Although there is future revenue growth opportunities due to Ulta’s cultivation of diverse brand partnerships to capitalise on industry trends, returns on investment in its ecommerce overhaul and strategic retail expansion, Ulta’s share price is currently rather high. The high price is likely due to the market’s confidence that the management will continue to maintain its lead over industry peers, pricing in Ulta’s strong business model and continuous improvement in management of business risks and ESG issues.

8. References

Sustainalytics. (2023). Company ESG risk rating - Sustainalytics. https://www.sustainalytics.com/esg-rating/ulta-beauty-inc/1007914175

Executives’ Club of Chicago. (2023). The Beauty of Retail A Conversation with Dave Kimbell, CEO, Ulta Beauty. YouTube.

Kohan, S. E. (2023, May 30). Ulta beauty sales grow 12.3% although theft is a serious concern. Forbes. https://www.forbes.com/sites/shelleykohan/2023/05/25/ulta-beauty-sales-grow-123-although-theft-is-a-serious-concern/

McKinsey & Company. (2023, May 22). The Beauty Market in 2023: A special state of fashion report. https://www.mckinsey.com/industries/retail/our-insights/the-beauty-market-in-2023-a-special-state-of-fashion-report

Monteros, M. (2023, March 27). Ulta CEO sees the expansion of beauty category as key growth driver. Modern Retail. https://www.modernretail.co/operations/ulta-ceo-sees-the-expansion-of-beauty-category-as-key-growth-driver/

Mueller, J. (2022, September 20). Ulta Beauty Launches Muse Accelerator Program for BIPOC Brands. Global Cosmetic Industry. https://www.gcimagazine.com/retail/brick-and-mortar/news/22262740/ulta-beauty-launches-muse-accelerator-program-for-bipoc-brands

Rao, P. (2023, October 16). Ulta Beauty’s merchandising chief looks inside a big bet on Wellness. The Business of Fashion. https://www.businessoffashion.com/articles/beauty/the-state-of-fashion-beauty-report-ulta-monica-arnaudo-cmo-interview/

SEC. (2021). Ulta Beauty Announces Long-Term Financial Targets and Strategic Priorities. Sec.gov. https://www.sec.gov/Archives/edgar/data/1403568/000155837021013270/ulta-20211019xex99.htm

Motley Fool Transcribing. (2023, December 1). Ulta Beauty (Ulta) Q3 2023 earnings call transcript. The Motley Fool. https://www.fool.com/earnings/call-transcripts/2023/11/30/ulta-beauty-ulta-q3-2023-earnings-call-transcript/

MSCI. Ulta ESG Rating. MSCI. (2023). https://www.msci.com/our-solutions/esg-investing/esg-ratings-climate-search-tool/issuer/ulta-beauty-inc/IID000000002798249

Ulta. (2023a). 10-Q - 11/30/2023 - Ulta Beauty, Inc. https://www.ulta.com/investor/sec-filings

Ulta. (2023b). Ulta 2022 Annual Report. https://www.ulta.com/investor/sec-filings

Ulta. (2023c). Ulta 2022 ESG Report. https://d1io3yog0oux5.cloudfront.net/_0c2ce48885ef6bc98055835484b8033d/ulta/files/pages/ulta/db/1975/description/ULTA-003_2022_ESG_Report_ADA_110623.pdf

Ulta. (2023d). Ulta Beauty commits to science-based climate targets. https://d1io3yog0oux5.cloudfront.net/_e1dbd01b90665921b9f4d02566ab94b3/ulta/files/pages/ulta/db/1975/description/Approved_SBTi_Goals_Media_Alert_FINAL_11.27.23.pdf

Wassel, B. (2021, October 27). Ulta Beauty Plans 50 store openings per year, AI Investments and Retail Media Network. Retail TouchPoints. https://www.retailtouchpoints.com/topics/store-operations/ulta-beauty-plans-50-store-openings-per-year-ai-investments-and-retail-media-network

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.