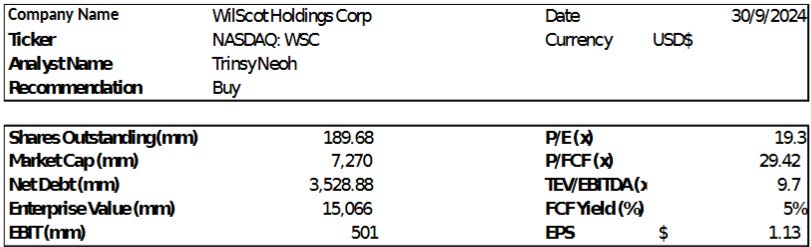

Initial Report: WillScot Holdings Corp (NASDAQ:WSC), 246% 5-yr Potential Upside (EIP, Trinsy NEOH)

Trinsy presented a "BUY" recommendation based on its undervalued stock, driven by strong growth in its Value-Added Products (VAPS) line and robust free cash flow supporting strategic flexibility.

LinkedIn: Trinsy Neoh

Most of us are familiar with Lego blocks—you can stack them to build something and dismantle them when you're done. WillScot Holdings (NASDAQ: WSC) operates similarly but in the context of temporary space solutions. Unlike traditional construction methods, which build structures on-site, the company assembles pre-fabricated sections, or modules, in a factory setting before transporting them to the construction site. Today, WSC is the market leader in North American modular workplace solutions (with ~50% market share) and portable storage solutions (around 25% market share).

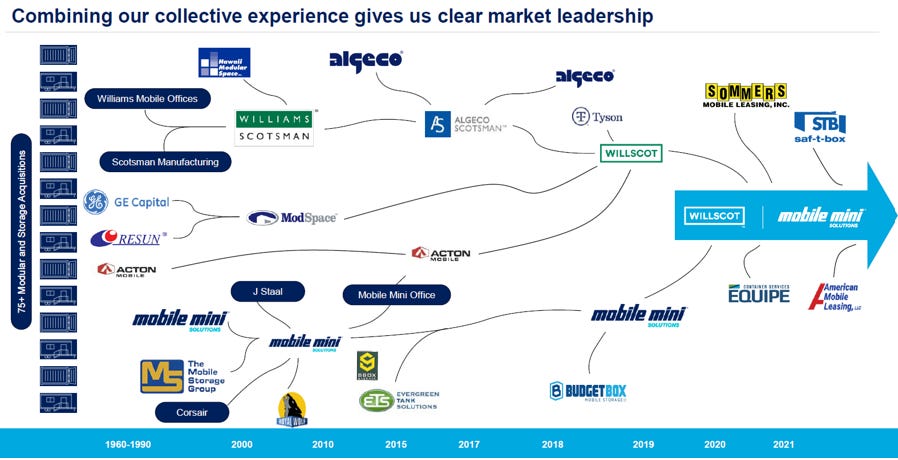

WSC is the result of a merger between two companies, WillScot and Mobile Mini. Prior to their 2020 merger, WillScot Corp was the largest U.S. supplier of mobile office trailers, while Mobile Mini Inc was the leading U.S. provider of portable storage solutions. After the merger, WillScot CEO Brad Soultz became CEO of the combined company, while Kelly Williams, CEO of Mobile Mini, took on the role of president and COO (Kelly left in 2021, as he wished to return to a CEO position).

In terms of management incentives, leadership is rewarded based on metrics such as performance relative to the MidCap 400 Index. Management has implemented an efficient capital allocation framework, with 25% allocated to net capex, 25% to M&A, and 50% returned to shareholders. In November 2021, the company introduced a $1.0 billion repurchase program for its outstanding shares of common stock and equivalents.

