Initial Report: Wise PLC (LON: WISE), 105% 5-yr Potential Upside (Arivarasan M, SC VIP)

Arivarasan M presents a "BUY" recommendation for Wise PLC based on its high growth, margins, and cost advantages over its fintech and banking peers.

About the Company and its history:

Wise is a cross border money transfer business founded in 2011 by two Estonians, Kristo Kaarmann and Taavet Hinrikus, and it was founded actually as TransferWise. Wise is more focused on digital retail payments, which are either smaller peer to peer or small businesses transferring money across borders. However, despite engaging in bank account transfers, Wise isn't a bank, but rather a licensed financial institution.

Typically, the traditional chain of communication between banks is called correspondent banking. The banks are reliant upon an organization called SWIFT for communication. SWIFT is owned by 200 banks. It's used by over 11,000 of them and it stands for the Society of Worldwide Interbank Financial Telecommunications. It is essentially an electronic communication network that tries to put in place a common language and some standards around how cross-border transfers work.

For a $100 transfer across borders, a multitude of banks may need to communicate and reconcile and verify and confirm that the transfer has actually taken place, which slows down time and increases costs due to regulations and various compliances and different opening hours as well. Another problem is that the entire process is opaque.

What Wise does differently is that they maintain this entire network of bank accounts that they own, and therefore there is no need to communicate outside of the company. For example, if it needs to transfer money to India from the USA, it has an Indian bank account, and also an US bank account. . It's the arbitrage of a broken system that Wise manages to fill. Wise is 10x cheaper than the legacy alternatives and much faster, while also being incredibly transparent with the pricing.

The Company, after entering a specific geographical market, moves up the stack to become more centrally integrated into the national infrastructure and become licensed more fully as a regulated financial entity. By doing this, it removes any partner fees or kind of the friction of needing to rely on a partner bank in that market to facilitate those domestic transfers. As they increase this vertical integration over time, they're lowering operational costs and unit costs.

They also utilize AI and machine learning to help try and forecast required liquidity pools in the various domestic countries they operate in, so they don't have to rely on partners or go to the international money markets to get more currency if there's a shortfall in one particular market.

Another thing to consider is that Wise has less than 4% market share in the personal market and is growing at such a rapid pace, yet it's really not spending much in comparison to some of the competitors in the market.

Overall, there is no question that it is an interesting business, just their Mission Zero, the aim of which is to make cross border transactions (which accounts for 80% of their revenues) free, is something that would boggle the mind. However, while pivoting away from cross-border transfers, their aim seems to be to supplement their income with lots of other different features that they can charge for.

Business Model & Operations

Wise PLC (formerly TransferWise) operates a global digital platform for cross-border money transfers, aiming to make moving money internationally faster, cheaper, easier, and more transparent.

Its primary revenue comes from transfer fees charged on international transactions. Rather than a flat fee or high percentage like banks, Wise uses a low, transparent fee plus the real mid-market exchange rate. This cost-plus pricing model ensures a sustainable margin of around 20% while passing savings to customers. The company’s personal money transfer customers contribute the bulk of revenue, followed by a growing base of small business customers, who use Wise for invoices, payroll, and other cross-border payments.

Wise also offers a multi-currency account (the “Wise Account”) for individuals and businesses, allowing users to hold balances in 40+ currencies, spend with a Wise debit card, and receive local bank details in various countries. This account generates revenue via card interchange fees and other services, and drives customer retention through its added utility. Wise’s debit card is linked to its multi-currency account, enabling customers to spend in over 40 currencies without high bank fees. This card and account offering sets Wise apart from traditional banks by providing borderless banking functionality via a fully digital platform.

In recent years, Wise has unlocked a new revenue stream from interest on customer balances. With customer deposits growing, Wise earns interest on these funds. As interest rates rose, Wise’s interest income surged. Wise introduced an “Assets” feature allowing customers to earn a return by holding funds in government-backed assets, but the company still benefits from a portion of the yield.

For example, in FY2024 Wise kept the first 1% yield as underlying interest income and shared the rest with customers. This interest income, while ancillary to transfer fees, has significantly boosted Wise’s total income and profitability in the high-rate environment.

