Meet the Investor - Discerene Group LP - Mr. Soo Chuen Tan

An Unforgettable Session with Soo Chuen: Insights from the Founder of Discerene

The session began with a brief introduction to the speaker, Mr. Soo Tan, the President and Portfolio Manager of Discerene Group. Mr. Tan initially studied law before attending business school. Before founding Discerene, he honed his skills at prestigious firms such as Deccan Value Advisors, the Baupost Group, Halcyon Asset Management, and McKinsey & Company.

Mr. Tan started by sharing that he discovered investing during his time in business school. Today’s session, organized by the Z Club, prompted him to express his regret that there wasn’t a Z Club during his own time in business school.

He also provided some background about his family, mentioning that he comes from an academically inclined and science-oriented family, rather than one focused on business or investing.

Mr. Tan graduated as the top student in his law school class, but he chose not to practice law because, while he enjoyed studying it, he found business more interesting than legal practice.

During his time at McKinsey, he learned a great deal about businesses. He witnessed the height of the dot-com bubble and its subsequent bursting, during which many restructurings took place. He recalled how it was a fascinating time to learn through observation.

He mentioned that he first discovered Warren Buffett in his mid-20s through reading Buffett’s investor letters when Buffett visited his campus. He found it incredible that someone could pursue a career in investing. He chose not to return to McKinsey after business school and joined an investment firm instead.

Mr. Tan noted that the mentorship from his professors and learning about Buffett were pivotal moments in his life.

When asked about his investment philosophy, Mr. Tan explained that value investing is logical and makes a lot of sense. He emphasized that, as value investors, we own businesses, not stocks, and our goal is to determine a company's worth and buy it at a discount. He stressed that a company's worth is independent of its market price.

He pointed out that, as value investors, we must strive to figure out a company’s worth, even if we have imperfect tools, skills, and knowledge.

Mr. Tan also spoke about his time at Halcyon, they focused on distressed companies and special situations. He mentioned how his legal background was beneficial in analyzing businesses going through bankruptcies. His experience with distressed credit helped him to focus on downside protection in potential investments, a discipline that continues to serve him well after 20 years.

He reflected that witnessing how companies fail can open one’s eyes and improve one’s ability to analyze companies that are still going concerns.

Mr. Tan emphasized that joining a startup teaches one more about a business as one needs to learn to be resourceful as the startup struggles to survive, and to build a company from the ground up.

He recounted how, during the mid-2000s—when hedge funds were at their peak—the startup he worked for rapidly grew from $300 million to $2 billion in assets within just three years, which felt like experiencing entrepreneurship at high speed.

Mr. Tan explained that investing is more of a probabilistic craft than a science, and as an investor, one must try to stack the odds in one’s favor.

He suggested that the first question one should ask is whether a company has a compelling reason to exist. For example, if the business disappeared overnight, would the world be significantly different? He cited the example of Lululemon products, noting that if they disappeared, the world wouldn’t change much. In contrast, the disappearance of the Suez Canal would have a far greater impact.

He also discussed the concept of long-term investing. In particular, can one buy the common stock of a company and then doesn’t look at it for 10 years predict what the company looks like in 10 years? He believes that no one can predict a company’s earnings in 10 years, but can one at least reasonably predict such company’s business model, customers, products, and services a decade out?

Mr. Tan also advised setting aside companies that may be too difficult to understand, not necessarily because they are bad businesses, but because they fall outside one’s circle of competence. If it’s not something one has the skills to understand, it’s better to move on to the next opportunity.

He then discussed the importance of a business’s barriers to entry, suggesting that we put ourselves in the shoes of someone trying to compete against the business. For example, imagine how would Elon Musk approach it attacking the business? How defensible is such business to an attack? However, he noted that even after doing all the work to reasonably calibrate a business’s barriers to entry, one can still be wrong, as nothing is foolproof in investing.

Regarding Discerene’s investment strategy, Mr. Tan explained that, if nothing’s changed about a company they own, they try to buy more shares as the company’s stock price declines. For example, if a company is worth $100 and they can buy it at $60, they will continue to buy more as the price drops to $50 or $40, as the risk-reward ratio improves with a higher margin of safety.

However, he also emphasized the importance of considering the risk of permanent capital impairment. Their analysis could be wrong, and the company might be worth less than they initially thought. They size their investments accordingly

Mr. Tan mentioned that Discerene has only one portfolio manager—himself. He noted that they don’t trade stocks frequently as other firms do; instead, they buy stocks only when they’re at a discount. Portfolio management at Discerene is more of a process than a distinct role.

In terms of hiring, Mr. Tan explained that they typically recruit people early in their careers. Traits such as grit, hard work, patience, passion for investing, logic, and honesty are highly valued. Skills can be taught, but traits are inherent. He also mentioned that turnover rates at Discerene are very low. The investment team is currently an international group with seven different nationalities, speaking eight different languages.

When asked about the market for distressed credit investment firms in Singapore, Mr. Tan believed that distressed credit is a niche market in Singapore and other Asian countries. Mr. Tan explained that distressed credit investing is specific to each country due to differing legal frameworks across jurisdictions, and that restructuring laws in Asia are not as developed as in the US.