Business Model

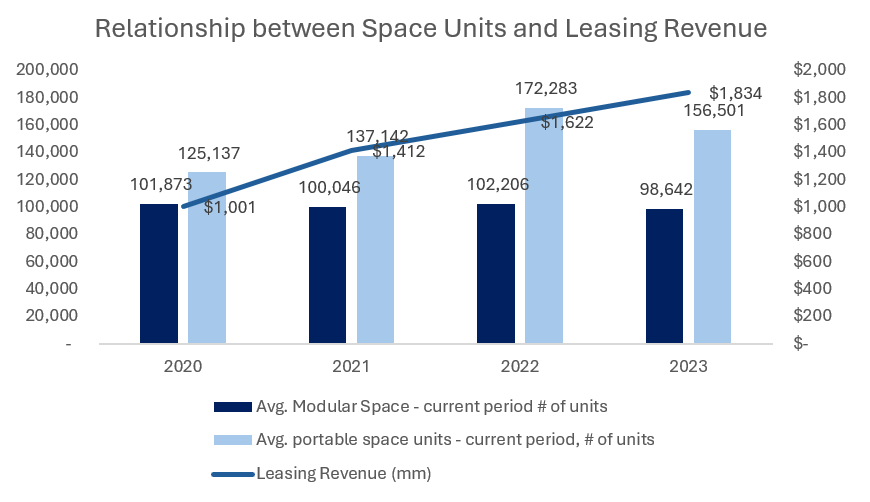

WSC derives its revenue primarily from two segments. First, it generates income from leasing modular space units (including Value-Added Products, or VAPS) and portable storage solutions. The business currently operates 156,000 modular space units and 212,000 portable storage units, representing approximately $3.4 billion and 130 million square feet of relocatable commercial space. These units come equipped with "Ready to Work" solutions, known as VAPS. VAPS refers to items like furniture, steps, ramps, and basic appliances that equip an empty temporary space. Customers pay for VAPS in addition to the monthly rent of the unit. As of December 2023, around 99,000 modular space units and 151,000 portable storage units were on rent.

Second, WSC offers ancillary services, covering delivery, installation, and removal of units. Since the business leases its spaces, WSC’s revenue is generally predictable, with the modular space segment having an average lease duration of 37 months in 2023 and the storage segment averaging 38 months.

Beyond its predictable revenue stream, the unit economics of WSC are attractive. The company employs refurbishment capabilities, allowing it to extend the lifetime of its assets by 20-30 years, cycling through up to seven different customers. Additionally, WSC can extend the asset life by another 10 years through full refurbishment, which costs only 20-30% of the price of a new unit. In contrast, competitors like McGrath can only extend their asset lifetimes by less than 18 years. This lowers WSC's capital expenditures and results in a higher return on invested capital (ROIC) compared to its competitors.

In addition, the business promotes the concept of circularity, which focuses on minimizing waste and maximizing resource efficiency. WSC achieves this by prioritizing refurbishments, leveraging its industry-leading refurbishment capabilities.