Another important revenue stream is Wise Platform, the company’s B2B offering. Wise Platform allows banks, credit unions, and other fintechs to integrate Wise’s international transfer infrastructure into their own services. Through API integration, partners can offer low-cost, fast cross-border payments to their customers, powered by Wise behind the scenes. This is often co-branded. For Wise, these partnerships expand its reach without heavy direct customer acquisition, and over 85+ partners have joined Wise Platform as of FY24. Revenue is generated by sharing fees with partners or charging the partner institution. Wise Platform differentiates itself by offering banks a turnkey solution that effectively turns potential competitors into collaborators.

Wise’s distribution is purely digital, either through its website or mobile app, meaning no physical branches or agent networks. This allows global scale without the overheads that burden traditional remittance players. Customers from all over the world can use Wise’s services as long as they have a bank account or card to fund the transfer and an internet connection. Wise’s marketing model is notably lean as 66% of new customers find Wise through word of mouth referrals rather than paid advertising. The remaining new users come via online marketing, partnerships, and organic search, but Wise’s CAC is relatively low compared to fintech peers thanks to its referral-driven growth.

Operationally, Wise is headquartered in London with offices globally, but its service delivery is centralized on its platform. The company holds regulatory licenses worldwide, enabling it to hold customer funds and execute payments in compliance with local laws. Wise’s workforce is focused on engineering, customer support, compliance, and localized banking operations.

Wise’s value proposition sharply contrasts with traditional banks. Historically, banks have transferred money cross-border using the correspondent banking network (SWIFT), which involves intermediary banks, high fees, poor exchange rates, and opaque delivery times. Banks typically charge a hefty wire fee plus hide a profit in the exchange rate markup, making international transfers much more expensive than domestic ones. In contrast, Wise charges a transparent fee that is often a fraction of a percent of the transfer amount and uses the real exchange rate. This strategic positioning as a low cost, high speed alternative to banks and a more focused, scaled player than generalist fintechs is a cornerstone of Wise’s success in capturing millions of customers from the traditional banking sector.

Financial Performance & Unit Economics

Wise has delivered robust financial growth, underpinned by rising user numbers and volumes. In FY2023, Wise’s revenue was £846.1 million, up 51% YoY. This top-line growth was driven by a 37% increase in payment volume that year, as active customers grew 34% to 10 million. In FY2024, growth continued as revenue rose to £1.05 billion which is an upside of about 24%.

By FY2024 Wise served 12.8 million active customers, representing a growth of 29% who transferred £118.5 billion, an increase of 13% of payment volumes across borders. Wise’s underlying income still grew over 30% thanks to greater account usage and interest income. Profitability has scaled rapidly. Wise has been profitable since before its 2021 direct listing, and its margins have expanded recently.

Wise benefited from higher rates and kept a portion of that as profit, but even on an underlying basis, excluding interest above 1% yield, PBT was £242 m, representing an underlying PBT margin of 21%. This margin is exceptionally high for a fintech company and even compares well to mature money transfer businesses.

Wise also converts a large share of earnings to cash, as FY2024 FCF was £486 m indicating a cash generative model with low capital expenditure needs. Importantly, Wise has managed to grow rapidly without sacrificing profitability, a rarity among fintechs.

It is however worth noting that Wise’s leadership takes a long-term approach to margins, and they target an underlying PBT margin of 13-16% over the medium term, deliberately choosing to reinvest excess profits into lower prices and growth initiatives.

Its CAC is relatively low in the industry while retention is high. This is partly because once users trust the platform, they consolidate more of their transfers through Wise. High retention and low CAC produce stellar unit economics as each customer brings a high lifetime value for little acquisition cost.

Wise added ~5.4 million new customers in FY2024. The vast majority will stay on and continue transacting. The payback period on any marketing spend to acquire a customer is very short, as often the first transfer’s fee covers acquisition cost, according to Wise’s past statements.

Another aspect of Wise’s unit economics is transaction margin. Wise’s revenue as a percentage of volume has been roughly 0.7–0.8% in recent years. On that, it has maintained a gross profit margin ~65%+. Given the scale and efficiency, Wise has achieved an underlying profit before tax margin of ~20%. The high margins and strong retention mean each customer is very profitable over their lifetime. This suggests Wise’s unit economics, which are enabled by low cost of service, low CAC, high retention, economies of scale and growing ARPU are among the best in fintech. Most important is the fact that satisfied customers bring in more customers and more business, lowering relative costs and increasing margins, which Wise can then partially pass back as lower prices, which is fueling further growth ensuring scalable profitability.