He pointed out that in the US, restructuring is common, whereas in Asia, bankruptcy is often perceived as shameful.

He gave an example from Japan, where after the financial-markets bubble burst, many companies were unwilling or unable to restructure for a long time. He also shared that when he joined Halcyon, he didn’t know much about modeling or, restructuring but learned on the job.

Mr. Tan finds his legal knowledge valuable even today and believes studying law was a good decision.

He learned how to understand the law in the context of how a company operates and reiterated that this understanding is crucial for analyzing companies. He mentioned that his legal background has been helpful in running Discerene, he highlighted that law teaches logical reasoning, a skill that is also beneficial for investing.

Book recommendations for someone new to investing:

The Intelligent Investor and Security Analysis by Ben Graham

The Letters of Warren Buffett

Competitive Strategy by Michael Porter

The Theory of Industrial Organization by Jean Tirole

Capital Ideas by Peter Bernstein

The General Theory of Employment, Interest, and Money by John Maynard Keynes

Capital Account by Edward Chancellor

The Most Important Thing by Howard Marks

Margin of Safety by Seth Klarman

What I Learned About Investing from Darwin by Pulak Prasad

Mr. Tan also discussed the rise of passive investing over the past 15 years, as indexes have outperformed many active investors. He noted that larger companies have historically underperformed smaller companies due to their size, but unexpectedly, in the last 15 years, larger companies have sometimes been faster-growing.

He highlighted how the tilt towards growth investing, rather than value investing, is influenced by monetary policy and interest rates. This environment encourages people to focus more on growth than on barriers to entry, margins of safety, and downside protection.

Mr. Tan acknowledged that these trends have not favored Discerene, which focuses on active, contrarian value investing on a global scale. However, Discerene has thrived despite these headwinds. He believes that investment trends tend to be cyclical.

He mentioned that growth and passive investing might lose popularity as the growth rates of large companies slow due to the law of large numbers. The reduction in the number of active competitors, especially those pursuing value investing strategies, is also beneficial, as there will be less competition for those left standing. He emphasized the importance of maintaining investment discipline and the willingness to persevere during difficult periods.

During the Q&A session, a student asked about whether good investment ideas are typically time-sensitive. Mr. Tan agreed that this is often the case, noting that many of their best ideas are bought during times of crisis.

Mr. Tan concluded the session with advice to students, encouraging them to think logically, know themselves, and make sound decisions that aren’t necessarily influenced by what others do. He shared that his best decisions have come from doing what he believed was the right thing even when it wasn’t popular.

Generation Z Investment Club, VIP

Arivarasan M

It does not happen every day when you are in the same room with Soo Chuen Tan (SCT) for our session at the investment bootcamp. From his recollections of his humble beginnings in Southeast Asia to found and lead Discerene in Stamford, Connecticut, I knew this talk would be a special one.

A moment that caught my attention was not actually from the reading list. It came after the session in the form of a LinkedIn post by SCT, discussing the Isaiah Berlin essay titled “The Hedgehog and The Fox” and how he applies the ideas therein to Discerene’s culture.

I personally applaud the sincerity of SCT in sharing his investing journey. Let us hear more reflections about SCT’s sharing from our members who attended the event.

Generation Z Investment Club, VIP

Fabian VERA

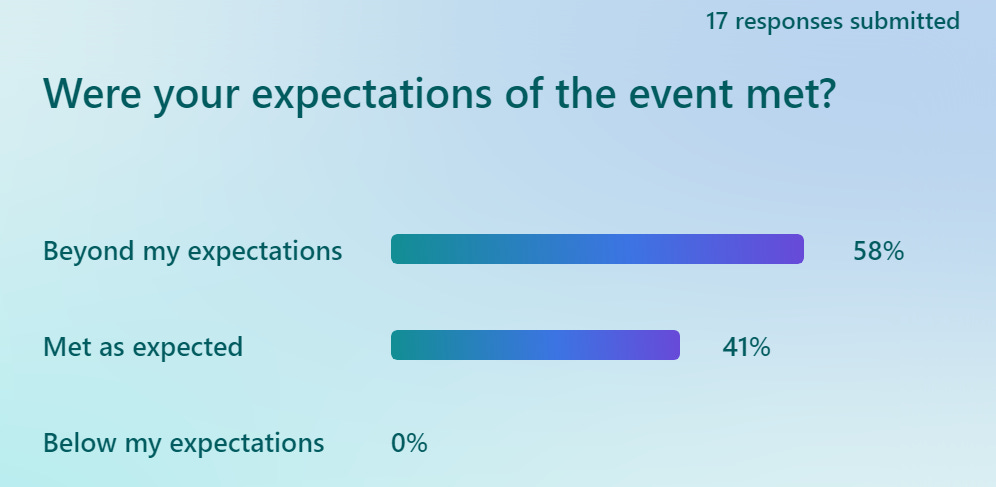

Feedback

What did you learn from Mr. Soo Chuen Tan?