WSC Investor Presentation 2021: Illustration of business operation

WSC Investor Presentation 2021: Business offerings

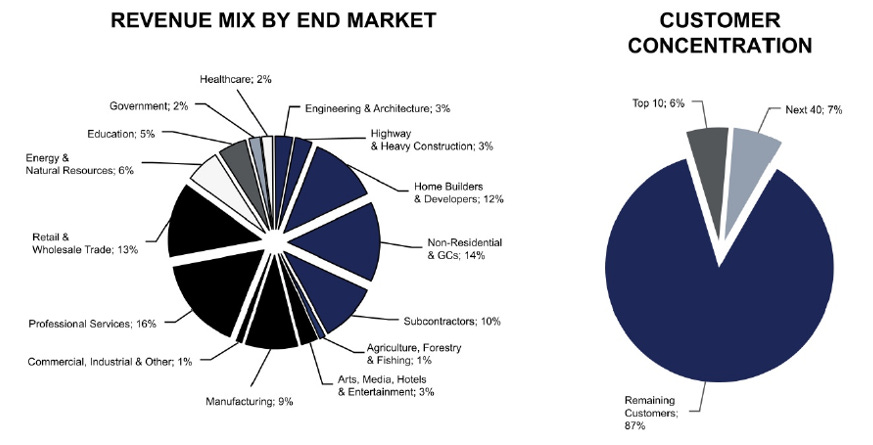

Based on WSC's current customer demographics, the majority of its consumers come from the Commercial sector (44%) and the Construction & Infrastructure sector (42%). Notable examples include supplying modular units for Facebook data centers, providing storage for Target’s remodeling projects, and supporting tour events like the PGA.

Financials

Annualised ROIC

Economic Moat

In the modular space industry, customers prioritize the safety and functionality of the rooms or buildings provided to them. This concern increases their willingness to pay higher prices to offset the perceived risks of uncertainty, which can be more costly than the price of the product itself. Customers would rather pay a premium than face poor quality, delays, or other issues that could significantly impact commercial or construction projects.

Operating in a relatively non-price-sensitive market, WSC has the ability to raise prices without alienating customers. In fact, prices have steadily increased over the past 10 years. When trust is a key factor, customers tend to favor reputable, industry-leading companies. This is evident in WSC’s performance, as revenue has increased even though the number of units sold has declined.

Industry Overview

The modular space and portable storage industry focuses on providing space efficiently and effectively. Key industry tailwinds include the rise in commercial applications, urbanization, infrastructure development, economic growth, and increased institutional use. In the U.S., where urbanization and population growth are driving demand, housing and office space are consistently needed. Modular solutions meet these needs in a fast and scalable way.

WSC competes based on factors such as customer relationships, availability, delivery speed, price, VAPS, and product quality. Its competitors range from lessors of storage units to providers of mobile offices. While WSC is the market leader in North America, the industry remains highly fragmented. Key competitors include McGrath RentCorp, United Rentals, ATCO Structures & Logistics, and Satellite Shelters. Among these, McGrath is WSC's closest competitor, with a fleet size five times smaller. WSC has greater market penetration in the construction and industrial sectors, while McGrath has a stronger presence in the education sector.

Customers are increasingly seeking a one-stop-shop solution rather than dealing with 5-10 different companies to set up a job site. This approach reduces administrative costs and eliminates the inconvenience of coordinating with multiple suppliers.

Over the years, the modular space and portable storage industry has experienced significant consolidation, partly driven by the pandemic, and I expect this trend to continue. In 2018, WSC acquired ModSpace, a privately owned provider of office trailers, portable storage units, and modular buildings. At the time, ModSpace was WSC's largest competitor in the modular space sector. To strengthen its position in the storage space industry, WSC acquired Mobile Mini in 2020, the leading provider of portable storage solutions in the U.S., UK, and Canada. Today, WSC boasts the broadest and deepest network of locations in North America, allowing for more efficient and faster customer deliveries.

Competitors have also been consolidating. In 2021, McGrath RentCorp acquired Design Space, a leading provider of modular buildings and portable storage in the Western U.S. With a network of 15 branches and over 100 employees, Design Space serves diverse end markets, including construction, government, education, and commercial sectors.

There was also speculation about a potential merger between WSC and McGrath, which attracted significant attention from shareholders. However, this has been put on hold due to concerns raised by the FTC regarding potential monopoly issues.

Thesis

WSC is underappreciated by the market. Several factors are driving the company’s growth, making the stock currently undervalued. This includes the growing potential of WSC’s Value-Added Products (VAPS) line and strong free cash flow (FCF) generation.

(1) Single Point of Contact: Value-Added Products (VAPS)

WSC has mastered the single point of contact approach, streamlining the process for customers. Rather than requiring clients to source furniture and appliances separately, WSC offers everything under one invoice, making the space immediately ready for use. As the first company to introduce this concept, WSC has consistently stayed ahead of customer needs. It would be difficult for smaller companies to match WSC's pricing and quality, especially with a fraction of its workforce.