Cost Structure

Wise’s cost structure can be broken into cost of sales, which includes banking partner fees, payment processing, and currency conversion costs and operating expenses such as administration, product development, support, compliance and marketing. In FY2024, cost of sales was £307 m, essentially flat from £308 m in FY 2023.

This means that despite strong volume growth, Wise drove efficiencies to keep transaction costs stable. Consequently, gross profit grew 51% to £853 m in FY 2024.

Wise’s gross margin of ~70% reflects that once a transfer is executed, a large portion of the fee is retained, this is because the actual marginal cost of moving additional money is low thanks to the automated platform.

Opex as a percentage of total income has been trending downward. Marketing spend in particular is efficient due to word of mouth growth, this is because 2/3rds of the customers join the company via referrals at no cost to Wise.

Industry Trend Overview

Wise operates in the global cross-border payments industry, which is enormous and undergoing rapid modernization. This market includes remittances such as person-to-person transfers, B2B trade payments, e-commerce payments, and more. In total, cross-border payment flows are projected to reach $250 trillion by 2027, up from about $150 trillion in 2017.

The growth is driven by globalization of commerce, migration, and digital connectivity. Within that, the segment of low value international payments relating to consumer and small businesses where Wise focuses is expanding as more individuals transact globally for freelancing, overseas education, travel, family support, etc.

Remittance flows hit a record high in recent years, and e-commerce and gig-economy payments across borders are rising. Historically, this vast market was dominated by banks and legacy money transfer operators. Banks facilitated wire transfers via SWIFT, and firms like Western Union and MoneyGram built extensive agent networks for remittances. These traditional channels, however, have long-standing pain points, which are high fees, poor exchange rates, slow delivery, and lack of transparency.

For example, sending money from a bank in one country to another often incurs intermediary fees and can cost 5–10% of the amount for retail customers. Western Union and similar MTOs provide faster cash remittances but charge significant commissions to fund their agent and compliance network. This inefficiency and cost created a ripe opportunity for fintech disruptors. Over the past decade, digital-first fintech companies such as Wise, Revolut, Remitly, PayPal through Xoom, and others have been steadily eating into banks’ share of cross-border payments.

These fintechs leverage modern technology to streamline international transfers. According to a Citigroup survey, over 40% of banks have already lost at least 5% of their cross-border market share to fintech competitors, and 89% of banks expect to lose at least 5% more in the next 5-10 years. This highlights the accelerating shift as customers discover better alternatives. Fintech solutions tend to offer real-time or near-instant transfers, lower fees, and a much better user experience compared to the legacy model.

Another trend is increased transparency and regulation pushing for lower costs. G20 and World Bank have also set goals to reduce average remittance fees to below 3% by 2030. Which is putting pressure on all players to drop fees.

However, incumbents are responding slowly. Banks are upgrading their systems or partnering with fintechs like Wise or others. However, their legacy businesses and cost structures often prevent them from matching the pricing of digital-native players. Also noteworthy is the potential impact of cryptocurrency and blockchain in cross-border payments. Companies like Ripple (with XRP) and stablecoin platforms offer the promise of near-instant settlement globally without traditional banks. While crypto hasn’t yet achieved mainstream consumer adoption for remittances, it’s a space that could pose a disruptive force in coming years.

However, the overarching theme is that competition is intensifying from all corners, including fintech peers, incumbents adopting new tech, and possibly Big Tech or crypto entrants.

Competition

Banks & Credit Unions

These are the primary incumbents from which Wise wins customers. Banks typically offer international wire transfers and some now offer online/mobile transfers. However, their services remain costly and sluggish due to legacy infrastructure. For example, a major US or European bank might charge a $/£30 wire fee plus a 3% FX markup, and take 2-5 days – versus Wise’s low fee and same-day delivery.

Wise has been directly siphoning customers from banks by highlighting how much one can save. Wise’s CFO also noted that the majority of Wise’s users are people switching from using banks for transfers.

Banks have huge customer bases and trust, but their inertia and high fees leave them vulnerable. Some banks have chosen to partner via Wise Platform to offer Wise’s service rather than build their own. Wise’s challenge with banks is to continue convincing consumers and businesses to step outside their default bank and use a separate app for international needs. As awareness grows and word spreads, this is happening at scale. Banks’ competitive response so far is limited to incremental fee reductions or fintech partnerships, as building an equivalent global low-cost network from scratch is difficult.

