Quarterly Letter, VIP SEA

Quarterly Letter from CIO, VIP Southeast Asia Chapter, Q1 2024

Dear Sponsors, Board of Advisors, Members, and Readers,

I’m You Gin, one of the co-chairs for VIP SEA. With this letter, I am eager to share the exciting updates for Q1 2024.

We had our 2nd Z Club Academy session with Allen Xiao, Deputy Chief Risk Officer of Amundi Asset Management, who is also on the board of Next Generation Investors Endowment. It was an insightful sharing session where Allen shared about the global sustainability landscape and how the world is seeking to achieve their green goals. During the session, we also discussed how the US elections at the end of the year will affect trade policies that can affect the green movement. In May, we also had a sharing session by Daniel Phua from Ford Asset Management where he shared with the club about Swedish Serial Acquireres, a group of investors who can create shareholder value through acquisitions despite such activities being generally bad for companies. In June, we will be hearing from Raymond Goh, founder of New Silk Road on fundamental research. I look forward to hearing from these esteemed investors.

Currently, our analysts are working on their memo for h1 2024 and I look forward to the new ideas that they will be bringing. VIP SEA met in person last week as one of our international members, Claire is in Singapore. We had a lot of fun interacting with one another and exchanging new ideas. VIP SEA is also beginning recruitment for our next batch of analysts for 2024 with an additional interview round during recruitment. There have been no significant updates since the previous letter. As such, this letter will provide updates on existing positions and new companies that VIP SEA is monitoring.

Portfolio Update

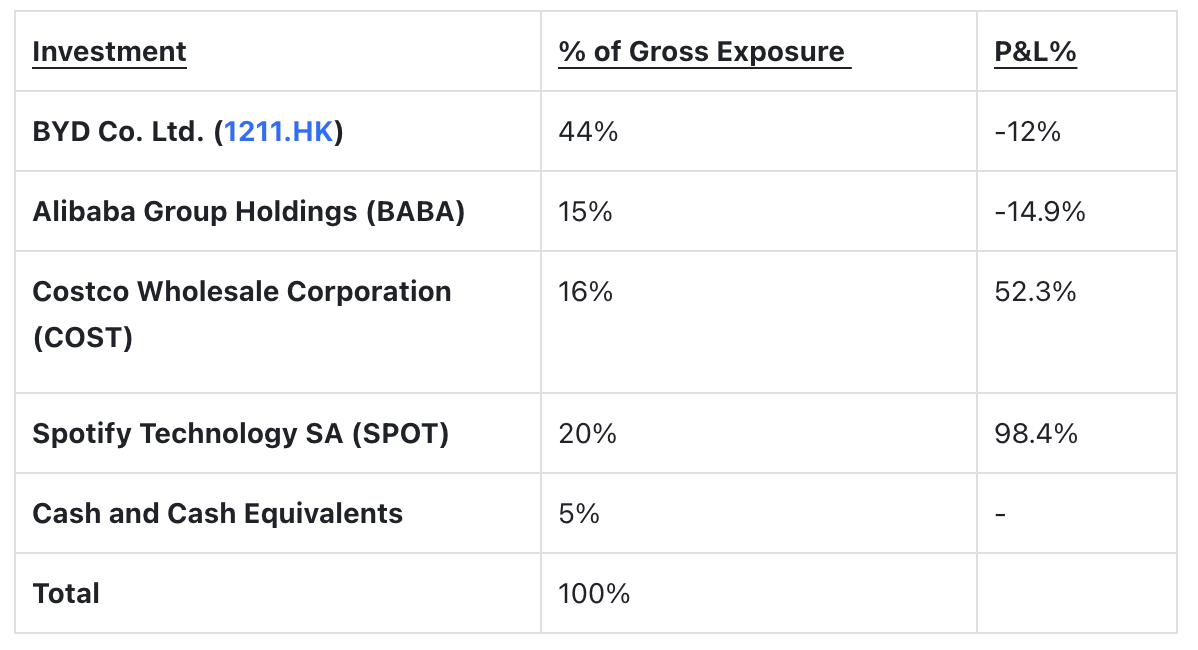

Alibaba

In the last month, Alibaba stock is up 30%, reaching almost $90. Several factors are driving its stock price higher, most being non-fundamental reasons. One is investor, Michael Burry of Scion Asset Management, increasing his stake in several China companies including Alibaba. The broader Chinese stock market also marked a strong rebound over the past two months, as global investors slowly warmed up to China stocks amid persistent government support. China was also seen winding down a regulatory crusade against its internet giants over the past year, as Beijing looked to all avenues to boost growth. From a technical perspective, China stocks may not look as bleak. The Hang Seng Index, comprising some of the largest companies in the Hong Kong Stock Market, is up almost 20% from its low, potentially signalling an uptrend in the broader China market. However, to put things in perspective, the index was up almost 50% in 3 months on Jan 23 but continued trending down afterwards. We will continue to monitor Alibaba to see if the general rebound in the Chinese macroeconomic environment is sustained.

Costco

Since the last letter, Costco is up almost 12% and is at an all-time high of $800. At this price, it is trading at 52x P/E which is significantly higher than its historical average of 33x. This is also higher than the average Forward P/E of 20x for its industry. The recent spike in May was due to Uber announcing a new ridesharing service, Uber Shuttle, where users can reserve up to five seats in advance on buses. Uber is partnering with Costco where Costco members will get a discounted rate on the new ridesharing service. Costco members will also receive additional discounts on their orders on Uber Eats and also a 20% off on the annual Uber One plan. From my point of view, this does not affect Costco's fundamentals significantly and the rise in the stock price is unjustified, mainly driven by sentiment. Costco's main net profit margin driver is still membership sales and it is unlikely that the partnership with Uber will drive membership sales up significantly. The near-term sustainable driver of the stock is still likely to be the membership rate hike which is set to happen any moment. At this price, we are heavily considering exiting the position to take advantage of this spike in price.

Performance Food Group

Performance Food Group is a company pitched by one of our analysts, Julian. We are generally optimistic about PFGC despite near-term headwinds and the high inflationary environment. PFGC has reported gains in bottom line and cash flow despite facing significant headwinds this quarter. It successfully gained market share in both independent and chain restaurants, outpacing the total industry. At the same time, PFGC's largest foodservice segment saw a 1% increase in net sales with similar volume growth, reflecting resiliency and potential for further growth despite current pressures. Looking ahead, we are encouraged by recent trends, with 3 operating segments gaining new chain businesses which should help accelerate growth in Q4, despite a less stellar Q3. In terms of low single-digit inflation for its key segment food service and rise in tobacco prices, given the PFGC % markup style, it would prove to help drive higher selling prices. However, given how PFGC is a retailer, high inflation puts pressure on consumer wallets, coupled with the overall consumer environment remaining soft, especially in QSR, thereby impacting the company's performance. PFGC experienced a drop in net margins which we believe are shorter-term issues including OPEX such as wages, maintenance and net income due to higher taxes. That said gross margin improvements were noted and combined with the easing of industrial headwinds, we could see further upside for PFGC moving forward. We conducted an analysis and found no significant correlation between inflation and PFGC's performance. We are continuously monitoring PFGC and how it continues to adapt to this high inflation and high-interest rate environment.

I look forward to the next update where new positions will be initiated in the portfolio.

With Best Wishes,

Cheng You Gin

on behalf of the Value Investing Program’s Southeast Asia Chapter