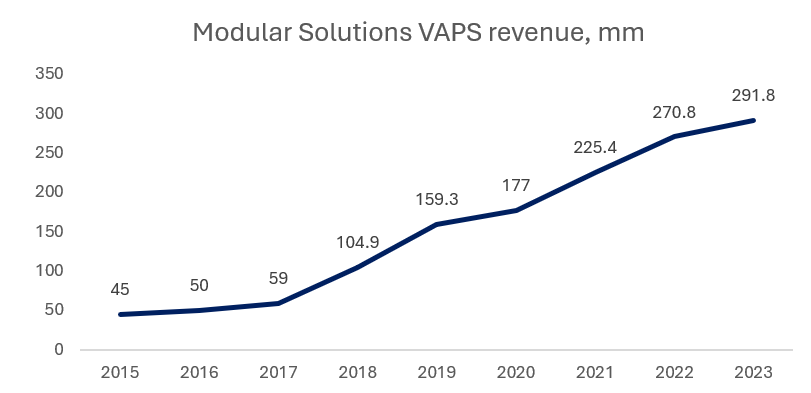

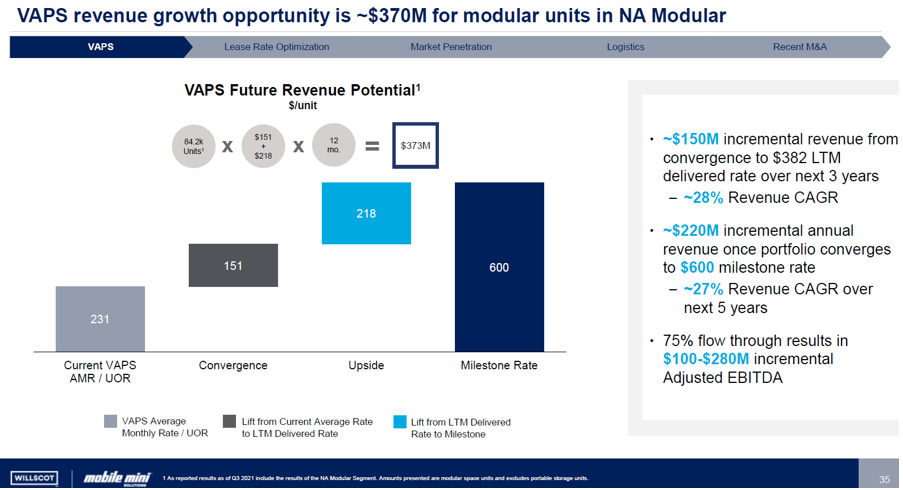

VAPS has been a core focus for WSC over the past five years, representing a $500 million revenue growth opportunity and growing at a double-digit penetration rate. Being a first mover in this area gives WSC a dominant position, enabling it to deliver before competitors can respond. WSC’s product availability allows it to charge higher prices than competitors, often 30-40% higher. Customers prioritize service availability, and WSC has more assets on the ground than its peers.

Additionally, the strong growth of VAPS is expected to continue, with WSC acquiring smaller players that lack access to similar offerings. This expands WSC's customer base, providing new opportunities for cross-selling its services.

(2) Strong FCF generation with optionality

WSC’s strong free cash flow (FCF) generation is driven by its attractive unit economics, particularly in reusing and refurbishing modular spaces. This provides the company with flexibility for mergers and acquisitions (M&A), debt reduction, and share buybacks, while also reducing cyclical risk during potential downturns.

Following the failed M&A transaction with McGrath, WSC's Board of Directors announced the expansion of its existing share repurchase program to $1 billion. During the six months ended June 30, 2024, the company repurchased 2,035,513 shares of common stock for $78.7 million, excluding excise tax. As of June 30, 2024, $419.5 million remained available for future repurchases under the authorization.