These incumbents still serve a segment Wise doesn’t, which is cash-based remittances where migrant workers send cash to areas where recipients may not have bank accounts. Wise currently requires bank accounts or cards on both ends, which limits reach in some developing markets. However, as the world banked population increases and digital wallets spread, Wise can address more of this remittance market. Wise’s advantage is strongest in bank-to-bank transfers and account deposits, whereas legacy players still have the agent networks for last-mile cash. Over time, physical networks may become less relevant, and Wise is well positioned to capture volume from these players.

Digital Remittance Fintechs

Remitly, WorldRemit, InstaReM focus on remittances, often targeting specific corridors only. Remitly is a notable peer, a Seattle-based digital remittance provider that went public in 2021. In 2023, Remitly’s revenue was $944 million growing 44% YoY, it currently as of 2024 has 7.8 million customers. Remitly’s business is primarily migrant remittances

Wise and Remitly likely have overlap in customers in corridors where both operate. Wise may win on price, while Remitly might attract users sending to regions where Wise is less established. WorldRemit is another digital player, similar in size to Remitly, focusing on mobile and cash payouts in developing countries. These fintech peers collectively indicate a booming digital remittance sector, taking share from incumbents, but also competing with each other.

Multi-Currency Neobanks

Revolut and PayPal are some fintechs that offer currency exchange as part of a broader suite. Revolut, for example, lets users hold multiple currencies and do exchanges at interbank rates up to a limit, with a small markup on weekends. Revolut has gained over 25 million customers globally with its multi-currency card and app. For basic FX transfers, Revolut can be very cheap, which poses a competitive threat to the tech-savvy segment. However, Revolut’s core is more around card spending and banking alternative features; for large international transfers or business payments

PayPal is another major player. While known for domestic payments, PayPal owns Xoom, a digital remittance service, and also facilitates cross-currency payments for merchants and peer to peer. PayPal’s fees for cross-border personal payments are relatively high. Xoom targets remittances and charges a margin, so it hasn’t undercut Wise on price either.

Emerging Decentralized and Card Network Solutions

There are new solutions like Ripple aiming to enable cross-border transfers with crypto or central bank digital currencies in the future. Ripple has partnered with some banks for back end settlement, though its usage in retail remittances is limited so far. Stablecoins and crypto exchanges are sometimes used by individuals to move money. These methods can be very fast and cheap, appealing to a niche of tech-savvy users.

No single competitor currently offers the exact same model of global accounts and cheap transfers at Wise’s scale. The key trends favor digital disruptors like Wise, yet the company must stay vigilant as incumbents are adapting, albeit slowly.

Wise leads on cost to consumers and is a technology leader in terms of integrating local payment systems for speed. In terms of profitability, Wise and Western Union both generate solid margins, albeit via very different models. Remitly and other newer fintechs lag in profitability but are catching up in volume and revenue. Wise’s public-market peers in fintech like PayPal tend to have broader businesses, so Wise stands out as a more singular cross-border specialist.

In the big picture, Wise has positioned itself as the benchmark for international money transfers against which others are compared. It forced the industry to increase transparency on FX fees and speed

The competitive landscape is dynamic, but as of now, Wise is a leader in its niche, outperforming traditional players on growth and beating most fintech peers on profitability and scale in cross border payments.

Investment Thesis

Wise offers a rare combination of high-growth and actual profitability in fintech. It has consistently grown revenue 30-50% YoY while maintaining healthy profit margins and positive cash flow. Its user base and volumes continue to scale globally, tapping into an enormous addressable market. Unlike many fintechs that burn cash to grow, Wise is self-funding its expansion with profits, which is a sign of a sustainable business model.

Despite its success, Wise has only scratched the surface of its market. Management estimates Wise has a very minimal share of global consumer cross-border transfers and small business transfers. The vast majority of individuals and SMEs still use banks or incumbents for international payments. This represents a huge runway for growth. As awareness increases and Wise continues to add features, it can capture significantly more customers.

Global trends also favour the company. Global migration, remote work, and e-commerce mean cross-border transactions will grow. Wise is also expanding into more emerging markets to multiply its volumes. It is also a possibility that Wise could replicate its success in remittances in B2B payments, which are trillions in flows where businesses are equally frustrated with bank fees.