Valuation

WSC stock is trading at USD$38.57, 40.66x P/E. Based on trading multiples, a bear case of 7x EV/EBITDA would give us an upside of 54%. For the bull case of 13x EV/EBITDA it would achieve an upside of 213%. Based on a 12% weighted average cost of capital. Estimating EBITDA growing at ~7-10% CAGR.

Risk: What’s next for WSC and McGrant?

Earlier this month (Sept 2024), WSC and McGrath has mutually agreed to terminate the previously announced merger due to the regulatory requirements for the transaction. FTC felt that the merger will detract from the execution of other value creating initiatives inherent in WSC business. McGrant remains the closest competitor to WSC and present hurdles for WSC to dominate in the education sector in modular workplace solution.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.

This was an interesting read Trinsy, the report was succinct and insightful. While I agree that WSC’s innovation and efficient business model allows them to lead the North American modular workspace solutions and portable storage solutions, I am not completely convinced whether they would be able to continue dominating these markets over the long term as I do not find WSC’s moat to be deep. The unit economics of WSC compared to its peers are impressive. However, it can be easily replicated by competitors like MGRC given enough time after their current units – which lifespans are significantly shorter than WSC’s units – become obsolete. Furthermore, the VAPS are not a unique product offering and are also provided by competitors.

Even though WSC acts as a one-stop solution, it does not make them stand out greatly from competitors as they also provide multiple solutions, albeit not as many as WSC. I think it would be useful to delve deeper into its competitive advantages and see how WSC is able to set themselves apart from their competitors. For example, comparing prices between similar product offerings or the average time taken to set up a space.

With all these being said, I agree that the scale of WSC is a key competitive advantage. MGRC having a fleet size 5x smaller but still being their closest competitor emphasizes WSC’s ability to serve their customers more efficiently than their competitors. I also think your 3 and 5 year targets are achievable as WSC's competitors are not likely to be able to catch up within this timeframe.

I’d like to know your thoughts on how WSC is undervalued, I took a quick look at WSC’s competitors (MGRC, URI, and ACO.X) and noticed that they had drastically lower LTM P/E (12.5x, 16.14x, and 13.75x respectively) compared to WSC’s LTM P/E of 259x. What is your opinion on whether WSC will still be able to lead the modular workspace solutions and portable storage solutions after 10+ years?

Thanks for the write-up Trinsy! Found it interesting that you delved into this area, and the consolidation story is also very interesting as well.

1. The management comments indicate that its economic moat precisely exists in that new customers will choose the most reputable and known company in this area, and I do not presume to know which companies are most well-known in this area. But to my knowledge, this is not a household name that will come to mind, and that would mean that when people try to search up temporary space solutions areas, they would rather do a Google search. Shouldn’t the company be focusing on SEO based outcomes, or am I missing something in how the company acquires new customers?

2. If scale is an advantage in this place, and with having a Single-Point of Contact as an investment thesis, you expect WSC to continue acquiring small players that lack access to similar offerings to expand the customer base. However, with quick market consolidation already happening among all players, would this mean

a. that small players would all be sold at premiums and each big player would pay an increasingly larger price to attain these smaller businesses, and;

b. with larger FTC scrutiny existing in this space, that would mean that larger, more aggressive competitors such as McGrath would quickly sprout up with no fear of being acquired by WSC. This would necessarily erode the economic moat that WSC would now have in time.

3. Since a trump victory has occurred, and market looking more conducive than ever for deal making, could WSC be thinking of acquiring McGrath again? Would the share price then fall as a result and would this risk be more present than ever going into 2025?

4. Stock is down since you first covered this, due to EPS miss by -0.08 in Q3 24. Do you foresee any catalysts other than earnings revisions (MS upgraded from 40 to 50 but stock still fell) or earnings results?

5. You also mentioned that McGrath is WSC’s closest competitor. Can I ask why the larger player URI is not as close a competitor as McGrath?