Wise has a significant cost advantage over both banks and fintech peers. Its proprietary network of local accounts and scale allows it to process transfers cheaper than others, and importantly, to pass much of those savings to customers while still earning a margin.

New entrants would need years to build a similar global infrastructure and liquidity network, and the network effects in terms of clients are numerous, as satisfied customers and word-of-mouth referrals help Wise grow without burning cash on marketing.

Wise’s integration into banks via Wise Platform could make it an industry standard backbone for cross-border payments, entrenched behind the scenes.

Wise also has opportunities to monetize beyond transfer fees. The rollout of Wise Account features like Assets for earning interest can increase ARPU and stickiness. Already, 48% of personal and 60% of business customers are using Wise for more than just occasional sends. This points to Wise evolving from a single-use tool into a primary financial account for internationally active customers. That increases lifetime value and provides cross-sell opportunities.

In a rising interest environment, Wise’s profitability gets an extra boost,as seen in recent results from interest income, which can be reinvested in further growth or margin expansion.

The Moat

Wise’s competitive moat stems from a combination of cost structure, network effects, technology, and brand, and most importantly its superior service quality. Wise, adopts a different way or a superior way, a new way of doing business, which an incumbent bank, can't or doesn't want to respond to or mimic due to the foreseen damage it will do to its own business. So just from a price perspective, Wise is, due to their efficient model, able to cut out a lot of that inefficiency and offer the lowest possible price to the consumer.

The strongest moat is the cost advantage which the company enjoys through its unique infrastructure, which is its low cost operating model for international transfers. By circumventing correspondent banking and instead using its own network of local accounts and internal netting of currencies, Wise avoids many of the fees that banks and competitors incur. This allows Wise to offer prices that are genuinely hard for others to match without losing money.

For a traditional bank to match Wise’s fee on, say, a £1000 transfer, it would often have to waive its wire fee and give up the FX margin which would make the transfer unprofitable for the bank given their higher overhead.

The more the volume, the lower the average cost per transaction. It’s telling that Wise can consistently maintain around a 65-70% gross margin while charging minimal fees, implying that their internal costs per transfer are extremely low. This cost advantage is a significant moat, as it’s not easily replicated.

A new entrant would require years of investment, regulatory approvals, and trust-building to set up a similar global footprint.

Furthermore, as more customers use Wise, two things happen that strengthen its position, firstly Wise can match more transfers internally, reducing reliance on external FX trades. Secondly, when many people and businesses have Wise accounts, sending money within Wise’s network becomes more instantaneous.

Network effects are huge, as the more businesses and freelancers use Wise, the more their counterparties might adopt Wise for convenience. Each new bank or app that integrates Wise effectively funnels more volume into Wise’s system, strengthening its network and making it harder for any single partner to switch out.

Wise has built a strong brand around being trustworthy, transparent, and customer-friendly in a sector notorious for the opposite. This reputational moat means consumers often think of Wise first when they need to send money abroad.

Wise’s platform is a moat in terms of its user experience and capabilities. It’s not just the low fees, it’s also how easy and fast it is to use Wise. Many banks struggle to offer such quality due to clunky IT systems. Wise’s continuous innovation, such as implementing new local payment rails as soon as they become available, such as Brazil’s PIX or India’s UPI means it often leads in speed of delivery, and speed is a very important competitive differentiator. Especially considering the fact that 62% of Wise transfers are now instant.

While regulation can be a burden, it can also form a barrier to entry. Wise holds dozens of licenses which it has acquired over a period of time. A new entrant would face a steep curve to convince regulators to grant licenses at scale. Incumbents have this too, but many fintech peers are still expanding their regulatory footprint. Wise’s early start in many markets gives it a regulatory moat.

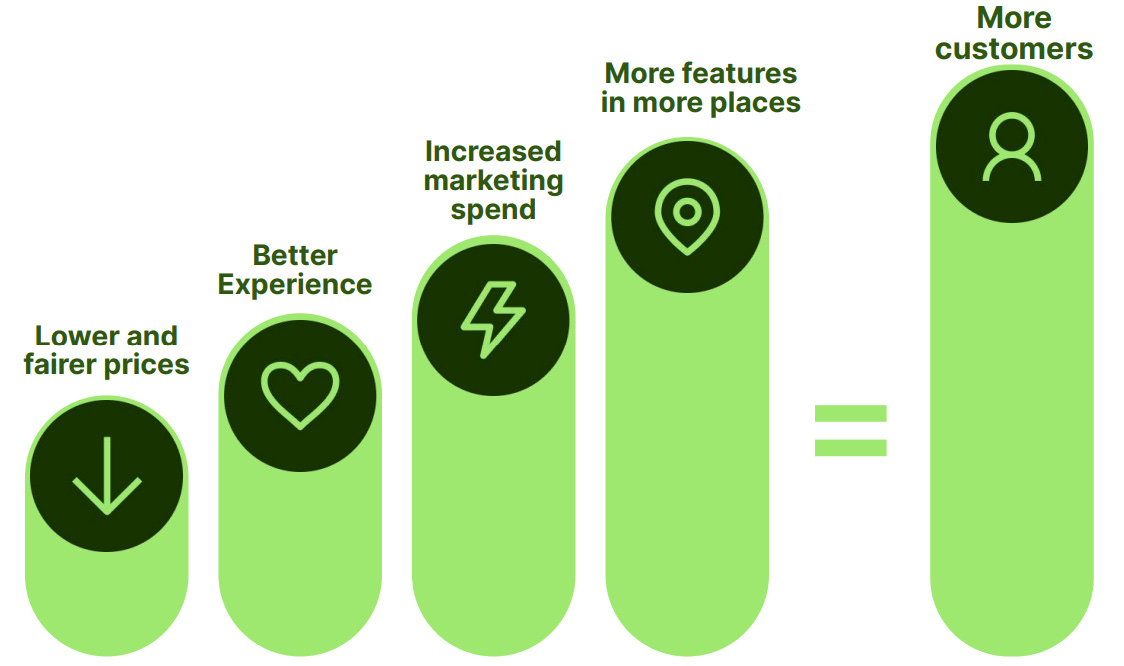

The most fundamental thing to understand about Wise is that they're always trying to drive the lowest price possible as opposed to what a lot of companies do, which is focus on profit maximization in the shorter term, where they're pricing to the equilibrium whereby they price as high as possible without forcing a customer to leave and seek services from a competitor. Wise always transfers the benefit to the consumer.

Future Prospects

One key opportunity for the company is geographic expansion and deeper penetration in markets outside its strongholds. Wise is originally Europe-focused, and the UK and US are major markets. There remains huge potential in regions like Asia, Africa, and Latin America where cross-border flows are large. Wise has made inroads in India, Japan, Brazil and the Philippines, but could further localize and market its services in other countries with high remittance outflows and inflows. As more people in emerging markets get bank accounts and come online, Wise’s total addressable customer base will expand.

The partnership approach, which is the Wise Platform will also help, as signing up banks or mobile wallet providers in those regions can bring Wise’s tech to local users without direct customer acquisition.

Another growth driver is Wise Business. SMEs conducting international trade, paying remote workers, or managing global accounts have many pain points that Wise can solve. Wise has been ramping up its business offerings, such as batch payments, interfaces with accounting software, and multi-user access for business accounts. The global B2B cross-border payments market is massive. While Wise historically focused on consumers and micro-businesses, moving upmarket slightly to target larger SMEs or even mid-sized corporations could greatly increase volumes per customer. Wise’s low fees are expected to be attractive to businesses that make frequent international transactions

Wise’s introduction of assets allowing customers to earn interest on balances by investing in safe instruments hints at further expansion into financial services adjacent to payments. There is also the possibility that in the future, Wise could offer things like international lending or even cross-border investment products. The key theme is leveraging Wise’s infrastructure to remove friction in any global financial interaction. If executed well, these new services could open additional revenue lines.

Macro tailwinds could also aid Wise. The trend of remote work and digital nomads means more individuals are earning in one currency and living in another, creating natural use for Wise accounts. Furthermore, global e-commerce growth means more sellers need to move funds across borders. Additionally, if certain currencies become more volatile, users may want to hold multiple currencies, which is enabled by Wise, unlike many banks.

Stock Valuation and Investment Outlook

Wise’s stock has seen a volatile journey since its direct listing in July 2021 at about 8.74 GBP per share. It traded as high as 11.76 GBP in September 2021, after which the stock has been racing downhill, where it finally made a bottom of 2.86 GBP around June 2022 before rebounding strongly through 2023 as results and growth impressed. As of the moment of writing this report, Wise currently trades at 8.9 GBP.

Wise does not pay a dividend, and while Wise’s P/E is higher than most banks and legacy payments companies, it is lower than many growth fintech peers. For instance, PayPal trades around 17x earnings, but with single-digit growth, while Adyen trades at 50x earnings. While WIse currently trades at 25x PE, I believe that it deserves a valuation of 30x PE considering the various factors mentioned hereinabove, which should ideally result in a target price of 15 GBP by 2027, equating to an estimated upside of about 70% in 4 years.

However, ideally entry price as per my estimate should be around 8 GBP for a higher margin of safety for the investor.

Wise’s dominant position in a growing niche could allow it to eventually take a meaningful chunk of a multi-trillion market, which would make today’s valuation look small. While the opposite could happen, where growth could taper and competition may nibble away at fees, compressing margins, which would in return lead to the Company being treated at valuations closer to legacy banks, which would result in a heavy downturn. The outlook is however looking positive given the trends and the company’s track record.

Risk Factors:

While Wise’s historical growth has been strong, there are signs of moderation. Customer growth was +29% in FY2024, a deceleration from +34% the prior year. Volume growth was only +13% vs 37% prior. The low-hanging fruit of easy to acquire clients may already be using Wise. However, to continue growing at 20-30%, Wise might need to expand into segments that require new capabilities or higher marketing spends, which the company has yet to do.

A notable portion of Wise’s recent profit surge comes from interest income on customer balances. In FY2024, out of £481m PBT, £364.5m came from interest above the first 1% yield. The US Fed is expected to come with rate cuts very soon. Similarly, if global interest rates retreat, this income will decline. Wise has been upfront that it doesn’t intend to keep all this benefit, and it has started sharing more interest with customers through paying them yield via Assets or cashback. Wise’s EPS could disappoint in future years.

Wise is heavily tied to the fortunes of cross-border payment trends. If for any reason that activity declines, Wise doesn’t have other large revenue streams to offset it. In contrast, some peers like PayPal have broader ecosystems to fall back on if one segment falters.

As a cross-border financial services provider, Wise is heavily exposed to regulatory oversight. Each country’s regulators can impose licensing requirements, capital rules, anti-money laundering (AML) standards, and data protection laws. Maintaining compliance in dozens of jurisdictions is complex. A failure in compliance could result in fines or even suspension of services in that region. For example, the Company was forced into a formal remediation plan after the National Bank of Belgium found in 2022 that there was a shortcoming in its AML controls, which led to hundreds of thousands of accounts not having proper addresses.

Any major security breach, hacking incident, high profile outage or regulatory penalty on Wise could shake customer trust in its brand moat.

If one day, all the central banks decide to create a globally interconnected instant payment network that’s low cost, as a means to promote trade, commerce and globalisation, banks might be able to offer near Wise pricing, diluting Wise’s differentiation.

In a global recession, there might be fewer international job opportunities, thus fewer remittances or business transactions. Macro factors like interest rates also play a role, because if interest rates globally decline from their recent highs, Wise’s interest income which has been boosting profit will shrink.

Competition is a persistent threat. Giants like Western Union are not standing still and fintech peers are also well funded and innovating. If a competitor drastically cuts fees or a new entrant subsidizes transfers, Wise might have to respond to avoid losing market share, which could erode revenue. Additionally, giants like Google, Whatsapp and Apple have also shown interest in payments. A deep-pocketed competitor could decide to run cross-border transfers at zero profit or even at a loss to gain market share, effectively undercutting Wise’s cost advantage. For example, a global tech firm could bundle free transfers with another product. This could pressure Wise’s fees and test how much of its volume is loyal vs price-sensitive.

Another challenge is multi-currency liquidity management at a larger scale. Wise has to ensure it has enough float in each currency to facilitate instant payouts. As volumes grow, those floats become bigger, and misjudging liquidity needs could either tie up too much capital or cause delays if under-provisioned. So far, Wise has managed well, but higher scale means a higher possibility of error.

Great post. I’ve also done deep research on Wise plc and I agree with your take.

That said, investing isn’t about finding people who agree with you, it’s about finding those who disagree so you can stress-test your thinking.

If you think I’m missing something, I’d genuinely love to hear it. https://therationalcapitalist.substack.com/p/why-the-market-underestimating-wise